Management summary:

If you are looking for actionable investment insights, you can skip this post. This post is more about satisfying my own curiosity why the two UK traded battery funds have been doing so badly in the recent months. In the unlikely case you are interested in that, I invite you to read on.

The UK was for some time a lighthouse country for rolling out “grid scale” Battery Energy Storage Systems (BESS) in Europe. Relatively benign regulation and support schemes allowed a significant amount of BESS capacity to be developed in the UK, well ahead of other European countries.

UK being the UK, there was also an early offer for investors to participate in this development with 2 closed end funds/trust, One from Gresham House (GRID( and another one from Gore Street (GSF).

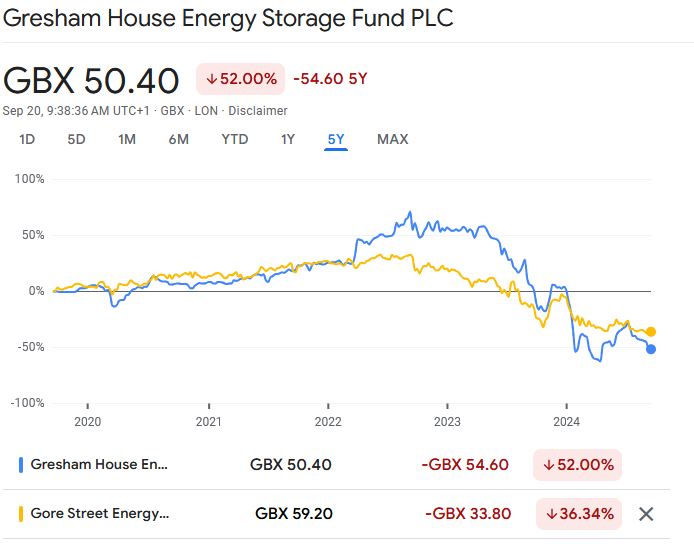

Both funds did very well in the beginning until mid 2023 before declining significantly:

Gresham House Energy Storage fund (GRID)

