{kind=link}

In instances of financial volatility, some sectors are extra resilient than others. Certainly one of them is the meals trade, as meals is in the end one among this stuff we HAVE to spend on.

That is clearly a really various sector, and this text will attempt to present an outline of the numerous potentialities for investing within the meals trade.

Greatest Meals Shares

We would purchase a automotive each 5 to 10 years, however we eat thrice a day. And even when instances are robust, meals is the very last thing we reduce on.

So let’s take a look at one of the best meals shares.

These are designed as introductions, and if one thing catches your eye, you’ll want to do further analysis!

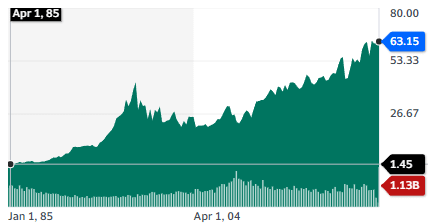

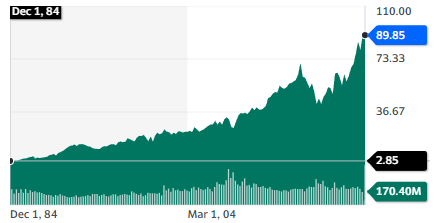

1. Coca-Cola (KO)

| Market Cap | $273.1B |

| P/E | 28.19 |

| Dividend Yield | 2.88% |

A well-known favourite inventory of Warren Buffett (Berkshire Hathaway owns 9% of KO) and an equally legendary compounding inventory. It has a wealthy historical past and even an array of city legends concerning the drink containing cocaine or how secret its method is.

Whereas the group takes its title from the well-known Coca-Cola drink, it’s now a large company holding a really giant array of 200 manufacturers and the world’s largest nonalcoholic beverage firm.

The corporate is licensing 225 bottling firms with 900 bottling vegetation to provide the ultimate merchandise from concentrates they purchase from KO.

Coco-Cola grew its incomes per share by 6% on common during the last 5 years, and free money movement rose by a median of 14% a yr. The corporate is commonly referenced as a stable instance of a inventory with a robust moat within the type of a model supported by a number of a long time of selling and product placement.

Revenues are extremely diversified and worldwide, with North America representing only a third of complete gross sales.

This inventory is just about as protected because it will get and likewise provides a modest however steady and rising dividend. So it’s principally favored by long-term buyers searching for security and a dividend reinvestment alternative.

2. Tyson Meals, Inc. (TSN)

| Market Cap | $17.8B |

| P/E | 11.99 |

| Dividend Yield | 3.83% |

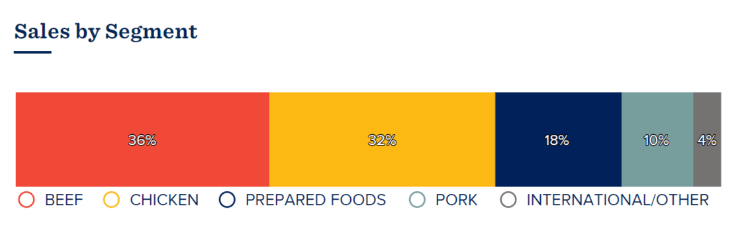

Tyson is one the most important meals firms on this planet and a frontrunner in protein. Tyson holds 33 completely different manufacturers, with lots of them recognizable by any American.

Many of the exercise comes from meat gross sales, with 2/3 being beef and rooster. Tyson can be investing in potential new sectors and rivals, like lab-grown meat and meat-free options, by its Tyson Ventures department. The identical Tyson Ventures can be investing in different improvements (robotics, carbon market, genomics) and leather-based manufacturing.

The corporate gave a warning that Q2 2023 could be “more difficult” than Q1, with “All three protein classes impacted by unfavorable market situations

concurrently.” So it appears that evidently the looming recession and rising rates of interest are affecting People’ spending on meat.

Rising commodity costs, together with for animal feed, haven’t helped both.

Whether or not it is a sturdy challenge or a short lived hiccup will decide if the inventory is undervalued or not at 2023 costs. Nonetheless, the corporate is planning worldwide expansions, with 11 new vegetation deliberate to open within the subsequent two years.

Tyson Meals is a inventory that can entice buyers assured within the long-term recognition of meat merchandise and considering shopping for it at a (short-term?) lower cost and holding it for a few years.

