Management summary:

In this post I wanted to dig a little deeper on why I think that many currently offered Retail Private Equity offerings (e.g. ELTIFS) will most likely underperform public equity markets going forward. Despite some structural advantages of Private Equity as such, the double layer of fees and costs will be a huge drag on performance. On top of that, historic tailwinds for the PE industry (low interest rates and low purchase multiples) have most likely disappeared.

Introduction:

After the first installment of this mini series, where I tried to explain why stated PE IRRs should not be confused with actual performance, I wanted to briefly touch another important point in order to understand this “asset class” better:

Many Private Equity players claim that both, past returns and future returns of Private equity will be significantly better than comparable indices of listed equity.

Usually, people who are selling these structures mention like 10-15% return p.a. (or even more) which should be better than the typical 7-10% normally assumed for public equity which of course makes Private Equity a quasi “no.brainer” and an Asset Class that must be “urgently democratized”.

Potential Sources of Alpha for Private Equity:

So let’s look into these claims in more detail.

The Private Equity industry itself often offers the following reasons why their offering is “superior”:

- Private Equity has a longer time horizon

- Private Equity can actively influence the businesses (including the financing structure)

- Private Equity has access to more companies (listed & unlisted) and could be in theory more diversified

- The incentive structure is better than compared to normal funds (Manager only makes money after investment is returned to investors)

- PE firms have a better ability to time markets (buy cheap, sell expensive)

- Private Equity portfolios are less volatile

However I would add also a few aspects that would counter the rosy return projections:

- Private Equity “Alpha” is concentrated only a few managers that might not be accessible for everyone

- Fees, fees and costs

- Higher valuations & the role of cheap leverage

So let’s look at these features and examine if they are real “alpha factors” or just marketing gimmicks..

- Longer Time horizon

Indeed, the average holding period for actively managed mutual funds in the US is supposed to be between 1-2 years for the US, for Hedge Funds most likely even less than that. A typical holding period for a PE investment however is typically 5-7 years.

A typical PE investor normally just cannot simply trade in and out of positions.Good Private Equity investors however normally have a clear plan what they want to do with a company and have at least 3-4 options on how to exit an investment.

So yes, PE funds do have a longer time horizon. This clearly doesn’t guarantee higher returns per se, but it clearly gives the manager time to maximise the outcome and the ability to invest in and profit from mid-term transformations.

- Active influence

This is the second most relevant argument, that PE investors can actively steer companies. However, this only applies fully to so-called “full control” investors and not every PE manager is a full control investor.

Usually, you only get full control, if you own (significantly) more than 50% of a company. Of course one can also have a certain influence with a 20% or 30% position, but full control is obviously better.

The value of the control clearly depends on the experience and the ability of a Private Equity investor. As history has shown, even full control deals can go south if done at the wrong time or, what happens quite often, with too much leverage.

On the other hand, even in the listed space, there seems to be pretty clear evidence, that as a whole,stocks with a clear long term oriented owner do better over time than those without.

So We could also give this point to Private Equity, although one could maybe replicate this in the public market with a strategy that focuses on stocks with “owners”.

- More diversification due to access to both, private and public companies

The argument that is often made is that only 10% or so of companies are listed and so Private Equity allows access to a much larger universe. On this argument, I would actually call BS.

Yes, in theory, PE could access more companies, but due to Fund sizes etc, the actual selection is not that big. Not every private company is for sale at any time etc.

In order to get real diversification, an investor has to invest into a lot of funds over a lot of intages which is only feasible for the largest institutional players.

One could actually make the counter argument that Private Equity is effectively a Small- & Mid Cap Strategy, so an investor lacks access to Large cap, which, as we all know have driven stock performance in the past years via Microsoft

In practice, in my opinion, any investor gets much better and instant diversification via listed stock index funds.

- Incentives are better for Private Equity than in public markets

As a rule of thumb, PE managers (and their employees) only earn money when the investor’s money is returned and investors have received a minimum return AFTER fees which is usually 8%.

Compared to a normal stock manager, even with a performance fee, this is clearly better, as for instance performance fees for normal stock funds are often paid out on a yearly basis and so often incentivises short term risk taking with no “claw back” if things go wrong later.

One important detail to mention here is that however the PEs not only get a share of what they earn above the hurdle rate but also, if the fund is successful, from 0% investor performance.

How this is exactly calculated is often hidden in the Fund documents but the section to search for is called “GP catch up”. This can be a number between 0 and 100%.

100% GP catch up means that after crossing the hurdle, any Dollar earned by the funds goes to the GP until they have earned their performance fee (usually 20%). So if a fund with a “GP catch up” of 100% earns 10% p.a., the hurdle is 8% and the carry 20%, the investor gets 8% and the GP 2% of these 10%.

To be honest, the incentivisation of a fund with a 100% GP catch-up is not that much better than a public stock fund.