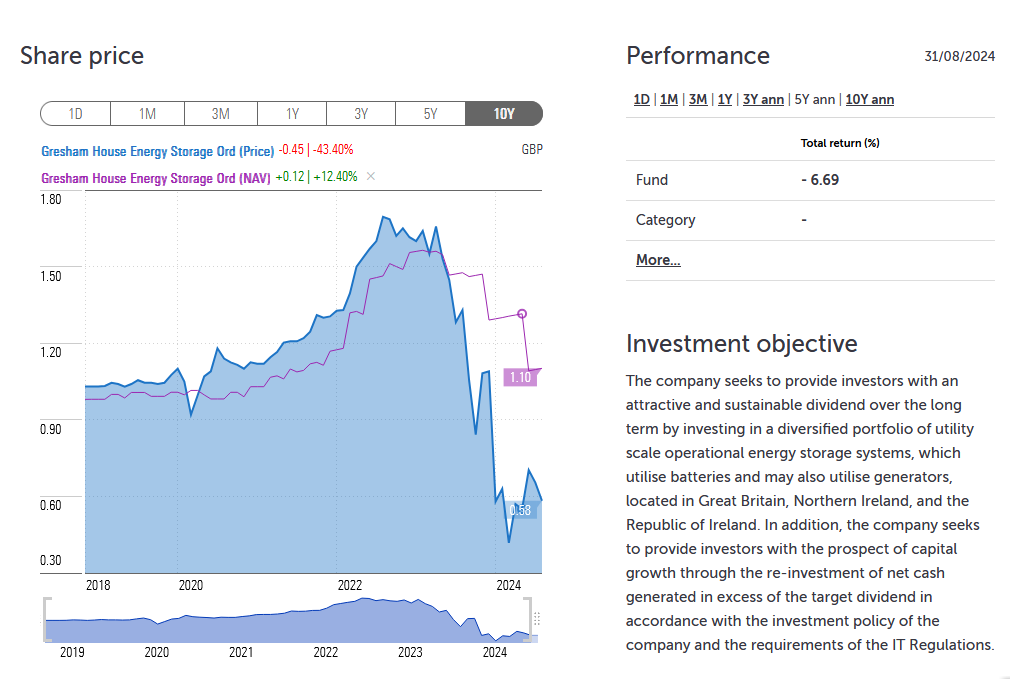

The larger of the two, the Gresham House Energy Storage Fund with the nice Ticker GRID was doing very well initially, with a strongly increasing NAV and unit price. From inception in 2019 until mid 2023, the trust was actually trading at a premium to NAV before things went south as we can see in this chart:

This of course leads to the question: What happened here ?

Battery storage still is supposed to be a very “hot” asset class and an essential part of a well functioning Renewable Energy system. Yes, the pendulum has swung back from the wild optimism following the Russian attack on Ukraine, but that doesn’t explain the bad fundamental performance of the fund with a rapidly declining NAV.

So let’s look at the recent history of the fund:

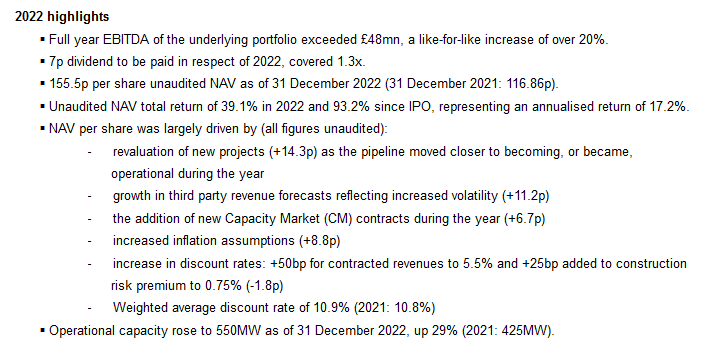

Things looked dandy at the end of 2022. This is from the year end trading update:

Cash was gushing in, NAV was increasing significantly and everyone was happy. Just as a very crude measure we can divide the realized EBITDA (48mn) by the average operational capacity (550+435)/2 and get to a number of ~97k EBITDA for every MW installed which looks like a pretty decent return on investment.

Then a few things happened: First, the fund placed additional units into the market, especially also for retail investors at the juicy NAV of 155 pence.

Then, the Fund manager Gresham House itself was sold to a company called Searchlight Capital Partners in July 2023. The Battery fund was only 10% of the assets, but clearly one of the most “sexy” parts.

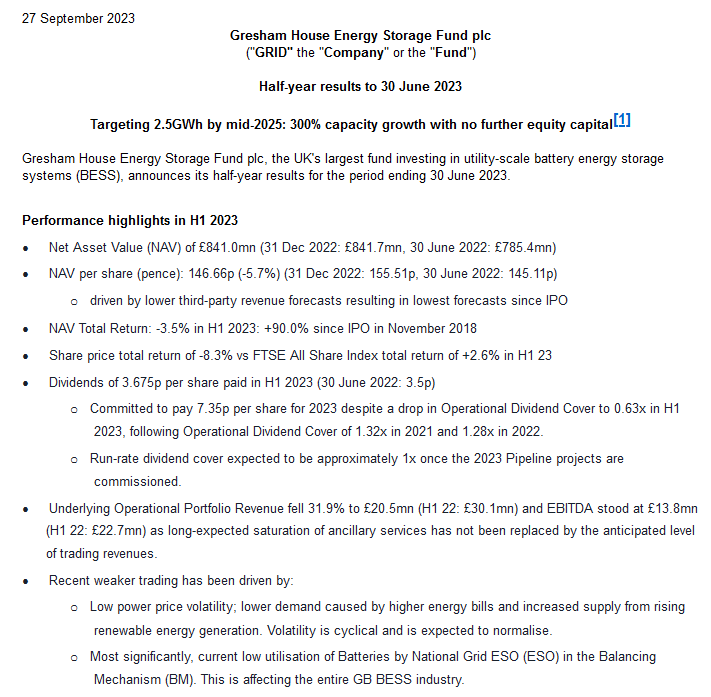

Then, coincidently only 2 months later, in the 6M trading update, the first cracks showed already with a slight reduction in the NAV after a long series of increases:

Annualized EBITDA was ~28 mn GBP, this translates to around 49K EBITDA per MW installed. a pretty drastic decline from just 6 months earlier.

