{kind=link}

Power is a basic want, and industrial societies eat it in gargantuan and ever-increasing portions. This constant demand makes the sector enticing to buyers, significantly these in search of the perfect power shares so as to add to their portfolios.

The power sector has been out of favor for a very long time, with buyers preferring the excessive development potential of the tech sector. The sector rotation from bits (tech, software program) to atoms (manufacturing, mining, power) is likely to be solely getting began, given the comparatively low P/E ratios and excessive dividend yields provided by many power shares.

Finest Power Shares in 2023

The power sector could be very various, together with renewables, oil, gasoline, coal, and nuclear, together with useful resource extractors, utilities, service suppliers, producers, and extra. The profiles of main corporations range, with focuses on development, returning revenue to shareholders, and growing new applied sciences.

So, let’s have a look at a number of the greatest power shares.

This choice is concentrated on giving an outline of the sector and fascinating corporations in it, however can’t cowl all the things.

This checklist of the perfect power shares is designed as an introduction, and if one thing catches your eye, it would be best to do further analysis!

1. Petróleo Brasileiro S.A. – Petrobras (PBR)

| Market Cap: | $89.9B |

| P/E: | 2.54 |

| Dividend Yield: | 41.75% |

Petrobras, the nationwide oil firm of Brazil, is changing into more and more important on this planet of greatest power shares, as the corporate is on its technique to changing into the world’s 4th largest producer of oil.

The corporate has a profile with excessive contrasts. On one hand, the enterprise itself has carried out nicely, with steadily rising oil manufacturing and strong profitability, permitting for record-breaking dividend yields. The corporate is generally producing from offshore oil fields, with 3.74 boed (Barrels of Oil Equal per Day) in Q1 2023.

The corporate has additionally used this profitability to scale back its debt from $79B in 2019 to $37.6B in Q1 2023.

Alternatively, Brazil is a rustic with critical popularity issues amongst buyers, and the current election of socialist Lula to the presidency has spooked markets. Riots storming a number of authorities buildings by his opponent’s supporters didn’t assist both. Lastly, the prices of decarbonization plans and increasing petrochemical actions may scale back the corporate’s profitability in the long run.

So Petrobras is a superb oil firm IF the political scenario stays secure sufficient. And that might be a giant ‘if”. This could make any buyers cautious and seeking to diversify regardless of the good-looking dividend.

On the identical time, the dividend is massive sufficient that if Brazil stays collectively for even three years, an funding can be worthwhile primarily based on dividend yields alone!

🛢️ Be taught extra: Discover our current evaluation for an outline of notable oil shares and ETFs within the present market panorama.

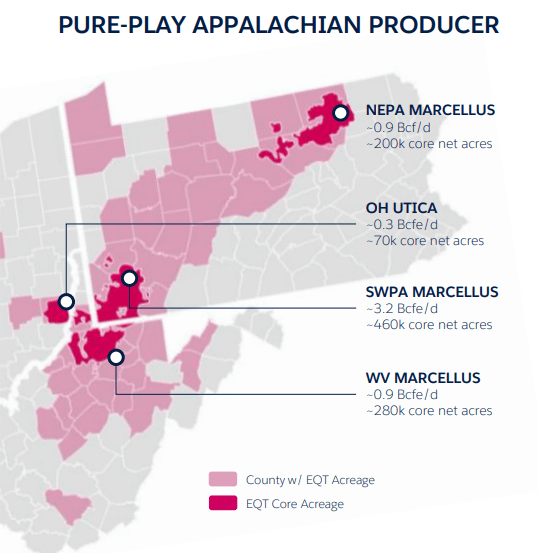

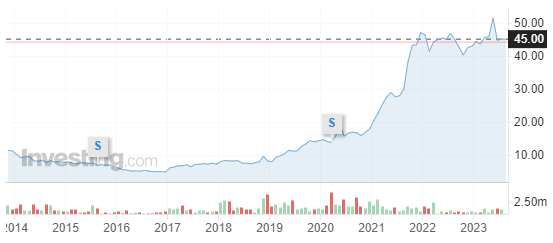

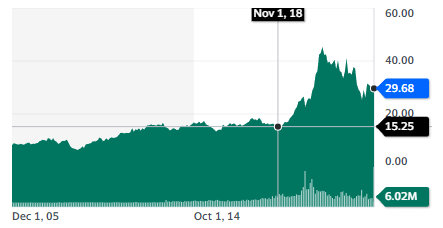

2. EQT Company (EQT)

| Market Cap: | $14.1B |

| P/E: | 3.38 |

| Dividend Yield: | 1.54% |

EQT is the main producer of pure gasoline within the US, with operations in Pennsylvania, West Virginia, and Ohio (Appalachian Mountains). Or as the corporate places it, “If EQT had been a rustic, it will be the twelfth largest producer on this planet of pure gasoline”.