Another important detail here is, if a fund employs an “European waterfall” or an “American Waterfall”. This has nothing to do with water but with the mechanism how carry (Performance fee) is allocated. The European Waterfall required that the whole fund earns the hurdle rate, whereas the American waterfall calculates Carry on a deal by deal basis which in my opinion is a really bad way to incentivise fund managers.

So as a summary for this section: If a PE fund is properly structured ( GP catch up significantly below 100%, European waterfall), the incentive structure is indeed better than most traditional mutual funds. However, this is not always the case and especially in offerings to retail clients I have seen really bad incentives structures.

And as Charlie Munger said: Show me the incentives, then I show you the outcome.

- Market timing abilities

In the financial literature there is some evidence that PE managers at least seem to be able to time their exits well. The question is if this is an active skill or a result of the inevitable IPO boom after a longer positive run in the stock market.

Recently however, especially in the German/European market, PE IPOs had been timed maybe too well, leaving investors with significant losses.

So timing at least partially seems to favor Private Equity to a certain extent.

6. Private Equity is less volatile

Looking at reported Private Equity returns, which are normally only published on a quarterly basis could lead to the conclusion that the volatility is indeed lower than for listed stocks. There are some quite sophisticated arguments why this is the case but in reality it is quite easy:

Private equity has a build in “time machine” in reporting performance which allows them to easily “smooth out” returns.

How does that work ? As a fund investor, You will get your quarterly valuation normally only around 90 days after the end of the quarter, so more or less effectively at the end of next quarter. In addition, unless a position is already IPOed and listed, The PE forms have a pretty wide discretion how to value their investments. Reporting is never really transparent. You might get some kind of “adjusted EBITDA” numbers or even an EV here and there, but overall, investors often don’t fully understand how their stakes are valued.

So what PE firms now do is quite obvious: they wait as long as possible to see how the situation in public markets develop and then decide relatively late how they will mark their positions. If for instance there was a huge drop in the indices and then a decent recovery (like for instance in the current quarter), a GP will do …..exactly nothing. The valuation wil lmost likely not change much and don’t show much volatility.

If markets dropped significantly over a longer period of time, GPs will then slowly mark down their positions. If markets go up significantly, GPs will mark up slower to keep a reserve for bad quarters. The main challenge for GPs is to mange valuations in a way that they don’t have to show a loss at exot.

The variations are endlessly but as an investor you must remember two things: The quarterly return you see in your fund is actually the return from a quarter before and has little to do with the actual development in that quarter. It is mostly a made up number.

Cliff Asness form AQR has coined a very good term for this: “Volatility laundering”.

So in essence, PE returns are clearly not less volatile than public stocks, they just appear to be less volatile.

Counter arguments to Private Equity “Alpha”

1. Private Equity “Alpha” is concentrated only a few managers that might not be accessible for everyone

One big issue with Private Equity is that different than in public markets, you can access the asset class only via a manager. There is no index fund.

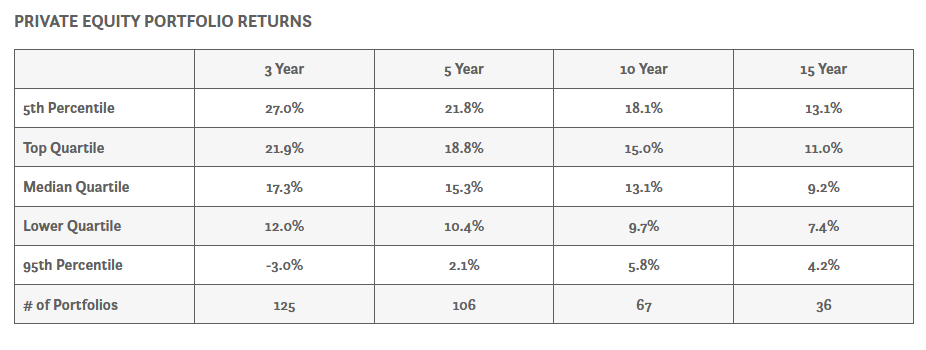

Now not all Private Equity managers perform equally. And the difference between well performing fund managers and not so good managers is persistent and very significant.

I found for instance this table which shows the differences between good and not so good managers:

The difference between the best 25% of managers and the bottom 25% is between 9% for 3 years and ~4% over 15 years.

Also the dispersion graph which doesn’t average the returns clearly shows how different returns are:

So why not just invest into the best managers ? Well, in order to create really good returns, the top performing have to limit the size of their fund because success in Private Equity is not extremely scalable. And often it is not a secret, especially among the more experienced managers, who the really good funds are.

So the big question is: Who will get the chance to invest ? Most often, investors that have been investing in previous funds have priority. Next come large, deep pocketed investors who can write large checks.

