{kind=link}

Fast Inventory Overview

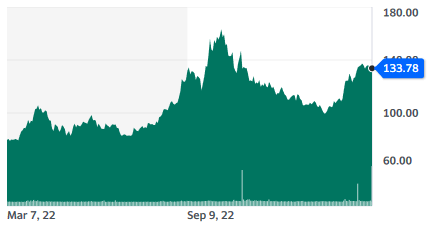

Ticker: CLCO

Supply: Yahoo Finance

Key Information

| Trade | Power / Transport |

| Market Capitalization ($M) | 687 |

| Worth to gross sales | 4.26 |

| Worth to Free Money Movement | 5.97 |

| Dividend yield | 3.05% (12.5% annualized) |

| Gross sales ($M) | 161 |

| Free money stream/share | $4.18 |

| P/E | 16.4 |

1. Govt Abstract

The Ukraine conflict has put a highlight on the hazard of Europe’s dependence on Russian power provides. That is very true for pure fuel, which the EU consumes in large quantities to energy it’s electrical grid, run its industries, and keep heat in winter.

The pipeline fuel that Europe acquired from Russia was cheap, however a pipeline can solely transfer fuel from one supply, and Russia’s political instability makes dependence on Russian fuel unacceptable. LNG terminals make a great various. An LNG terminal can obtain fuel from wherever, avoiding the issue of being tied to a single provider.

This led to a flurry of development geared toward constructing infrastructure to obtain and course of LNG. This leaves one unsolved chokepoint that’s little mentioned: LNG transport.

LNG can solely be shipped on specialised vessels, and the present fleet will not be dimensioned for the sudden surge in European demand. On the identical time, shipbuilding capability will not be ready so as to add new provide shortly, as it’s already working at 100% capability after many shipyards went bankrupt within the 2010s.

Worse, new air pollution laws are forcing the retirement of a big portion of the prevailing fleet.

This offers a novel alternative for CoolCo, a pure play in LNG transport. Its fashionable fleet is unaffected by air pollution laws. Its ships will be capable to seize a lot of the upside when consumers outbid one another to acquire treasured provides forward of the approaching winters.

2. Prolonged Abstract: Why CoolCo?

The Not-Over Power Disaster

The Ukraine conflict has dramatically elevated Europe’s want for LNG. This has dramatically elevated international demand, as Russia’s pipeline fuel can’t be redirected elsewhere for years. 75% of Russia’s fuel pipeline internet runs to Europe, and the prevailing pipelines to Asia can carry solely a small fraction of Russia’s output.

This created a logistical nightmare for the EU.

The Coming Provide Chokepoint

Gasoline and LNG producers are increasing capability as quick as they’ll. The EU has additionally rushed new services to course of and acquire this provide. However transport is a chokepoint that can not be solved as simply. Restricted transport capability is resulting in growing day charges, multiplying the margins of LNG transport corporations.

CoolCo

CoolCo is among the solely publicly traded pure-play LNG carriers. It operates a contemporary fleet that may profit from its rivals being pressured to retire vessels on account of new stringent air pollution laws. Growing transport day charges might carry its Free Money Movement to Fairness as much as a 30-50% yield.

Financials

CoolCo has rising revenues, revenue, and money flows. It has some debt, however most reimbursement is scheduled for 2025 and 2027. Its coverage may be very shareholder pleasant, with most free money stream distributed in dividends and anticipated double-digit dividend yields.

A New Itemizing

CoolCo filed for a direct itemizing on the NYSE on February 14, 2023. The Firm accomplished the regulatory course of on March 10 and requested the SEC to declare its registration efficient on March 14.

The registration has been authorised, and CoolCo shares commenced buying and selling on the NYSE on March 17, 2023, below the image CLCO. Buying and selling on the Oslo trade will proceed.

Up till this time CoolCo has traded on the Oslo Euronext Development trade in Norway, limiting entry for US traders and limiting the inventory’s visibility and profile.

