Disclaimer: This is not investment Advice. Never trust an anonymous dude on the internet. DO YOUR OWN RESEARCH!!!

As always, I have attached a pdf with the full writeup and only focus on a few sections in this post. And the Sound Track of course.

- Elevator pitch:

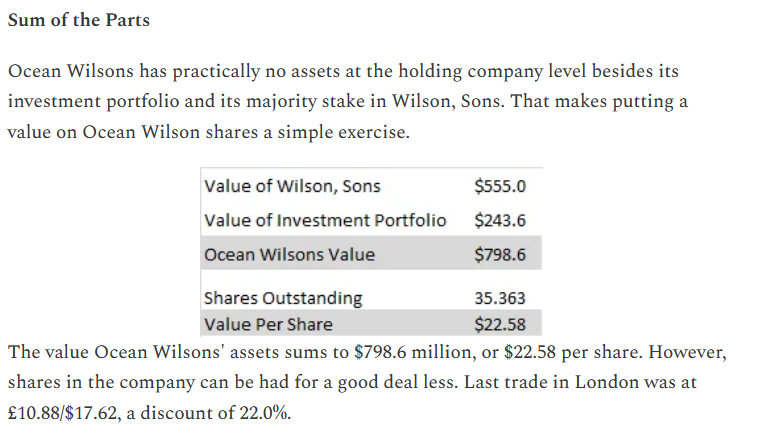

Ocean-Wilsons, a UK listed, Bermuda domicile HoldCo which owns a 56% stake in a listed Brazilian Port/Maritime company called Wilson Sons and an investment portfolio, is trading a a deep discount (-48%) to its SOTP value. Now however it seems very likely that the Brazilian Asset will be sold by year end 2024, which could potentially trigger a re-rating of the stock on top of any premium paid in the sale.

2. Introduction:

Longer term readers of my blog know that in addition to investing into boring GARP stocks, I also invest into Special Situations from time to time. A special situation is a more short term oriented investment with a clear trigger or catalyst. In earlier times, I did more of them, these days I have less time and only look into them if they jump at me but usually with a relatively small allocation. There are different types of Special Situations. This one is of the “Undervalued company sells major operating asset” type of Situation, of which I have done a few in the past. The last one was Exmar two years ago with a decent outcome.

3. Ocean Wilson: Potential sale of major operating asset

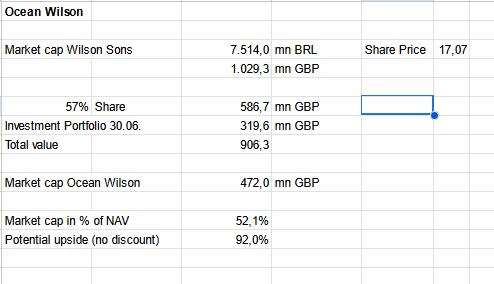

Ocean Wilsons is a UK listed. Bermuda domiciled holding company with a market cap of around 470 mn GBP. It is quite an unusual company. It reports in USD, owns a 57% stake in a listed Brazilian Port/Maritime company and runs a “fund of fund” hedge fund portfolio.

I came across the company during the analysis of both. Logistec and Eurokai, but did not invest up to now.

The Balance Sheet is hard to read as it combines an investment portfolio and the consolidated Brazilian Port operations.

On the plus side, as the subsidiary is listed, it is quite easy to see that the value of that participation called (Wilsons Sons S.A.) is higher than the market cap of the parent company.

A quick and dirty SOTP analysis gives us the following Discount/potential upside:

Prior to the announcement (early June 2023), Ocean Wilsons also traded at a 50% discount, so the discount to NAV hasn’t narrowed that much.

Funnily enough, when Alluvial Capital wrote about Ocean Wilson in 2013, the discount back then was only 20% (those were the days….):

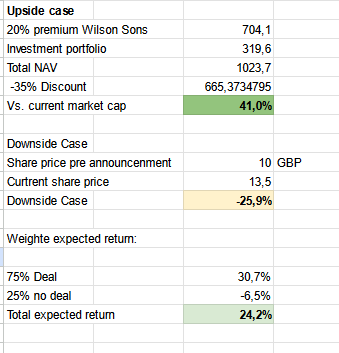

8. Calculation of the potential return:

In order to calculate a potential return on this special situation, we need to make a few assumptions:

- What is the assumed probability of a deal vs. no-deal ?

- What is the timeline ?

- What will be the ultimate purchase price for the Brazilian stake ?

- What will Ocean Wilson do with the proceeds ?

- How will the share price of Ocean Wilson react, i.e. how will be the discount to NAV after a deal ?

- What happens if the deal does not go through ?

My “gut feeling” assumptions would be as follows:

- 75% probability

- Year end 2024 (for deal announcement, Q1 2025 for NAV discount tightening)

- Current market price +20%

- Reinvest in Hedge-Funds

- NAV discount will narrow to -35%

- Share price will drop back to mid June Level 2023

This gives us the following “expected” return:

Of course my assumptions could turn out to be wrong

- The purchase price could be lower or higher.

- Maybe the NAV discount doesn’t narrow at all (negative).

- Maybe Ocean Wilson pays a special dividend or even buys back stock (positive).

- If the deal fails, the share price could go lower (negative).

- the timeline could be further extended

On balance, I do think that my assumptions are not aggressive and should be considered a “Base case”. For me, +24% expected return for a potential holding period of ~6 months looks pretty OK.

11. Conclusion & Game Plan:

Ocean Wilsons Holdings looks like a potentially interesting special situation. There is a relatively clear catalyst with decent upside and the potential downside looks limited.

I therefore decided to allocate ~2% of the portfolio into this Special Situation investment at ~13,70 GBP/share.

The interesting part will be if and when we get further information on a sale. Equally interesting will be if Management then says something about what they are going to do with the proceeds. In the Exmar case for instance, there was a time lag between the announcement of the sale and the announcement of a rather small special dividend.

It might also be helpful to watch what Hansa Investment and Wilson Sons will communicate in parallel.

Bonus Soundtrack: Mas que nada

Sergio Mendes feat. Black Eyed Peas – Mas Que Nada