Due to a heat winter and a softening of the worldwide power disaster, pure gasoline costs have gone down lots within the USA. Thus far, this has not damage EQT’s free money move era, which hit $774M in Q1 2023.

After a interval of pursuing development in any respect prices, like many of the remainder of the shale sector, EQT is now targeted on lowering debt ($1.5B by the top of 2023) and enhancing returns to shareholders, notably within the type of share buybacks ($1B in 2023).

EQT is likely one of the greatest power shares to think about should you’re betting on the continued growth in shale gasoline manufacturing. Its prospects look promising because of presently low gasoline costs within the US rebounding, coupled with a secure or rising world demand for LNG exports and industries from Europe relocating to the US.

3. S. N. Nuclearelectrica (SNN)

| Market Cap: | $2.9B |

| P/E: | 4.64 |

| Dividend Yield: | 11.9% |

The only nationwide operator for nuclear energy in Romania, Nuclearelectrica has one of many world’s greatest nuclear security data. It’s owned within the majority (82%) by the Romanian state.

The corporate depends on its Models 1 & 2 for energy manufacturing, which collectively have a nominal capability of 1.4 GW. Unit 1 must be refurbished from 2027-2029 to offer it with one other 30 years of operational life after that date. Unit 2 must be refurbished in the identical method after 2037.

The corporate can be planning to construct 2 new reactors, Models 3 & 4, which might convey Romania’s power combine to 36% nuclear and double Nuclearelectrica’s manufacturing. They’re anticipated to be commissioned by 2030 and 2031.

Lastly, Nuclearelectrica must be the primary European firm to implement the SMR (Small Modular Reactor) expertise, due to an settlement with US-based NuScale. This challenge ought to add 462 MW to Nuclearelectrica capacities. This challenge already has $275M in funding from a coalition of worldwide companions.

Nuclearelectrica is a really high-performance nuclear operator in a nuclear-friendly nation. It affords a beneficiant dividend and plans to increase its capability massively by the top of the last decade.

Due to the refurbishing of Models 1 & 2 and the brand new manufacturing deliberate, the corporate is rising as top-of-the-line power shares match for an revenue portfolio with a protracted holding interval, with secure baseload power manufacturing anticipated for the foreseeable future.

⚛️ Be taught extra: Perceive the up to date panorama of the nuclear world with our breakdown of the business and its key gamers. Uncover why nuclear is again within the highlight.

4. Brookfield Renewable Companions L.P. (BEP)

| Market Cap: | $13.2B |

| P/E: | – N/A |

| Dividend Yield: | 4.53% |

BEP is the renewable utility department of the asset administration big Brookfield. It holds $625B in belongings and manages 25 GW of energy manufacturing, with plans so as to add a staggering 110 GW of latest capability.

Its present manufacturing is a mixture of numerous renewables, with many of the deliberate growth being in photo voltaic.

In 2023, BEP bought 51% of Westinghouse (along with uranium miner Cameco), the main builder of nuclear energy crops in North America and a designer and elements & service provider for many of the West’s current nuclear energy crops.

BEP’s distribution to shareholders has grown by 6% yearly since 1999. Along with the inventory value development, it generated annualized returns of 16% for its shareholders in the identical interval.

BEP combines a deal with renewables, a newly added presence within the nuclear OEM (Authentic Tools Producer) enterprise, and aggressive power manufacturing development within the subsequent 5-10 years.

This makes it top-of-the-line power shares for buyers seeking to guess on the power transition and a speedy flip to a low-carbon power combine (together with nuclear) in Western international locations.