This report first appeared on Inventory Highlight, our price investing publication. Subscribe now to get analysis, perception, and valuation of a number of the most attention-grabbing and least-known corporations available on the market.

Subscribe immediately to hitch over 9,000 like-minded traders!

3. The Not-Over Power Disaster

EU Gasoline Starvation

In January 2022, the EU was blissfully unaware of the approaching conflict in Ukraine. The sudden Russian invasion has pressured all of Europe to rethink its enterprise with Russia.

On the middle of the connection was the sale of power, particularly fuel. In the course of the Chilly Warfare, the USSR developed an intricate community of pipelines to hold fuel from its Siberian fuel fields to its conquered Japanese European vassals. It additionally exported fuel to West Germany, Italy, and Austria.

With the autumn of the Berlin wall, the connection deepened. Russia desperately wanted the laborious forex the sale of fossil gasoline would carry, and Europe’s business benefited enormously from a budget power provide.

This fuel provide was an enormous a part of the German success in heavy industries, from automobile manufacturing to the chemical and pharmaceutical industries. Most of this fuel was imported, with home manufacturing in regular decline and Norwegian manufacturing stagnating.

In recent times, fuel has additionally change into the principle answer for a clean power transition. Gasoline is way much less carbon-intensive y than coal or oil, so it grew to become a central a part of holding the lights on and homes heat in Northern Europe.

Gasoline energy crops are additionally extraordinarily reactive and may be powered up or down in a matter of minutes. This made them the proper candidate for pairing with carbon-neutral however unstable renewables like wind and photo voltaic. Each time the solar doesn’t shine, or the wind doesn’t blow, fuel energy crops can decide up the slack.

A Modified European Power Panorama

The assault on Ukraine has put Europe in a troublesome place. On one aspect, it’s extensively thought of unacceptable to maintain financing the Russian state and navy, particularly with NATO sending an enormous quantity of weapons to Ukraine.

On the identical time, your complete power infrastructure of Europe, and particularly of Northern Europe & Germany, was extremely reliant on Russian pipelines. So an immediate interruption would have doubtless introduced down the ability grid and carried out dramatic injury to the EU economic system. As soon as once more, counter-productive when it is advisable produce weapons and maintain the economic system afloat.

With the Nord Stream pipeline sabotaged and the battle escalating additional, Russian fuel is just about out of Europe.

That is most essential for fuel. Oil is one other product the EU purchased in giant quantities from Russia, however oil tankers are extra quite a few and are simpler to redirect. Gasoline is, effectively, a fuel, so it’s troublesome to hold it over lengthy distances.

The one 2 choices are pipelines and LNG.

The likelihood for additional provide to Europe by pipeline is just about maxed out, as pipelines from Algeria or the Center East are already working at full capability.

LNG stands for Liquefied Pure Gasoline. It’s virtually at all times costlier than pipeline fuel, because it requires the fuel to be became an ultra-cold liquid. However as a result of it’s carried in large tanker ships, its provide is much more versatile. As a living proof, plenty of China-bound American LNG shipments rotated mid-journey when rising European costs made it well worth the hassle.

The state of affairs is even worse for Russia. If it’s not promoting its fuel to Europe, it could actually’t promote in any respect. Russia lacks the infrastructure to move fuel to Asia in giant portions, and can doubtless have to cut back its gross sales quantity by 50% or extra. This could be modified by constructing pipelines towards China, however this can take a few years and even many years.

For instance, the prevailing Russia-China pipeline, Energy Of Siberia, connects to just one Russian fuel area, and its most capability is barely 5.4% of Russia’s output. POS 2, a bigger community, is scheduled for completion in 2030 and can carry one other 8.7% of Russia’s output. Mixed, these pipelines will solely carry 14.1% of Russia’s present output.

So Russian fuel can not redirect its fuel output elsewhere, prefer to India or China. This implies that demand for LNG will probably be elevated for many years to come back.