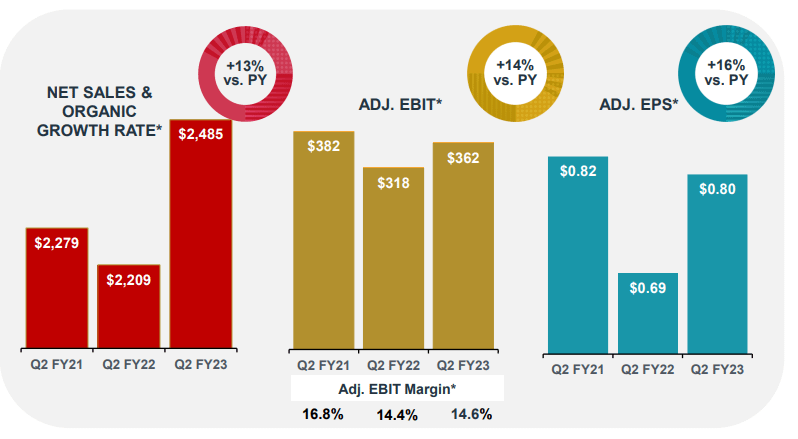

3. Campbell Soup Firm (CPB)

| Market Cap | $16B |

| P/E | 19.70 |

| Dividend Yield | 2.78% |

Whereas the corporate began within the soup enterprise, it’s now producing 15 meal and beverage manufacturers and 9 snack manufacturers. It makes a speciality of premade meals and comfort meals.

Among the manufacturers had been obtained by acquisition, notably the massive collection of snack manufacturers of Snyder’s-Lance, Inc. in 2018 and Pacific Meals in 2017.

Campbell is targeted on North America solely and registered outstanding gross sales development in 2022. Earnings are extra unstable on account of rising enter prices, a recurring theme within the meals trade in 2022 and 2023.

Whereas it lacks the scale and development profile of KO, it shares a whole lot of similarities with Buffett’s favourite inventory. The corporate has a historical past of profitable model launches or acquisitions and has confirmed to be a top quality compounder. Its smaller measurement additionally would possibly give it extra room to continue to grow.

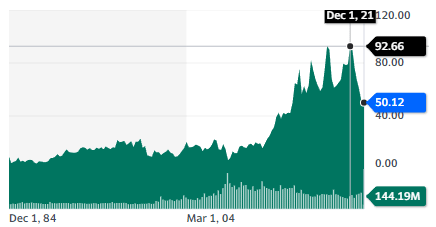

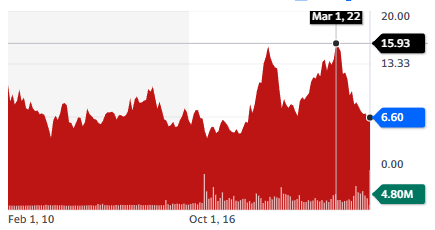

4. JBS S.A. (JBSAY)

| Market Cap | $7.3B |

| P/E | 2.38 |

| Dividend Yield | 11.75% |

The Brazilian chief in meat manufacturing, JBS is a bigger firm than its market capitalization would recommend. It controls 150 manufacturers, as properly the manufacturing of leather-based, biodiesel, cleaning soap, purified components, provides for the pharmaceutical trade, packaging, a buying and selling division, and a logistics fleet of 1,100 vans.

It’s the world’s largest beef producer, rooster producer, and second to largest pork producer. Additionally it is the second-largest salmon producer in Australia. It’s the main producer of plant-based meat options in Brazil and the third-largest in Europe. It’s additionally in first place for ready meals within the UK, Australia, and New Zealand and second in Brazil.

By income, JBS is bigger than the better-known recognized Nestle, Pepsico, or Tyson.

The corporate has been hit by decreased meat consumption in the identical manner as Tyson Meals, but in addition by the commonly adverse outlook of markets about Brazil since President Lula’s election.

JBS is appropriate for buyers prepared to deal with a whole lot of worldwide threat and volatility in alternate for a really low valuation as measured by P/E and dividend yields.

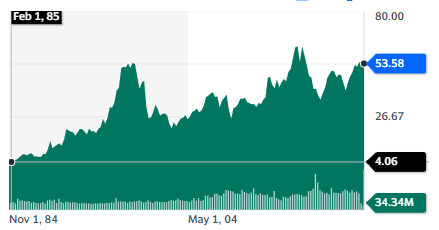

5. Normal Mills, Inc. (GIS)

| Market Cap | $52.8M |

| P/E | 19.49 |

| Dividend Yield | 2.39% |

Normal Mills is one other family title with 46 manufacturers, together with Cheerios, Cocoa Puff, Haagen Dazs, Outdated El Paso, and Yoplait, and even pet meals with Blue Buffalo.