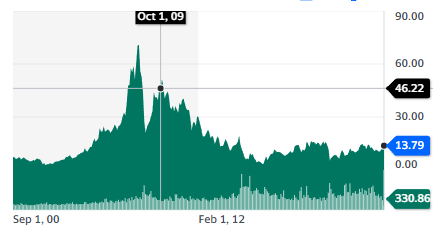

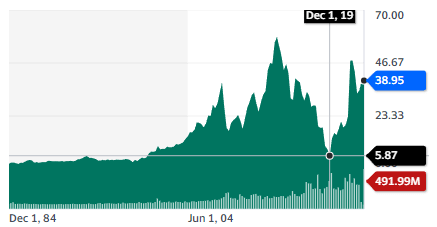

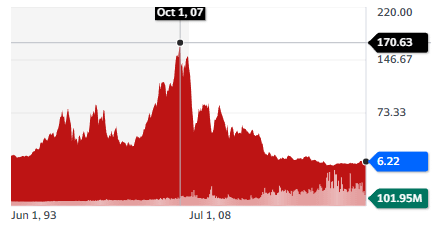

5. Transocean Ltd. (RIG)

| Market Cap: | $4.8B |

| P/E: | – N/A |

| Dividend Yield: | – N/A |

Whereas the entire power/fossil gas sector suffered within the 2010s, none did as badly because the oil & gasoline providers sector, particularly the offshore sub-segment. With oil & gasoline costs down, most producers lower severely on capital expenditure. And whereas onshore spending within the US remained sturdy with the shale revolution, only a few offshore initiatives had been authorised.

This led to a mass wave of bankruptcies in all the offshore drilling sector, affecting many corporations however not Transocean. At its lowest level, when the survival of the corporate was in query, the inventory fell to $0.67/share, or 1/253th of its peak worth in 2007.

With a deal with ultra-deepwater and newer era drillships, Transocean has persistently achieved among the many highest dayrates (the usual metric for the business) for brand new contracts in 2022.

The corporate now has an $8.5B backlog for future work contracts, twice that of the closest competitor. The corporate is presently targeted on repairing its stability sheet, in addition to placing a number of drillships that had been put in long-term storage (“chilly stacked”) again to work.

Transocean inventory is a guess on the continual want for brand new oil & gasoline assets, and particularly offshore assets, one of many lowest-cost sources of latest provide. When you’re seeking to diversify your portfolio, this might be top-of-the-line power shares to think about.

The most important threat can be a significant recession or some other occasion sending oil right into a sustained low value vary, which may hit the demand for offshore drilling. In such a situation, Transocean may wrestle to handle its nonetheless heavy debt load.

6. Peabody Power Company (BTU)

| Market Cap: | $2.9B |

| P/E: | 1.91 |

| Dividend Yield: | 0.37% |

Peabody is a coal miner with operations within the USA and Australia. When you’re considering the perfect power shares, understanding corporations like Peabody can provide invaluable insights. They produce a mixture of thermal coal (for energy manufacturing) and coking/metallurgical coal (indispensable for metal manufacturing, in inexperienced on the map under).

Thermal coal skilled a growth adopted by a bust through the 2022 power disaster. Costs have already risen again up in 2023. General, Peabody made a bit greater than half of its 2022 revenues from thermal coal.

2022 has proven that when going through power shortages, even international locations dedicated to lowering carbon emissions, like Germany, flip again to coal to maintain the facility grid secure. With the demand for power rising, it’s doubtless that coal will keep in demand for energy era, particularly in Asia and growing international locations.

There isn’t a prepared substitute for metallurgical coal in steelmaking, so its demand ought to keep secure consistent with total metal demand.

Resulting from these components, Peabody could be a good guess on the sturdiness of coal demand, whereas the market considerably dismisses the long-term worth of the corporate’s belongings, as illustrated by the low valuation multiples.

Nonetheless, buyers will have to be cautious. The corporate’s inventory has risen considerably since its 2020 lows, and coal markets are notoriously unstable, even when in comparison with different commodities.

ETFs (Alternate Traded Funds)

When you’re seeking to diversify your portfolio and contemplating a few of these greatest power shares we’ve featured above, you might also need to discover the sector as a complete. There are a number of energy-focused ETFs out there, offering totally different ranges of publicity to the varied segments of the power business.

1. Power Choose Sector SPDR Fund (XLE)

With a deal with “Huge Oil”, this ETF contains all the large worldwide fossil gas majors, like Exxon, Chevron, ConocoPhillips, and many others. It offers direct and diversified publicity to grease & gasoline manufacturing.

2. VanEck Oil Providers ETF (OIH)

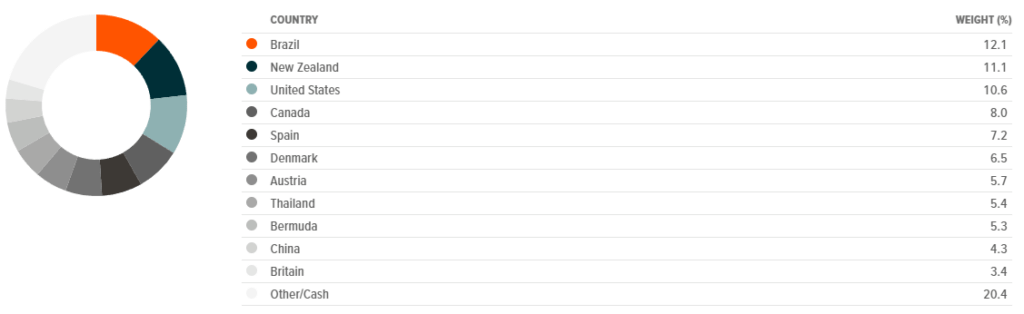

This ETF is concentrated on providers corporations for the fossil gas business. Its prime holdings are business leaders Schlumberger, Halliburton, and Baker Hughes. It additionally contains Transocean as its eighth largest holding. The ETF is primarily targeted on US-based corporations (90%), with solely 5% within the UK and 5% in Bermuda.