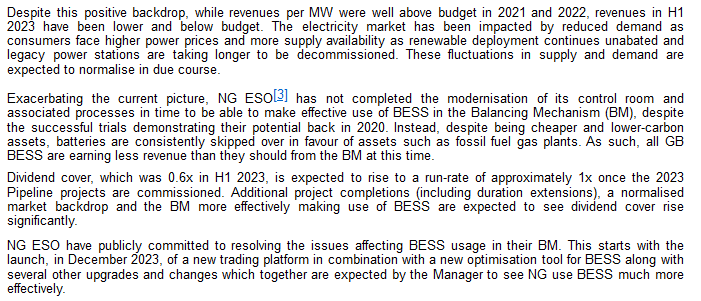

In this update they also mentioned for the first time, that national Grid, the operator of the UK electricity grid was unable (or unwilling) to include BESS capacity in the Grid rebalancing mechanism.

Nevertheless, management was quite optimistic that this was only a temporary problem:

This optimism however was gone when they dropped the Q4 trading update in January 2024:

The Dividend was suspended.

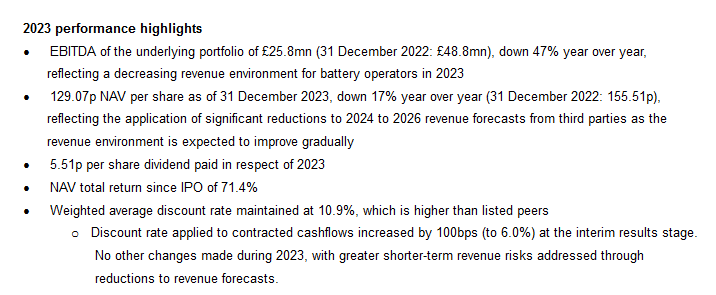

The full year results that were released in April 2024 painted an even worse picture than mid 2023:

This translates into ~42k EBITDA per MW, much lower than in the first 6M anuualized. With a valuation of ~900k per mW it was also clear that further nAV cuts were inevitable.

Fast forward to the latest trading update, 6M 2024:

EBITDA has fallen further, annualized EBITDA of 20,8 mn compare to on average 730 mn installed capacity, giving us ~35K EBITDA per MW installed.

Management is once again optimistic, but given the track record, Investors seem to be very wary.

The Gore Street Fund

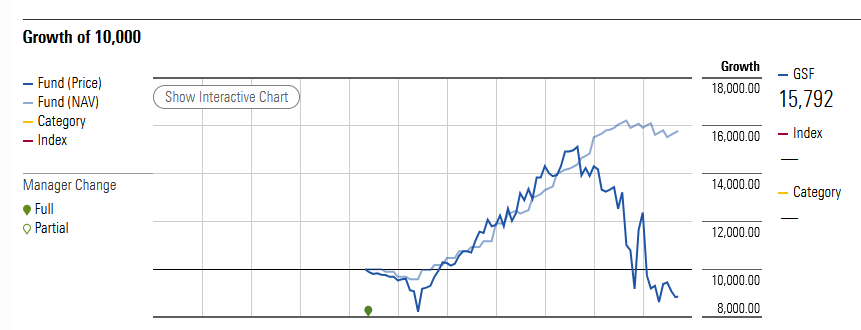

Looking at the chart, the Gore Street fund has been doing slightly better but not that much:

