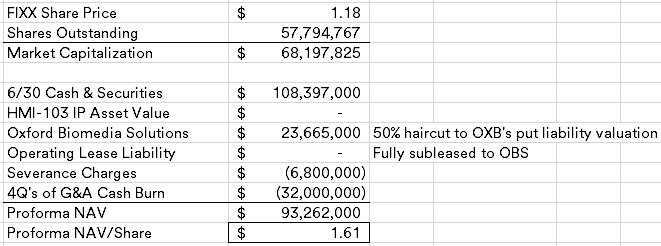

Homology Medicines (FIXX) (~$70MM market cap) is a medical stage genetics biotech whose lead program (HMI-103) is supposed to deal with phenylketonuria (“PKU”), a uncommon illness that inflicts roughly 50,000 individuals worldwide. In July, regardless of some early optimistic information, the corporate decided to pursue strategic options as FIXX would not be capable of elevate sufficient capital within the present surroundings essential to proceed with medical trials. Alongside the strategic options announcement, the corporate paused improvement and decreased its workforce by 87% which resulted in $6.8MM in one-time severance costs.

Exterior of roughly $108MM in money (netting out present liabilities), FIXX has a probably priceless 20% possession stake in Oxford Biomedia Options (an adeno-associated virus vector manufacturing firm), a three way partnership that was shaped in March 2022 with Oxford Biomedia Plc (OXB in London). As a part of the three way partnership, FIXX can put their stake within the JV to OXB anytime following the three-year anniversary (~March 2025):

Pursuant to the Amended and Restated Restricted Legal responsibility Firm Settlement of OXB Options (the “OXB Options Working Settlement”) which was executed in reference to the Closing, at any time following the three-year anniversary of the Closing, (i) OXB could have an choice to trigger Homology to promote and switch to OXB, and (ii) Homology could have an choice to trigger OXB to buy from Homology, in every case all of Homology’s fairness possession curiosity in OXB Options at a value equal to five.5 instances the income for the instantly previous 12-month interval (collectively, the “Choices”), topic to a most quantity of $74.1 million.

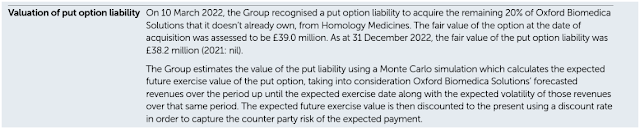

Poking round OXB’s annual report, they’ve the under disclosure:

Utilizing the present change fee, that is roughly $47MM in worth to FIXX. Now OXB is not a big cap phrama with a limiteless steadiness sheet, so there’s some counterparty threat that OXB will in the end be capable of make good on this put. In my again of the envelope NAV, I’ll mark this at a 50% low cost to be conservative.

Not like GRPH, the working lease legal responsibility at FIXX is generally an accounting entry as the corporate’s workplace house is being subleased to Oxford Biomedia Options, however would not qualify for deconsolidation on FIXX’s steadiness sheet. I’ll take away that legal responsibility, be at liberty to make your individual assumption there. Moreover, despite the fact that HMI-103 could be very early stage, it wasn’t discontinued on account of a medical failure and might need some worth regardless of me marking at zero since I am unable to decide the science.

It’s laborious to handicap the trail ahead, possibly OXB buys them out, they may do a pseudo capital elevate with FIXX’s money steadiness whereas eliminating the JV put possibility legal responsibility. Or FIXX may pursue the same old paths of a reverse-merger, buyout or liquidation.

Disclosure: I personal shares of FIXX