The corporate has grown, year-to-date in 2023, working income by 11% and earnings per share by 14%. The corporate is taking a look at an enhancing 2023 outlook of 8-9% EPS development.

General, regardless of inflationary strain, Normal Mills appears to be dealing with the macroeconomic setting fairly properly.

Money redistributed to shareholders is available in 2 varieties, in dividends but in addition the identical quantity in share repurchases for 2022. So contemplating each, the actual yield of the corporate is way greater than the seen 2-3% dividend yield.

This inventory has the profile of a high-quality meals inventory, with extremely precious manufacturers and a compounding inventory value. And its compounding profile during the last 4 a long time is outstanding and moderately equal to KO, even whether it is much less mentioned.

6. The Kraft Heinz Firm (KHC)

| Market Cap | $47.7B |

| P/E | 19.85 |

| Dividend Yield | 3.98% |

Kraft is a widely known maker of sauces, ketchup, and “simple” meals like Mac & Cheese.

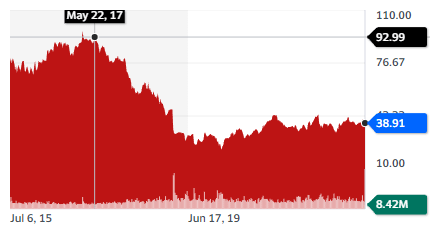

Additionally it is an organization that received into hassle in 2019 when it wrote off $15B in worth for underperforming manufacturers. The scenario was blamed on a failure to innovate and poor technique focusing an excessive amount of on closely processed and unhealthy industrial meals.

This was additionally on the time when “new meals” had been anticipated to take over the market by storm.

The corporate has confronted many challenges, together with accounting points, the resignation of its CEO and a slide in gross sales and earnings as individuals look to eat fewer closely processed meals and embrace plant-based merchandise from the likes of Past Meat (BYND) and Not possible Meals.

Considerations may need been exaggerated, even when the inventory continues to be to recuperate. For instance, the “ongoing enterprise development” section (manufacturers which were stored since 2019) has managed a 9% CAGR. The “energize” section noticed a 6% CAGR since 2019, and the “stabilize” section has been flat at 0%.

gross sales numbers, it’s onerous to completely see an organization a lot much less precious in 2022 than in 2019.

The brand new administration is centering the corporate round two segments, which makes a whole lot of sense for a meals enterprise. Style, with numerous sauces, and comfort, with simple and quick-to-make meals.

This renewed focus ought to assist the corporate make higher strategic selections and restart development.

Kraft just isn’t for each investor, because the final 3-4 years’ inventory efficiency has been abysmal in comparison with its rivals. However it is usually an organization that appears to have been radically energized and reformed by the disaster. So it may very well be a turnaround story with much more development potential than what the markets are pricing in.

Greatest Meals ETFs

If you happen to choose to have publicity to the sector as an entire, there are a number of food-focused ETFs accessible.

1. First Belief Nasdaq Meals & Beverage ETF (FTXG)

This ETF has a deal with the most important firms, with the highest 5 holdings representing 40% of the entire ETF: Mondelez, Normal Mills, PepsiCo, Coca-Cola, and Archer-Daniels-Midland.

2. Invesco Dynamic Meals & Beverage ETF (PBJ)

This ETF invests within the 30 largest firms within the meals sector (Mondelez, Normal Mills) in addition to in drinks (PepsiCo, Molson Coors) in addition to agriculture (Archer-Daniels-Midland).

3. VanEck Way forward for Meals ETF (YUMI)

This ETF is targeted on meals and agricultural improvements. Its high 4 holdings are Ingredion, Corteva, Deere & Co, and Novozymes. It incorporates fertilizer shares as properly, like Nutrien. It’s a nice ETF for buyers searching for publicity to the sector past client manufacturers.

Conclusion

Meals is a really worthwhile sector, particularly when supported by sturdy manufacturers. Habits and advertising could make one particular person a lifetime client of this particular product. This is among the principal causes behind the sturdy historic efficiency of meals shares.

With this inventory record, it’s doable to construct a portfolio gathering lots of of high-quality manufacturers by confirmed compounded shares, along with a low-digit dividend yield. And with potential turnarounds like Kraft-Heinz or hammered-down international shares like JBS, it is usually doable to extend yields.