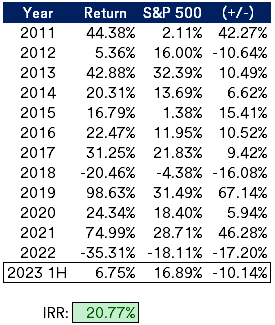

This will likely be extra of a quick check-in quite than a full evaluation. Sadly, my latest spell of underperformance has continued into the primary half of 2023, my portfolio is up marginally, 6.75% versus 16.89% for the S&P 500. I am nonetheless above my long run aim of 20+% IRR; the present goes on.

The primary efficiency detractors had been outsized positions in MBIA (MBI) and Transcontinental Realty Buyers (TCI), two speculative M&A candidates which have didn’t materialize. Lots of my different speculative M&A concepts did announce offers, however nicely under the place I had penciled them out. Consequently, I’ve leaned extra on smaller place sizes within the damaged biotech basket and different flavors of particular conditions for brand new concepts not too long ago.

The one outsized performer was Inexperienced Brick Companions (GRBK), homebuilders have exceeded low expectations as single household dwelling stock has remained tight regardless of rising rates of interest. I’ve begun to promote down my place, it had develop into too giant and does not actually match into a price or particular scenario bucket any longer.

Closed Positions

- Radius World Infrastructure (RADI), INDUS Realty Belief (INDT) and Argo Group Worldwide (ARGO) all acquired bids that had been a bit disappointing from elevated early 2022 expectations when rumors surfaced that every had been on the market. All had been rate of interest delicate companies the place the worth declined as charges rose quicker than initially anticipated.

- Within the damaged biotech basket: 1) offered Talaris Therapetuics (TALS) after their latest reverse merger with Tourmaline Bio for a pleasant achieve; 2) offered Oramed Prescribed drugs (ORMP) for minimal achieve after a number of readers identified their promotional (perhaps being form) administration after which noticed it first hand; 3) Offered Carisma Therapeutics (CARM, fka Sesen Bio) after the reverse merger, was left with a stub place (acquired the non-tradable Sesen CVR) that I offered pretty indiscriminately for a small loss.

- The Franchise Group (FRG) story ended quite disappointingly, have a little bit of a bitter style in my mouth, after rumors surfaced early within the 12 months that CEO Brian Kahn was contemplating taking the corporate personal. FRG then went on to have a horrible Q1 the place they breached a covenant of their credit score facility, stopping them from persevering with their dividend, that was disclosed concurrently the corporate agreed to Kahn’s $30/share buyout. For the reason that firm is type of a one-of-one primarily based on Brian Kahn’s deal making, with a covenant breach, it was unsurprising that no different bidder got here ahead in the course of the go-shop interval.

- I offered Star Holdings (STHO) shortly after the shut of iStar/Safehold transaction after a number of readers reached out with some considerations on SAFE. I will re-evaluate down the highway, that is one I will possible rebuy once more sooner or later in its liquidation journey.

- My thesis in Liberty Broadband Corp (LBRDK) was stale, I initially purchased Common Communications as a merger arb and held via GCI Liberty into Liberty Broadband. Offered it extra due to the chance value, reinvested these proceeds into extra present concepts.

- Digital Media Options (DMS) ended up rejecting administration’s buyout provide and as an alternative took on debt to make an acquisition, now it is buying and selling under a greenback. I need to imagine the existence of all these busted SPACs will finally flip into extra particular scenario kind alternatives, however these are questionable administration groups and it’d take a short time longer for administration and boards to totally come to their senses.

- Sonida Senior Residing (SNDA) disclosed a going concern warning, I discussed some place else that I outsized this place given the mixture of working leverage and monetary leverage, ought to have handled this extra as an possibility than a core place. Shares have recovered a bit, however they nonetheless face a difficult labor atmosphere and an absence of scale.

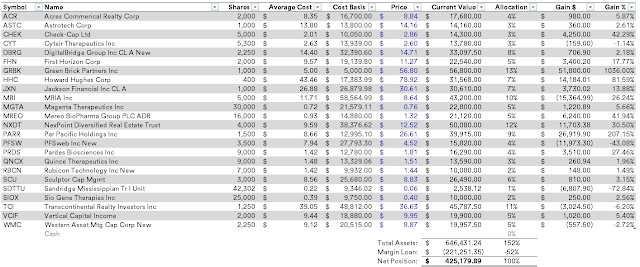

Present Portfolio

I do even have an assortment of non-traded securities (CVRs, liquidating trusts and a bond and not using a market) that I’ve omitted above. Thanks for persevering with to learn and observe alongside, additionally thanks to all which have despatched me concepts. Everybody please have a secure vacation.

Disclosure: Desk above is my taxable account/weblog portfolio, I do not handle exterior cash and that is solely a portion of my general belongings. Consequently, using margin debt, choices or focus doesn’t absolutely symbolize my danger tolerance.