{kind=link}

6. Litigation & Monetary Outcomes

Is There a Downside?

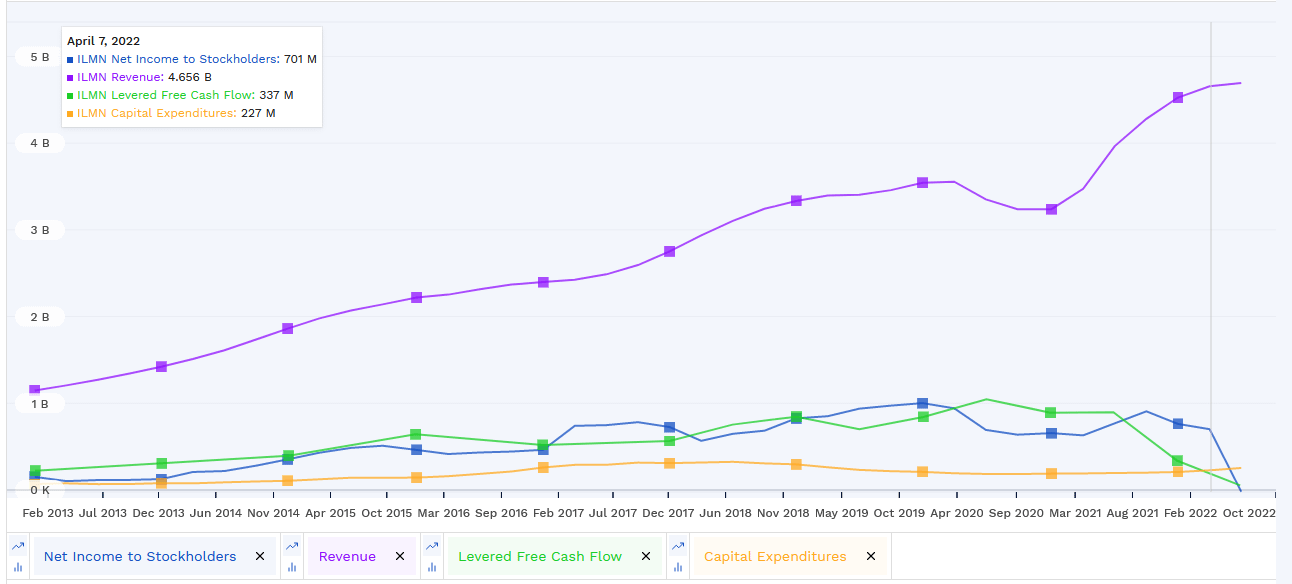

I’ve been watching Illumina for a very long time now, however for years its valuation was just too dear to make for a compelling funding. This grew to become much more true throughout the pandemic when each medical and bio inventory exploded upward. Illumina’s revenues jumped from $3.2B in 2020 to $4.5B in 2021.

Progress shares slowed down post-pandemic, and this has not been good for Illumina’s inventory worth. Shares have dropped 60% from their 2021 peak, erasing all of the pandemic positive aspects after which some.

Income progress has additionally slowed, reaching “solely” $4.7B TTM (Trailing Twelve Months).

Illumina’s CEO himself known as the Q2 2022 efficiency “disappointing“, attributable to macroeconomic headwinds. Gross margins dropped barely to 66% (nonetheless spectacular), and R&D spending rose massively, from $202M to $327M.

| GAAP | Non-GAAP (a) | |||

|---|---|---|---|---|

| {Dollars} in thousands and thousands, besides per share quantities | Q2 2002 (b) | Q2 2021 | Q2 2022 (b) | Q2 2021 |

| Income | $ 1,162 | $ 1,126 | ||

| Gross margin | 66.0% | 71.2% | 69.4% | 71.8% |

| Analysis and improvement (“R&D”) expense | $ 327 | $ 202 | $ 327 | $ 202 |

| Promoting, basic and administrative (“SG&A”) expense | $ 410 | $ 413 | $ 339 | $ 269 |

| Authorized contingencies | $ 609 | $ – | $ – | $ – |

| Working (loss) revenue | $ (579) | $ 187 | $ 141 | $ 338 |

| Working margin | (49.8)% | 16.6% | 12.2% | 30.0% |

| Internet (loss) revenue | $ (535) | $ 185 | $ 91 | $ 276 |

| Diluted (loss) earnings per share | $ (3.40) | $ 1.26 | $ 0.57 | $ 1.87 |

Supply: Illumina Q2 2022

So as to add to those short-term points, a cost of $609 million in authorized contingencies has been put apart, leaving the corporate registering a loss for the primary time in a decade.