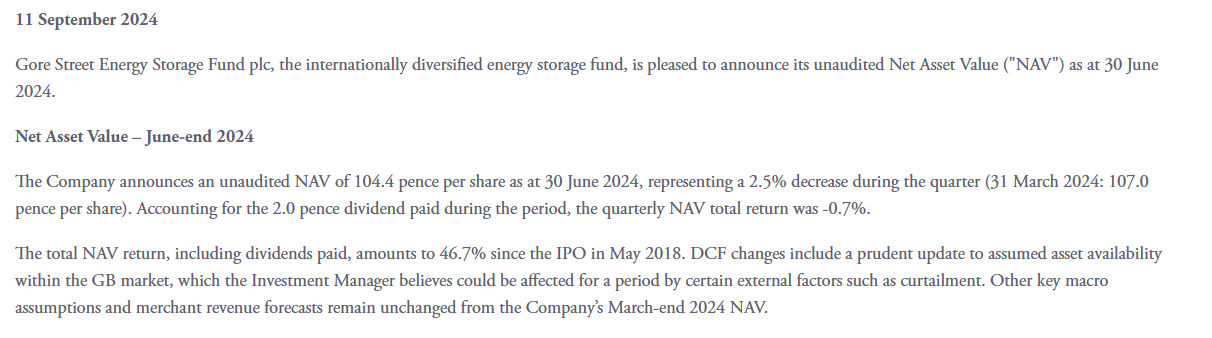

Looking at the last trading update, they still are paying a dividend and keep the NAV constant, but shareholders seem to be scared, too:

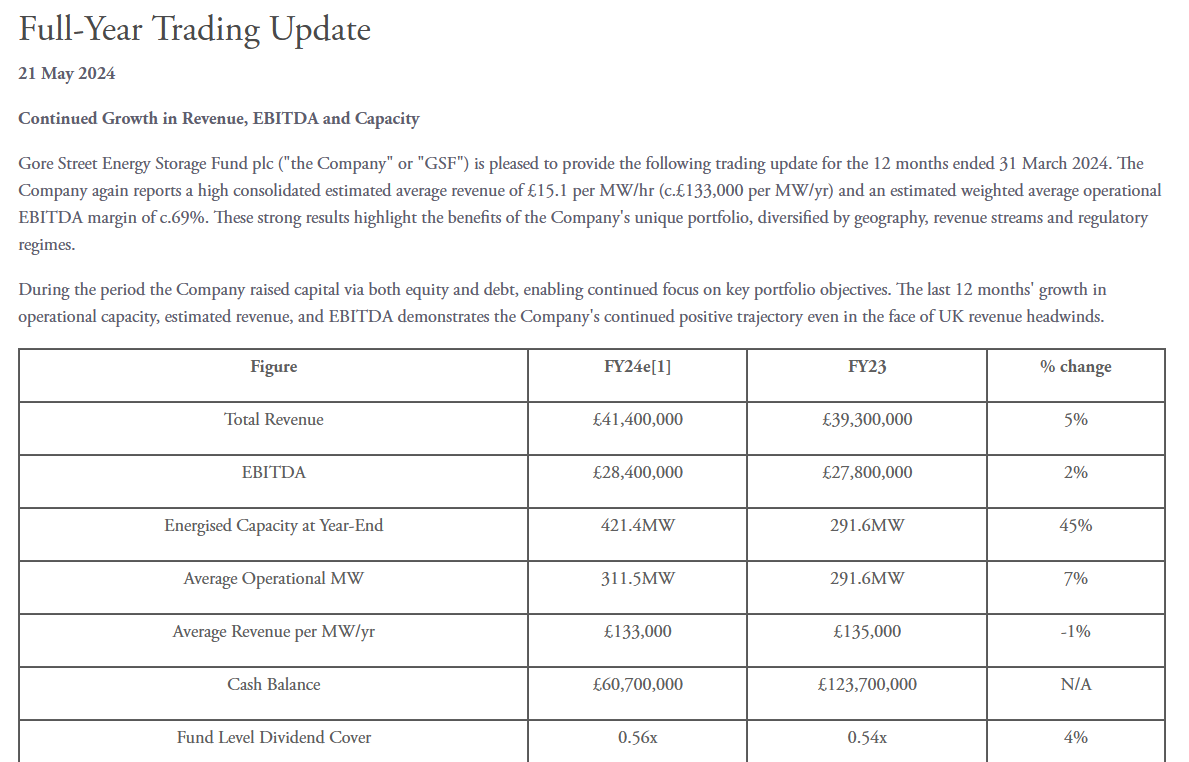

At a first glance, the Gore Street numbers seem to have held up a lot better than the Gresham ones:

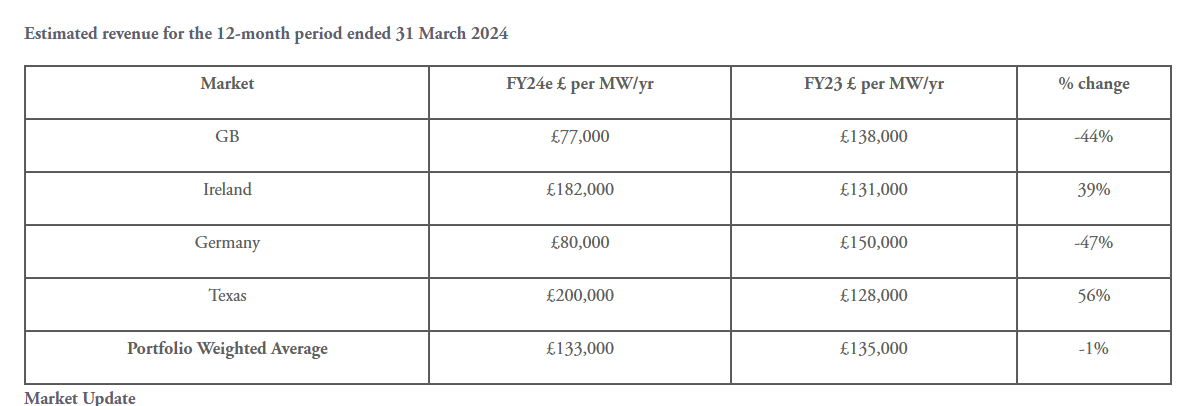

The main reason seems to be that they have diversified their portfolio across a few jurisdictions, where life seems to be (for now) more comfortable for BESS owners:

Learnings & Conclusion:

After the big Covid boom, the “New Energy Infrastructure” pendulum clearly has swung back massively into the other direction. The example especially of the Gresham House fund shows that even BESS, currently still the hottest subsector, has its issues.

The comparison to the Gore Street fund however also shows that in such regulated markets, with large dependencies on other players such as grid operators etc., diversification across jurisdictions and markets can help to mitigate individual risks.

The example of the Gresham House fund also shows that in such new areas, things can turn quickly around. Especially the BESS “arbitrage” business model is very sensitive to new capacity. This is very similar to investment strategies that produce alpha for small amounts of money and then the alpha disappears if many investors find out about it.

So a first mover advantage in that area can dissolve very quickly as setting up and connecting BESS is not rocket science, and battery prices are declining quite significantly these days.

To be honest, I am not 100% sure how these declining battery prices will impact existing BESS assets. Especially once, Sodium Ion batteries become commercially available. Existing BESS installations do have planned replacement cycles of something like 8-10 years, which should benefit them. On the other hand, even more capacity might hit the market.

For the UK, some short term relief might be coming, but to me it is not clear if and when. National Grid admitted in a recent FT article that their computer systems are indeed not capable using all the available BESS capacity,

This first look at the two funds did not yield any actionable insight. Going forward, I will casually monitor both funds, however overall I do think the Gore Street guys seem to be more credible and seem to have the better strategy compared to the Gresham House guys.

It also appears that the Gresham guys were more aggressive because of the pending sale of the fund manager itself.

Overall, the stand-alone BESS business case seems to be quite risky in the current environment and should be rewarded through adequate risk premia.