Quantifying the New Gasoline Provide

Pre-war Russian fuel provide to Europe was 150 billion cubic meters per yr. When this provide grew to become unsure, hypothesis and concern of scarcity prompted a skyrocketing value for EU fuel, equal to $400/barrel of oil at one level.

To present some perspective, in 2021, the world’s complete LNG provide was standing at 450 billion cubic meters. So changing the Russian fuel provide with LNG is an enormous enhance in demand in a single day.

With plenty of effort, the EU has managed to diversify away its fuel provide from Russia. It was not with out prices, because the EU power disaster is estimated to price a complete of 1 trillion {dollars} … up to now.

However, fuel storage is at an all-time excessive and near the utmost. A particularly delicate winter has additionally helped loads, as a lot of EU power consumption is from coping with the winter surge in demand.

A part of the success of the EU find sufficient fuel got here from the intense costs of final summer season. In a nutshell, it outbid anybody else, particularly poorer nations. This prompted all types of points in nations like Pakistan, which suffered large energy outages and power shortages (“Pakistan’s dependence on pure fuel is popping right into a nightmare“).

Not Over But

Another excuse the EU managed to get sufficient fuel, past paying loads and a gentle winter, was China’s harsh lockdown coverage, which constrained LNG demand. It’s in all probability not going to be that straightforward in 2023, with Chinese language consumption ramping up shortly. This may maintain demand for LNG excessive, as both China or Europe will want it sufficient to maintain shopping for at virtually any value.

Even with fuel costs within the EU quickly down, demand is ramping up, each in Europe and in rising nations.

As a result of the worldwide demand for LNG has shot up, there may be loads of contemporary provide developing as quick as doable.

So whereas we would see a robust LNG value for just a few years, LNG oversupply would possibly occur as quickly as 2025-2026. It’s because Qatar is ramping up manufacturing, the USA is growing its export capacities, and Mozambique is launching its first exports.

If Iran reaches an lodging with western nations and sanctions are lifted, one other main fuel provider will enter the market.

North America may be very wealthy in fuel and solely restricted by its export infrastructure. USA’s important export facility, Freeport, continues to be on partial standby. But it surely ought to be getting again on-line quickly.

Demand volumes will keep excessive, however LNG costs would possibly fluctuate extensively, and go down from 2025-2026 onward, which can solely stimulate demand additional.

This makes a guess on LNG producers or liquefaction services difficult for traders.

There’s over a trillion {dollars} of pure fuel infrastructure being constructed on the earth immediately. There’s a set secular shift and pure fuel that’s right here to remain.

CEO of LNG exporter Cheniere Power Jack Fusco

As a substitute, this report will talk about an typically uncared for however important step between the fuel producer and shopper, which is way much less prone to see a collapse in costs and earnings in 2-3 years: transport.

4. The Coming Provide Chokepoint

A Easy Enterprise

Power transport is a quite easy enterprise mannequin. An oil & fuel firm produces in place A and desires to maneuver its product to a shopper in place B. It hires a specialised firm to take action, utilizing devoted ships custom-built for this goal: oil tankers or LNG carriers.

This can be a enterprise completely pushed by provide and demand. Transport corporations will choose to get the ships shifting it doesn’t matter what, as an idle ship prices virtually as a lot as a employed one. If there are too many ships for too little cargo, the day price for transportation is barely or beneath prices.

Alternatively, if there will not be sufficient ships, day charges can explode, as transport is barely a small a part of the worth of the cargo. Paying loads for transport makes extra sense than being unable to promote the fuel or oil.

As a consequence of geopolitics, the demand for LNG will keep elevated for years, perhaps as a lot as 10-15 years. The EU will want that lengthy to begin constructing extra renewable and nuclear energy crops, and even then, fuel will probably be wanted as a backup for renewables.

China can be trying to constantly change a few of its coal capability with environmentally cleaner fuel energy crops.

So we all know that demand will probably be excessive for the foreseeable future. Because of this, appropriately forecasting the provision of LNG transport is all we want.

