{kind=link}

Two Books. One Purpose. A Better Life.

🎁 Now Available At Special Prices!

“This is a masterpiece.”

—Morgan Housel, Author, Psychology of Money

“Discover the extraordinary within.”

—Manish Chokhani, Director, Enam Holdings

I am writing this series of letters on the art of investing, addressed to a young investor, with the aim to provide timeless wisdom and practical advice that helped me when I was starting out. My goal is to help young investors navigate the complexities of the financial world, avoid misinformation, and harness the power of compounding by starting early with the right principles and actions. This series is part of a joint investor education initiative between Safal Niveshak and DSP Mutual Fund.

Dear Young Investor,

I hope this letter finds you well.

Let me quickly take you back to when I began my journey in investing almost 22 years back. I thought the most important questions were the obvious ones, like: Which stock should I buy? How much return can I expect? What mutual fund is better than the other? How much should I invest in bonds and how much in stocks?

I spent a lot of time talking to my seniors at work and other elders, searching for answers to these and many such questions, convincing myself that their responses would somehow tell me the future. And they did. But it took me years, and a few bruises, to realise that the most important question I should have asked was not about the market at all. It was about myself.

And that question came from a serendipitous meeting with a very experienced financial advisor who told me this in one of our discussions: “Vishal before you get worried about how much to invest in stocks and how much in bonds, first ask yourself if you are a stock or a bond.”

This sounded odd to me, almost like he was asking me to turn into a financial instrument. And probably you may be thinking the same. But stay with me.

I want you to sit quietly for a few moments and ask yourself this question: “Am I a stock or a bond?”

The answer, believe me, will determine far more about your long-term success than the cleverness of your personal finance models or the sharpness of your stock picks.

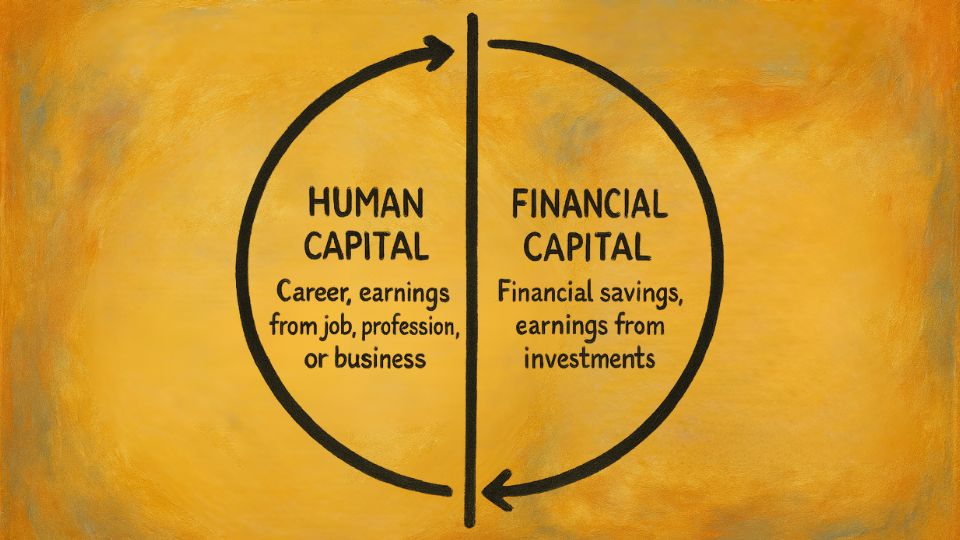

You see, most of us think of wealth only in terms of the money we’ve already saved, and which includes our bank accounts, mutual funds, and our stocks. But that’s just one part of the story. The other part, especially when you are young, is your human capital. That is the present value of all the money you are likely to earn in your career.

When you’re twenty-five, it may feel like you have very little. But think about it. You have thirty, maybe forty years of income ahead of you. If you could add all those future incomes up, discounted to today, the number would be staggering.

In fact, in your early years, your human capital is often ten times or more your financial capital. Let me explain.

Suppose you are 25 years old and just starting your career.

- Your annual salary: ₹10 lakhs

- Your expected career span: 35 years (till age 60)

- Let’s assume your salary grows modestly at 5% per year

- And to be conservative, let’s discount future earnings back at 5% per year (which cancels out the growth assumption and keeps things simple).

In that case, your human capital today = salary × working years left = ₹10 lakhs × 35 = ₹3.5 crores (in present value).

Now compare this to your financial capital at age 25. Maybe you’ve saved a bit from your first job, say ₹3–5 lakhs in the bank or mutual funds.

So, your human capital (₹3.5 crores) is nearly 70–100 times your financial capital (₹3–5 lakhs). Even if you’ve been diligent and saved ₹10 lakhs by 25, your human capital is still 35 times larger.

Now let’s fast-forward to age 45.

- By now, your salary is much higher — say ₹30 lakhs a year.

- You have about 15 years left to work.

- Human capital = 30 × 15 = ₹4.5 crores.

- But by 45, if you’ve been saving diligently, your financial capital may also be ₹2–3 crores.

So the ratio has narrowed. Your human capital is now only 1.5 to 2 times your financial capital.

By retirement, say at age 60, your human capital is effectively zero (no more active income). Your financial capital, hopefully, is the biggest it’s ever been.

This simple arithmetic shows why, in the early years, your future earning potential dwarfs whatever little you’ve managed to save. Your true wealth is not just your bank balance, but also your human capital plus your financial capital. And how you balance one against the other. That’s what sound asset allocation is all about.