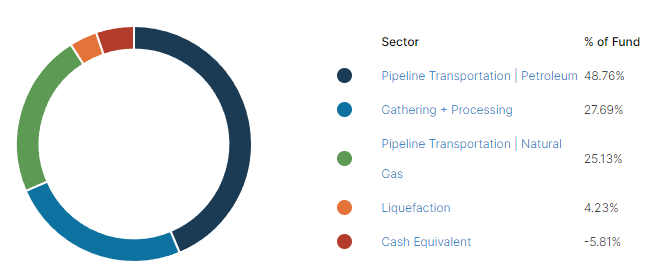

3. Alerian MLP ETF (AMLP)

This ETF is concentrated on the so-called mid-stream sector, the gasoline and oil pipelines that transport power all through the USA. It is a sector that tends to be much less unstable than power producers and in addition distributes beneficiant dividends, counting on its quasi-monopoly and the excessive worth of its transportation belongings.

4. World X Renewable Power Producers ETF (RNRG)

This fund is nearly solely investing in utilities producing energy by renewables. It is extremely geographically various and contains BEP in its sixth largest holdings, with the biggest holding being Danish wind farm chief Orsted.

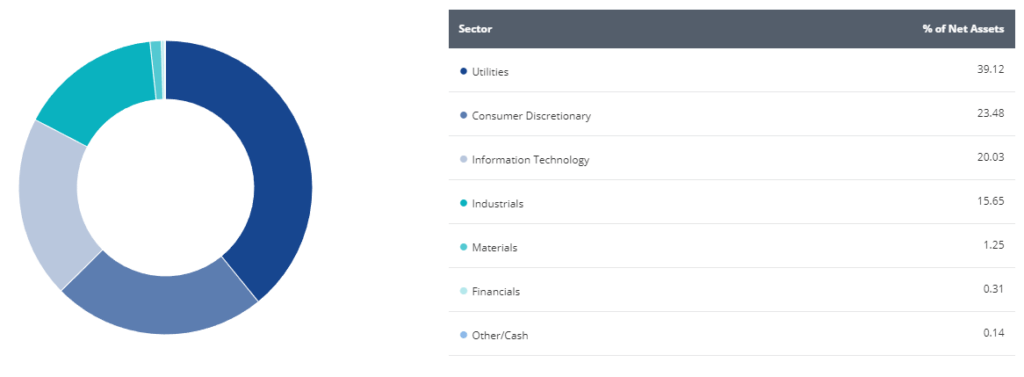

5. VanEck Low Carbon Power ETF (SMOG )

This ETF focuses on low-carbon power and is extra various than RNRG, with solely 39% invested in utilities. It additionally covers shopper items, IT, industries, and supplies with corporations like Tesla, Samsung Sdi, BYD, and First Photo voltaic.

6. Utilities Choose Sector SPDR Fund (XLU)

When you assume power will likely be in excessive demand however don’t have any opinion about the perfect power supply, XLU, with a big selection of utilities counting on hydropower, nuclear, fossil gas, and renewables, is likely to be greatest. Additionally it is doubtless to offer regular dividend revenue.

7. VanEck Uranium+Nuclear Power ETF (NLR)

This ETF offers publicity to nuclear energy total, from massive utilities to uranium miners and expertise corporations. It may be an excellent choose for buyers optimistic about nuclear power or in complement to different power ETFs.

Conclusion on the perfect power shares

Power is a fancy sector and can be a really worthwhile one. Additionally it is a really various business with many alternative profiles and applied sciences.

For that reason, buyers will both have to be taught lots a couple of particular sub-segment or take a diversified strategy to cowl the sector as a complete and discover the perfect power shares available on the market.

It’ll even be extremely really helpful to take an apolitical strategy, even when power, fossil fuels, nuclear energy, local weather change, and afferent applied sciences are usually very hotly debated matters. The long run power combine will most likely be as various as the present one, and an power portfolio ought to replicate this truth.