In my opinion, it is an absolute phantasy to think that a structure that is targeted to Private investors will get access to “proven winners” among PE funds. Maybe, some of the funds they will invest will turn out to be good, but as a consequence, without the access to the great managers, your expected return will be in the best case slightly below the average for PE, in the worst case significantly below the average if you end up with underperforming managers.

Many products that target Private Investors are also very intransparent in what funds they will actually invest. Just naming a few “household PE names” tells you nothing.

These effect is even more pronounced in Venture Capital, which is a small subsegment of Private Equity. A rule of thumb is that the top 5% of Venture funds consistently earn all the Alpha in Venture capital. And it is close to impossible to get into these funds if you are not already an investor.

My verdict here is that Private Investors will most likely not end up in the top quartile of managers and as a consequence experience significant lower returns than the “average” over time. Private Investors in Venture Capital will need to be lucky to get positive returns at all.

One final remark here: Don’t mistake “Household PE names” with Top Performers. Usually, especially the “Mega Funds” of the large players are not top performers.

2. Fees, fees and Cost

As mentioned above in the chapter on incentives, fee calculations are complicated and can vary a lot between funds.

For a typical 2&20 PE fund with a hurdle rate of 8% and 100% GP catch up, a “gross return” before fees of 12% p.a. turns into an 8% net return for investors. As a Private investor you will be subject to another layer of fees, which are typically something like an extra 1-1,5% base fee and another 10% Performance fee. With this second layer of fees, the gross return needs to reach 14% or more in order for the investor to get 8%.

Now we haven’t even seen the costs that are involved in doing PE investing. The industry is once again very intransparent, but buying and selling whole companies is very costly. You have to pay banks, consultancies etc. I would say a typical cost charge per investment is something like 5% each on the way in and out. On top of that we have costs for deals that do not materialize etc. My personal estimate is that these costs add at least another 1-2% p.a. of drag at fund level.

Again, structures for Private investors will add additional costs on top of that that are usually not very well disclosed.

3. Historic tailwinds might not be repeated – valuation & leverage

This is the graph taken from the excellent Bain Capital PE report:

Over the last 20 years, the initial deal valuation has doubled. That multiple expansion was really good for old deals that have been done cheap, but is clearly a headwind going forward.

With regards to interest rates, one might just listen to the latest episode of the “Dry Powder” Podcast, where a PE veteran clearly explains how much more difficult it is to achieve good returns at current interest rates vs. a ZIRP environment.

Bringing it all together: What returns can a Private investor expect from Private Equity ?

As we have seen in this post, there are some structural features that can lead to better performance for Private Equity managers compared to their listed peers BEFORE COSTS AND BEFORE FEES.

However, in order for this to actually reach the (private) investors, this needs to compensate for multiple layers of costs and fees, especially for typical fund-of fund structures.

My “back of the envelope” calculation of a typical cumulative fee drag from “gross returns” (i.e. before any fees and costs) to net returns investor looks as follows:

- minus 3-4% p.a. of base fee & incentive fee at primary fund level

- Minus 1% p.a. of costs at primary fund level

- Minus 1-2% p.a. of base fee & incentive fee at Retail structure level

- Minus 1-2% p.a. of costs at Retail structure level (ELTIF)

- Minus 2-5% p.a. underperformance because of inability to access top funds

So in sum, this leads to a drag of MINUS 8-15% p.a. from gross returns to actual pre-Tax net returns at Private investor level in a typical “Retail fund of fund” structure.

And on top of this we still have to remember that actual performance and IRRs stated from Private Equity funds are not the same.

Now one could debate how much “Alpha” PE can generate from its structural advantages, but in my opinion it is very unlikely that for a retail investor, this potential Alpha does not compensate for the extra costs at Retail level.

Some institutional investors are currently debating if the Alpha does actually compensate for the cost at primary fund level.

So for any Private Equity investor I would make the following recommendation: Be extra careful with the current flood of retail Private Equity products. The returns might be a lot lower than promised unless costs are low and you have access to the top managers.

So now what would be a real, actual performance for a Private Equity Investment ?

The real performance numbers for Private Equity are extremely hard to get. I wonder why ? One pretty decent source is CALPERS, one of the largest US Pension funds. Calpers has been doing PE for a long time, they have the size to get fee discounts and they have the access to the top funds. This is what they say in their last annual investment report:

“The investment team presented private equity’s 20-year annualized returns of 12.1 percent, making it the top performing asset class of the Fund over that period.”

So theoretically, these 12% would nicely fit into the promised 10-15% that has been promised but remember: CALPERS doesn’t pay any retail fees or costs and the might even get (significant) discounts on primary fund fees. And they have access to the top of the top. Looking at the list that I mentioned before, as a retail guy, you might have 4-9% p.a. lower returns due to additional fees & costs and less access to top managers. And this does not include any “discount” on missing tailwinds such as higher interest rates and low entry multiples.

In the next episode I will look at existing opportunities to invest into Private Equity via public markets. Currently, a lot of these assets are actually trading at significant “discounts”.