And this is where the metaphor of stock or bond comes in. Think about it. A stock is unpredictable. It represents a business, which means it has good years and bad years. Earnings rise, earnings fall, and stock prices reflect this wild ride.

A bond, on the other hand, is steady. It pays interest regularly, and at maturity, it returns your principal. If a stock is a roller coaster, a bond is a train which may be slower, but predictable.

Now ask yourself: what does your career (human capital) look like? What does your income stream feel like?

If you are in a job that is steady and predictable, say a doctor, teacher, banker, or government employee, you are more bond-like. Your incomes arrives like coupons, month after month, with little drama. But if you are in a job that swings with the market, say an investment banker, trader, startup founder, or small business owner, you are stock-like. You may earn very well when things are good, but your income is exposed to cycles. Sometimes it may even feel like being a junk bond, which is high yield in good years, but high risk of default when the tide turns.

Don’t see this distinction as just a metaphor. It has real consequences for how you should invest. If you are bond-like in your work, your portfolio can afford to tilt toward stocks (equities). You already have safety built into your career, so you can take more risk with your savings. If you are stock-like in your work, your portfolio should lean toward bonds (non-equities). Your career is already volatile, so your investments must provide ballast, stability, and peace of mind.

Let me tell you a story here. I had an analyst colleague who had quit our company to join an investment bank in 2007. He was making more money in a year than many people made in a decade. His bonus was bigger than his parents’ lifetime savings. He told me proudly that he was investing every rupee into the market. Not just that, he was also doing derivatives.

“I’m in the market every day,” he said. “I know what’s happening. Why waste time with bonds etc.?”

Then came the global financial crisis of 2008. And that didn’t just wipe out his portfolio, but also his job. He had assumed he was a bond—safe, secure, on a rising path. In truth, his human capital was stock-like, even junk bond–like.

When the market collapsed, both his salary and his savings disappeared together. That’s the danger of ignoring the stock-or-bond question. You double down on risk without realizing it.

Now compare him with a doctor I knew at the time. His income was steady, unaffected by market moods. Even in 2008, his clinic was full. He understood that his human capital was bond-like, so he had the courage to allocate his financial capital more toward equities.

While the investment banker was ruined, the doctor invested steadily through the downturn. A decade later, their fortunes had reversed.

This is why I want you to pause and reflect. Don’t just ask what the Sensex or the Nifty will do, or which fund is the hottest performer. Ask what you are: a stock or bond?

Here, your age also matters. When you are young, your human capital is high. You have decades of earnings ahead, which makes you bond-like even if you are in a volatile industry. That means your financial capital can afford to be in equities. You have time to ride out storms. However, as you grow older, your human capital shrinks. The bond is maturing. At that point, you must tilt your portfolio toward safety, because you have fewer incomes left to rely on.

This is not a rigid formula, but a principle. And one that keeps you from making big mistakes. Too many investors treat their careers and their portfolios as separate boxes. They obsess over market risk, inflation risk, political risk, and so on, but forget about personal risk. And personal risk is the one that can break you. Because if your job and your portfolio collapse at the same time, recovering is much harder than you think.

So, since you are just starting out, here’s what I want you to do. Take a blank sheet of paper and write down the nature of your work. Is it stable and predictable? Or volatile and uncertain? Then write down your age, and how many years of work you likely have ahead.

Put it together, and ask: am I a stock, or am I a bond? If you are a bond in life, tilt your portfolio toward equities. If you are a stock in life, let your portfolio act as a bond.

And if you are the latter, this doesn’t mean avoiding equities altogether. Even if your human capital is stock-like, you can still own equities, but choose them wisely. Look for the “bond-like” equities, which may include strong, stable businesses with predictable cash flows, or broad-based mutual funds that spread risk widely. They won’t give you the thrill of a quick double, but they will give you the steadiness your life may otherwise lack. But please… please, don’t do derivatives and don’t trade stocks!

At times, it also helps to talk this through with someone you trust. They may be a mentor, a friend, or even a financial advisor who can step back from your day-to-day excitement and see the bigger picture. We are all too close to our own lives, and an outside voice can sometimes remind us of risks we’d rather ignore. And not just to help pick investments for us, but also to help us stay true to who we are.

Investing, as I have mentioned in my past letters to you, is not only about maximising returns. It is about building a life where your financial capital and your human capital complement each other, not clash with each other.

I’ve learned the lesson the hard way, through mistakes and observation. You don’t have to. You can begin here, with this one question.

So, dear young investor, before you get lost in the noise of markets, pause. Don’t begin with pie charts or ratios or what your friends are buying. Begin with yourself. Ask honestly: am I a stock, or am I a bond? The answer won’t just shape your portfolio, but your entire financial life.

Sincerely,

—Vishal

Two Books. One Purpose. A Better Life.

🎁 Now Available At Special Prices!

“This is a masterpiece.”

—Morgan Housel, Author, Psychology of Money

“Discover the extraordinary within.”

—Manish Chokhani, Director, Enam Holdings

Disclaimer: This article is published as part of a joint investor education initiative between Safal Niveshak and DSP Mutual Fund. All Mutual fund investors have to go through a one-time KYC (Know Your Customer) process. Investors should deal only with Registered Mutual Funds (‘RMF’). For more info on KYC, RMF & procedure to lodge/ redress any complaints, visit dspim.com/IEID. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Also Read: