Private Equity Mini series (4) : “Investing like a “billionaire” for retail investors in the UK stock market via PE Trusts

This is the 4th part of my Private Equity “mini” series. The previous posts can be found here:

Private Equity Mini Series (1): My IRR is not your Performance

Private Equity Mini series (2) – What kind of “Alpha” can you expect from Private Equity as a Retail Investor compared to public stocks ?

Private Equity Mini Series (3): Listed Private Asset Managers (KKR, Apollo & Co)

Background:

Not sure if this is mainly a German phenomenon, but you can’t listen to a German finance podcast without being quite aggressively advertised on how Private Equity is finally being democratized through some “revolutionary” retail offerings that almost always are quite complicated and contain another layer of fees on top of what the PE guys are charging.

The main pitch is that now even the small guy on the street can do what previously only billionaires could do: Invest into Private Equity and make boat loads of money.

The hard truth is that Private Equity has been democratized long ago in the UK but no one gives a sh** about it.

UK listed Private Equity Trusts

In the UK, there is a tradition that almost any unlisted or listed asset class gets repackaged as an open ended fund or “Trust” which in most cases can be traded as easy as any other stock on the UK stock market.

The Excellent Verdad capital blog recently had a post about these trusts focusing on two aspects:

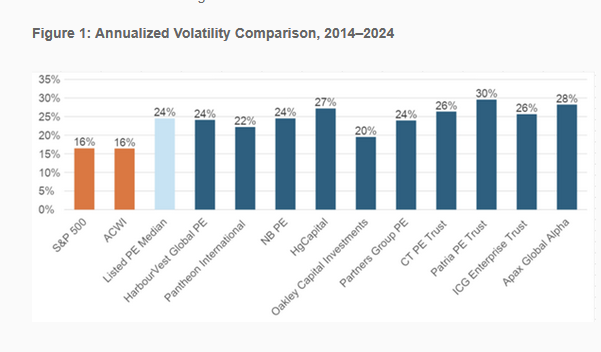

- These traded funds show (of course) a much higher volatility than the underlying “smoothed” NAVs

These clearly shows that in reality, PE assets are not less volatile than public markets, they just look less volatile because of the knows issues (Quarterly valuations, “Volatility laundering” etc.)

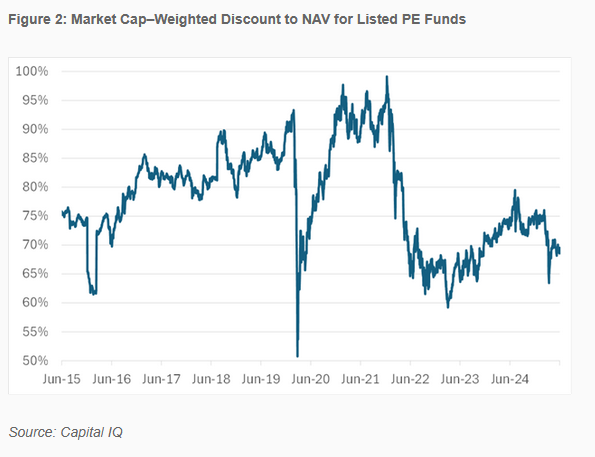

- On average, these funds trade at 70 cents on the dollar. So not only does this asset class offer access to retail investors, but even at “juicy” discounts:

Diving deeper

So let’s dive a little bit deeper into these trusts

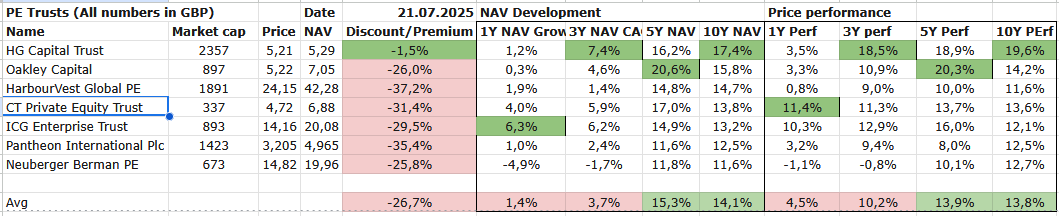

Citywire gives us in principle 13 different listed PE Trusts. I have chosen 7 of them that actually have at least 5 year history and a PE focus.

Here are the NAV discounts and Performance Numbers (NAV & Share price) over 1.3,5 and 10 years.

NAV Discounts

What we can see is that all 7 trusts trade at discounts, on average a whopping -27% to NAV.

What is maybe not surprising is the fact that the best performing fund over 10 years, Hg capital has the lowest discount. What I find interesting is that the rest of the trusts don’t show a clear pattern. Oakley, which has a still decent performance over 10 years, has the same discount as the Neuberger Berman vehicle that performed significantly worse.

Performance

The most interesting aspect of this whole exercise is in my opinion that we can see here “real” performance as these vehicles actually reinvest cash flows compared to the typical IRR numbers of single PE funds.

Looking at the chart again it is very striking, that for the past 1 year and 3 years, NAV performance and Price performance was quite weak on average for the whole group..

My interpretation is as follows: Most PE funds have “smoothed” over negative 2022 performance. However, as Private Equity is mostly small- to midcap focused, they couldn’t participate in the large cap rally of 2023 and 2024.

But still, the 10 year numbers look quite decent. However, these are performance numbers in GBP and the performance has benefitted from a stronger USD as most of the funds have significant USD exposure. In USD, 10 year performance would be around -1,6% p.a. lower.

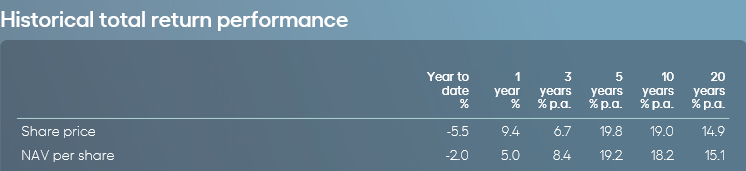

For those funds that have a longer track record, 20 year numbers are lower than 10 year numbers.

Hg for instance looks as follows:

Over 20 Years, the FX tailwind was around 2,5% p.a., adjusted for this, an investor has made around 12,5% p.a. which is good but clearly not out of this world. In my opinion, something around 12-15% real world return is the best you get from a top class Private Equity fund in the long run. On average, after fees, that number is clearly lower, not much different from public markets in my opinion.

Another interesting fact is that the two best performing funds, Hg Capital and Oakley both invest directly into their own deals, whereas all the others are more indirect “fund of fund” vehicles that invest into Funds and/or Co.Investments of other PE GPs.

Fees, Fees, Fees. & Costs

Initially, I wanted to do a comparison of the fees between the vehicles, but it turned out to be too much of a hassle. Some Trusts report the fees quite transparently, for some it is really hard to find the basic information on fees.

ICG is quite transparent and has the lowest cost & Fees with a total charge of 1,38% at vehicle level. However, a significant part of the portfolio is invested into other funds which again charge fees that are not included in the 1,38%.

As mentioned, Oakley and Hg only invest into their own funds and have no additional Management fees on trust level but of course “typical” PE funds fees that can be 4% p.a. in a good year.

The Neuberger Berman vehicle only invests into low fee co-investments form other GPs but this clearly doesn’t help the performance much.

Fun fact: German “Neo PE for the masses” player Liqid is offering a product (Liqid NEXT) that seems to have the exact same strategy like the NB vehicle just packaged as an “ELTIF II vehicle”. However, the Liqid product includes some provisions (deal by deal carry) that will make it even worse for investors.

In my opinion, being so opaque about fees and costs is not a bug but a feature of the whole Private Equity industry. The industry has gotten away with charging extraordinarily high fees for a few decades now and I wonder how long this will remain to be so.

Valuations

Another issue is that not every PE fund is transparent about the valuation of the portfolio companies. Yes, a 30% discount to NAV sounds good, but a discount for something that is extremely overpriced might be a bad deal.

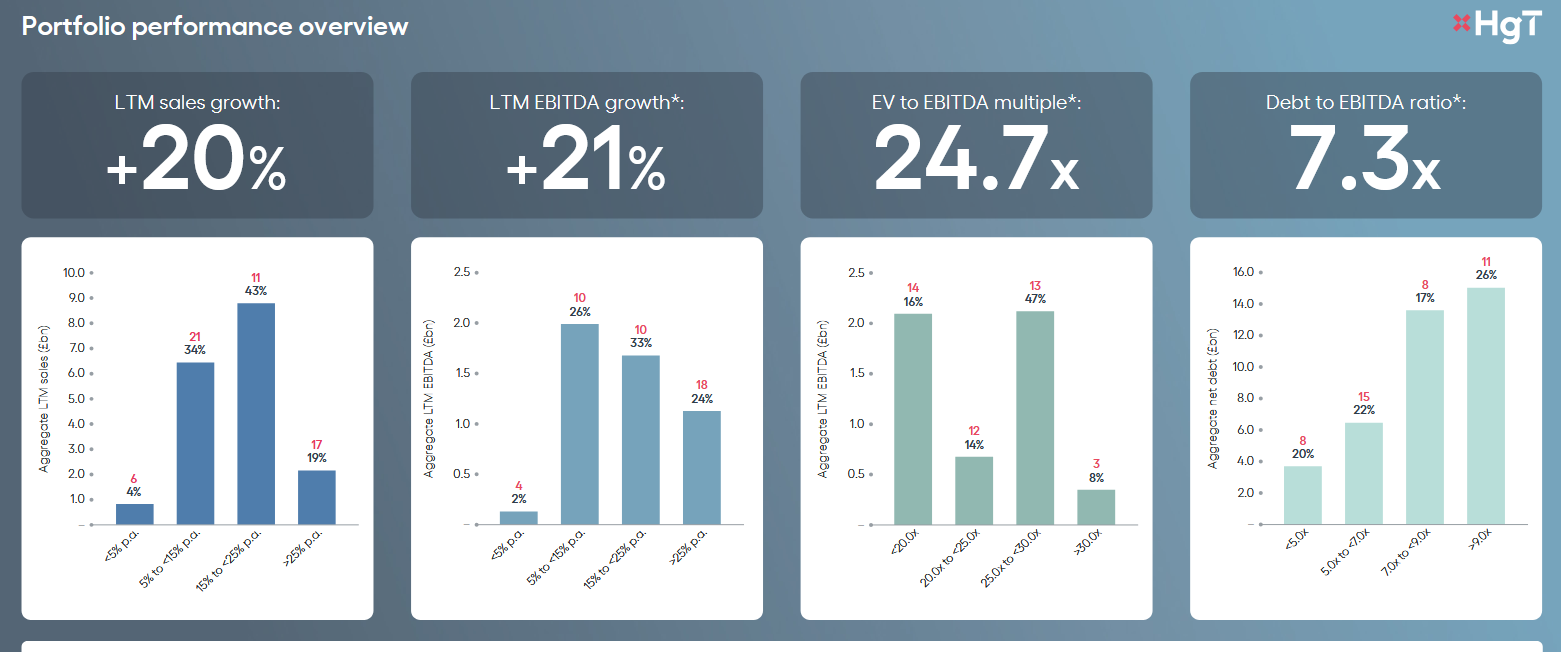

Looking at the Scoreboard leader HG Capital, they have at least a quite informative valuation slide:

An average valuation of ~25x EV/EBITDA is clearly errrm not cheap. However, their companies are growing but debt is also quite high. Hg capital is mostly a Software PE investor.