The Provide Chokepoint

The availability chain of LNG may be shortly summarized:

Gasoline effectively -> pipeline -> liquefaction -> LNG ship -> regasification -> distribution

The steps “Gasoline effectively -> pipeline -> liquefaction” have already got an honest and rising provide.

The EU has additionally rushed to construct as many new LNG regasification services as doable. Because of this, the just about saturated regasification capability in 2022 now has spare capability in 2023. With nonetheless some extra in development and coming on-line quickly, this is not going to be the limiting issue for EU’s LNG imports.

This leaves the transport a part of the provision chain unresolved.

The wonderful thing about transport as an funding is that it’s straightforward to forecast future provide. We all know precisely what number of ships are at sea, and it takes years for a shipyard to provide a brand new ship. So by trying on the (well-known and tracked) order e book of shipyards, we are able to forecast the long run provide.

The 2014 crash in power costs (from shale oil and fuel overproduction) had a drastic influence on the transport business. Nearly no new orders got here in for 3 years, and plenty of corporations went bankrupt.

So there may be little or no ship-building capability on the earth proper now, particularly for the extremely specialised LNG carriers. Worldwide, all shipyards in a position to manufacture LNG ships are totally booked till 2027. There isn’t any probability of a sudden surprising surge in LNG transport capability.

A superficial look would possibly allow you to assume plenty of ships are coming on-line, which might crash day charges. However this isn’t totally true, as plenty of the ships at present working are from earlier than 2002, and are getting retired as a result of they’ll’t adjust to present environmental requirements set by the Worldwide Maritime Group (IMO).

Air pollution Rules

The brand new 2023 IMO Sulfur laws will influence older designs (steam turbine sorts, in red-orange within the graph above).

When the regulation comes into pressure in lower than two years, many VLGCs will rush into shipyards to make enhancements to their power effectivity. Commonest modifications will probably be set up of power saving gadgets, or to put in Engine Shaft Energy Limitation (ShaPoli) and/or Engine Energy Limitation (EPL) system, which is used to decrease the utmost pace of the vessels.

Which means that the oldest ships should be both retired or completely retrofitted with new engines. Some others will should be upgraded with air pollution scrubbers. And lots of others should journey slower, decreasing complete transport capability.

Total, the newly constructed ships within the subsequent few years will barely compensate for the retiring older designs. And keep in mind that no additional provide than the prevailing shipyard backlog may be added for that interval.

So the full fleet dimension will keep stagnant for a few years, unable to develop in synch with demand.

👉 In case you are curious, you possibly can study all concerning the intricacies of various LNG ships at this hyperlink.

The consequence of rising demand and restricted/fixed provide is a direct and chronic rise in transport charges. And this was earlier than Freeport – the biggest LNG export facility within the US – resumed operations.

The US has been the world’s largest LNG exporter since 2022, and Freeport’s outsized liquefaction complicated restarting will enhance the demand for ships in a position to carry its manufacturing. US fuel producers will probably be glad to export as a lot as bodily doable, because the US fuel costs are a lot decrease than the Asian and European ones.

Briefly, transport charges rely on international demand. In need of Europe (or the world at giant) getting into right into a catastrophic despair, the elevated demand for LNG ought to persist.

5. CoolCo

A Uncommon LNG Pure Participant

In commodity and cyclical companies, a certain signal of a flip available in the market cycle is when corporations are turning extra worthwhile, and are taken personal by the bulk shareholders. It’s because typically, share costs will not be (but) rising a lot, however operators can see the writing on the entire, and snatch the corporate at an affordable value.

And like clockwork, Höegh LNG, a pure transport play, was lately taken personal.

Such pure performs in LNG transport are uncommon. There are a whole lot of LNG ships crossing the seas, however most are owned by small subdivisions of transport giants, the place LNG is 2-10% of the entire enterprise. This makes LNG day charges largely irrelevant to the general enterprise and the inventory value.