Authorized prices as excessive as half of the quarter income may very well be an enormous purple flag, so let’s have a look at what occurred.

Grail’s Botched M&A

Grail is a biotech firm trying to develop an early most cancers take a look at utilizing Illumina’s NGS know-how. Having the ability to routinely test for most cancers by way of a blood take a look at (“liquid biopsy”) can be a real revolution, doubtless saving thousands and thousands of lives yearly.

Grail is at the moment enrolling individuals in a very huge scientific trial (1 million individuals), which might result in the take a look at being commercialized in 2 years.

Grail’s historical past is reasonably advanced. It was a spin-off from Illumina fashioned in 2016 as a separate firm. It has since raised $2B, together with from Jeff Bezos and Invoice Gates. Illumina nonetheless held 14.5% of the Grail shares.

Illumina then determined to purchase again the entire of Grail, for the hefty sum of $9.7B.

The acquisition was supplied half in money and half in Illumina’s shares. I thought-about {that a} good possibility, and would even have welcomed a bigger debt element, as Illumina has little or no debt (whole liabilities are just a bit increased than its $2.9B in present property).

Nonetheless, I’ve to query what went improper, contemplating that Illumina ought to clearly have saved Grail in-house from the start, and financed its improvement alone.

It’s potential that Illumina executives didn’t totally imagine within the challenge on the time, moved to unfold the danger, and have been stunned by better-than-expected outcomes.

This was the primary mistake, a $7.7B mistake, or 1/4 of Illumina’s present valuation. Clearly, Illumina sees one thing in Grail’s outcomes that make it need to purchase out the opposite shareholders at nearly any price.

Such an acquisition can even create its personal set of points. A lot of Illumina’s purchasers are creating competing merchandise, and this might create conflicts of curiosity.

On prime of this, the acquisition was challenged by anti-trust regulators on each side of the Atlantic, largely due to the danger of battle of curiosity with different corporations.

Within the US, questions are coming from the FTC, which additionally blocked Illumina’s 2019 tentative to accumulate its solely actual competitor, PacBio.

Within the EU, the battle escalated additional, with the specter of a tremendous equal to 10% of the corporate’s world turnover.

Nonetheless, Illumina pressed on with the merger, “Regulators be damned” as commented within the trade press.

The anticipated 2024 FDA approval of Grail’s principal take a look at and a goal of fifty million individuals examined (and a price ticket per take a look at of round $900-$1,000) might be behind the frenzy. Even when unfold over a few years, this is able to be 10x Illumina’s present turnover.

In the long run, this mess with Grail mustn’t have a lot influence on Illumina. It has nonetheless made for wasted cash and adverse headlines and it has hammered the inventory worth.

Possibility 1 is that the merger really occurs. This may make Illumina each an gear and a really profitable diagnostic firm. It might be an costly acquisition that would have been prevented, however will doubtless be a worthwhile one. Perhaps a later IPO in 5 years or extra might alleviate battle of curiosity threat and nonetheless earn Illumina a big monetary acquire.

Possibility 2 is for the merger to be pressured to unwind by EU and US regulators. Then Illumina will nonetheless personal 14.5% of Grail, Grail will nonetheless run its take a look at utilizing Illumina machines, and Grail’s rivals will doubtless rely as effectively on Illumina’s best-in-class sequencers.

So general, I count on this to be a brief storm. It doesn’t mirror very effectively on administration’s strategic selections, and this is perhaps the worst facet of the corporate.

However it’s not as catastrophic because the latest inventory worth drop makes it seem. Authorized prices are already coated now, so it mustn’t have an effect on future profitability.