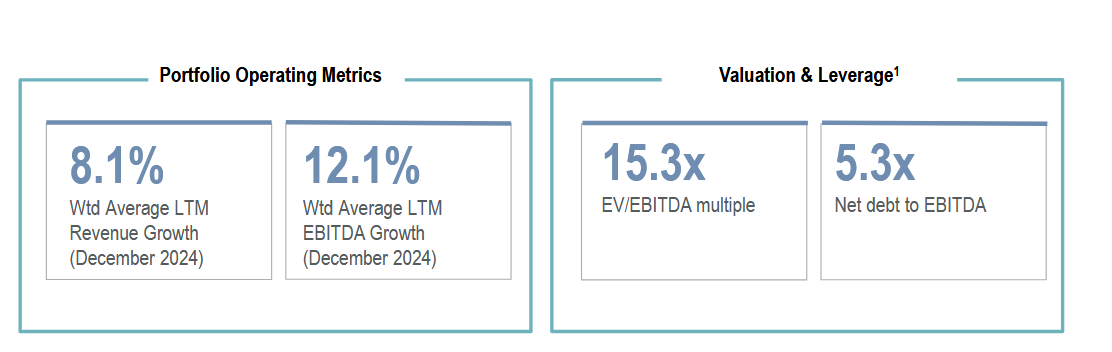

NBPE has a somewhat more general lower growth portfolio, but a valuation of 15x EV/EBITDA is not cheap either:

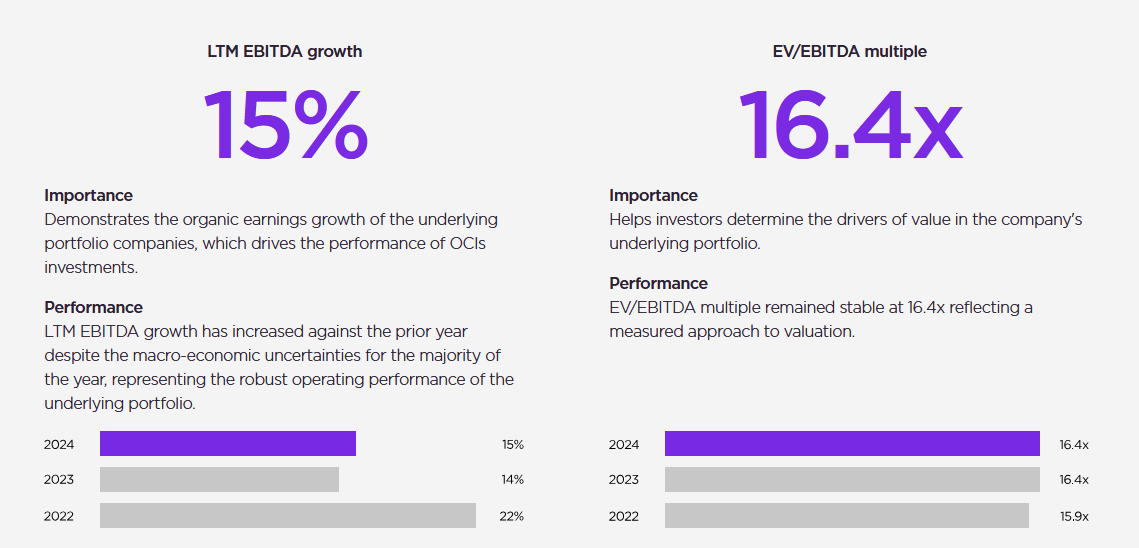

Oakley is somewhere in between with ~15% growth and 16,4x EV/EBITDA

In summary, at least to me, valuations look quite stretched. If I want to pay 15xEV/EBITDA, I have a wide choice of top notch quality company in public markets. Even at a 30% discount, this is still not dirt cheap, especially considering the rather high leverage of many of these companies.

I guews this is also the main problem for the PE GP’s: At those valuations, it is not that easy to IPO any of these companies, unless you are a Defense/AI company/AI Chip company.

Summary – what now ?

I am not here to give investment advice, but if you desperately need PE exposure, this list might be the best place to look at as a retail investor.

If I were forced to buy 2 of those trusts, I would most likely go for Oakley (good track record, decent discount) or ICG (low fees). A third would be Hg as this is really a top notch PE, but you need to be comfortable with Growth company valuations.

For me personally as a value investor, despite the discounts, the overall valuation looks somewhat streched. At the current valuation of these funds, I would construct a great quality portfolio that, without the PE fees, will most likely outperform the PE guys in the long run.

Compared to the fancy new “ELTIF II” vehicles, these trusts are clearly simpler, more transparent and liquid on a daily basis. The only advantage of ELTIF structures is that you don’t see the volatility.