So CoolCo is quite distinctive to my information in being a publicly listed, pure LNG provider play. The corporate has additionally very lately been listed on the NYSE along with its native Oslo itemizing, making it loads simpler for US traders to purchase shares.

Enterprise Overview

The corporate is owned at 58.2% by Japanese Pacific Transport, and the remainder of the shares are publicly traded. Japanese Pacific is among the largest personal transport corporations on the earth. Contemplating the latest itemizing within the NYSE, there is no such thing as a indication that Japanese Pacific is trying to take CoolCo personal.

CoolCo operates 12 LNG carriers, a contemporary fleet with a median age of solely 7 years. 4 of those ships have been purchased lately (November 2022), after the sale of 1 older vessel, and it has an choice on 2 ships below development, with supply anticipated on the finish of 2024.

The Firm additionally manages and operates 17 LNG infrastructure models for different corporations, together with former associate Golar LNG and New Fortress Power, principally floating storage and floating regasification models. Whereas this generates some revenue and cultivates business connections, this isn’t the core of the corporate revenues.

Bettering Circumstances

In 2022, the TCE (Time Constitution Equal, or basically revenue per day per ship) was round $69,800; within the final quarter, it had risen to $83,600.

The corporate is aiming for the entire fleet to achieve the $120,000-$140,000 vary, one thing already achieved for 4 ships (out of 12) and anticipated for 4 extra quickly.

You may see beneath the anticipated fairness yield if the entire fleet was chartered at these costs.

And that’s just about all to be mentioned about CoolCo operations.

The enterprise is hyperfocused on LNG carriers. The funding thesis depends on day charges staying excessive or rising.

So returns from CoolCo will rely on two components: the day price ranges and the present valuation.

6. Financials

Concentrate on Money

The corporate will not be a long-term progress play as a result of business’s cyclicality. As a substitute, the main focus is on earnings from the present rise in day charges and CoolCo’s capacity to seize this pattern.

The corporate generated $115M in free money stream final yr.

Revenues have been $90M in This autumn 22. Web revenue within the final quarter was $33M, and EBITDA was $42M.

It’s price noting that CoolCo was IPOed solely in March 2022, so the financials are a bit difficult. At one level CoolCo shared possession of most of its LNG vessels with Golar, making the accounts quite complicated.

The latest buy of 4 ships in November 2022 doesn’t make it easier, as they aren’t exhibiting within the final quarterly report. The latest $120,000/day constitution price can be not totally mirrored.

So total, each money stream and earnings talked about above are prone to be considerably beneath the final reported degree, however we are going to want the following quarterly report back to have a greater estimate.

Therefore I choose to check with This autumn 22 for the newest earnings, as they finest symbolize the corporate shifting ahead.

Stability Sheet

On the finish of 2022, Web debt was $1.1B, with “solely” $129M in money.

The common rate of interest was 5.65%. Rate of interest threat is hedged at 83%, so rising rates of interest shouldn’t be a risk to CoolCo. If something, if curiosity and/or inflation have been to rise, it might assist it neutralize a part of its debt.

Debt maturity can be quite good, with the majority of it scheduled for 2025 and 2027.

That is removed from a pristine steadiness sheet, but additionally not a dramatic downside for a corporation with capex-heavy industrial belongings. Total, dangers from the steadiness sheet and debt appear comparatively restricted and would solely materialize in case of a collapse of day charges.

Administration additionally appears conscious of the chance and is cautious to not let the debt put the long run money flows of the corporate in danger, utilizing a conservative hedging technique.

Valuation

CoolCo is at present valued at $687M.

With a P/E of 16, it’s fairly valued relative to earnings.

The price-to-free-cash-flow ratio is a low 5.97.

As well as, the free money stream reported on the finish of 2021 fails to incorporate the additional 4 ships lately acquired, and far greater day charges and TCE within the final quarter.

So I might guestimate the present value to free money stream is even decrease (3 to 4?), relying on price management and the working prices related to the acquisition of the 4 new ships.