Valuation

When drawing the final 10 years of Illumina’s efficiency on a graph, I come upon the problem of the final quarter’s loss (from acquisition prices and authorized charges) which makes previous progress probably not readable. So I as a substitute will present the income, web revenue, and money circulate till Q1 2022.

I believe the expansion profile of the corporate remains to be intact. Revenues are nonetheless in the identical development The one factor impacting free money circulate within the curve under is a 50% enhance in R&D spending, one thing that ought to repay in an excellent stronger long-term moat.

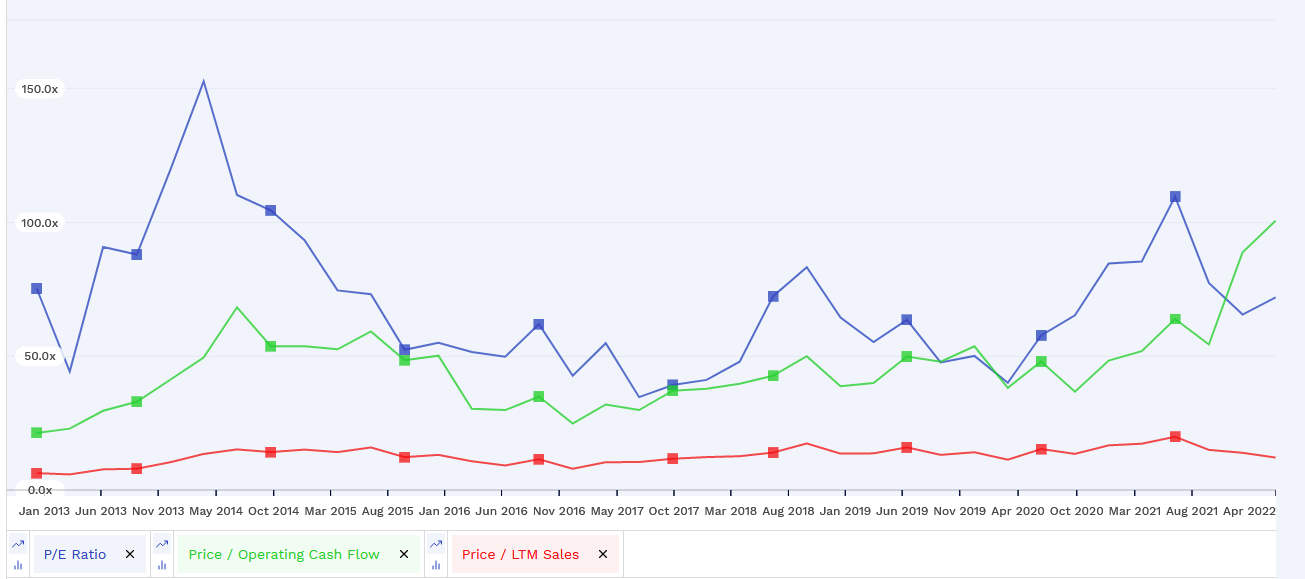

Relating to valuation ratios, Illumina has been (justifiably in my view) valued at a excessive P/E between 40 and 130. Equally excessive, price-to-sales oscillated from 6 to twenty, and price-to-operating-cash-flow from 21 to 89.

The present price-to-sales ratio is 6.6. Earnings are adverse so there’s no P/E. Similar totally free money circulate.

The present adverse earnings and free money circulate are a direct results of the Grail acquisition prices and potential related fines. At most, Grail will lower whole free money circulate whereas it will get prepared for commercialization.

So that is largely a one-time or short-term occasion that won’t change the core moat and high quality of Illumina.

With the price-to-sales ratio decrease than in a decade, I believe the inventory is kind of moderately valued and probably undervalued.

Returns to Shareholders

Illumina prefers share repurchases to dividends as a option to return capital to shareholders.

One available, contemplating the expansion profile, this is perhaps a good suggestion. Alternatively, contemplating the comparatively excessive valuation of the corporate, I’m not solely satisfied that is the perfect option to do it.

Illumina repurchased $750M value of shares between February 2020 and now. With how costly the share costs have been on the time, I query the timing and capital allocation ability of Illumina’s administration.