We appear early within the day price cycle, and the cycle is prone to final for much longer than regular, as a result of EU’s geopolitical incentive to remain off Russian fuel. The underlying pattern of coal-to-gas swap in China, India, and elsewhere helps as effectively.

So the present valuations are nice if the corporate returns money to shareholders.

With transport a really cyclical business, you will need to have an organization distributing earnings in good instances, as an alternative of increasing too aggressively and ending the rising a part of the cycle with large extra capability.

Returns to Shareholders

The corporate is anticipating a Free Money Movement on Fairness (FCFE) yield of 23% in 2023, assuming a spot day price of $91,000. To check, in 2022, the FCFE was standing at 15%.

The corporate’s administration targets to return a lot of the free money stream to the shareholders. So solely the choices on the two newly constructed ships for 2024-2025 beforehand talked about ought to devour money, with the remainder of the money generated being redistributed.

CoolCo lately (tenth March 2023) distributed a dividend of $0.40/share, giving it a dividend yield of 3%.

With a present valuation of $12.8/share, the identical dividend each quarter would carry the annual dividend yield to 12.5%, and could be according to administration forecasts.

7. Conclusion

CoolCo is an organization that might usually should be buying and selling at a deep low cost to be attention-grabbing, like a single-digit P/E and a beneath 4 price-to-free money stream ratio.

It’s because transport enterprise cycles are quick and may present brutal downturns. So with a P/E of 16 and a few debt, CoolCo could be a bit too costly if the cycle was to show unfavourable within the subsequent 12-18 months.

The distinction from the traditional enterprise cycles of the previous is the Ukraine conflict and the rising tensions between the West and Eurasian powers. These components elevated the worldwide demand for LNG by 30% virtually in a single day, a rise that isn’t short-term however structural. So this cycle is to be anticipated to final abnormally lengthy, at the least 5 years, and probably 10-15.

Since 2022, the LNG business has tried to reply and is managing fairly effectively when it comes to manufacturing, liquefaction, and regasification. However the diminished international shipbuilding capability leaves transport because the weak hyperlink within the chain and the one with essentially the most enduring pricing energy.

Being one of many solely pure gamers publicly traded, CoolCo is prone to entice much more consideration following its latest NYSE itemizing.

The present value is enticing, and administration appears targeted on redistributing revenue to shareholders. With the curiosity of the principle shareholders aligned with the minority shareholders, we are able to anticipate CoolCo to be a stable revenue inventory and supply some inflation safety as effectively.

Holdings Disclosure

Neither I nor anybody else related to this web site has a place in CLCO or plans to provoke any positions inside 72 hours of this publication.

I wrote this text myself, and it expresses my very own private views and opinions. I’m not receiving compensation from, nor do I’ve a enterprise relationship with any firm whose inventory is talked about on this article.

Authorized Disclaimer

Not one of the writers or contributors of FinMasters are registered funding advisors, brokers/sellers, securities brokers, or monetary planners. This text is being supplied for informational and academic functions solely and on the situation that it’ll not type a main foundation for any funding choice.

The views about corporations and their securities expressed on this article mirror the non-public opinions of the person analyst. They don’t symbolize the opinions of Vertigo Studio SA (publishers of FinMasters) on whether or not to purchase, promote or maintain shares of any specific inventory.

Not one of the data in our articles is meant as funding recommendation, as a suggestion or solicitation of a suggestion to purchase or promote, or as a advice, endorsement, or sponsorship of any safety, firm, or fund. The knowledge is basic in nature and isn’t particular to you.

Vertigo Studio SA will not be accountable and can’t be held chargeable for any funding choice made by you. Earlier than utilizing any article’s data to make an funding choice, you need to search the recommendation of a certified and registered securities skilled and undertake your individual due diligence.

We didn’t obtain compensation from any corporations whose inventory is talked about right here. No a part of the author’s compensation was, is, or will probably be immediately or not directly associated to the precise suggestions or views expressed on this article.