{kind=link}

When Warren Buffet dies, 90% of his wealth will probably be invested in an index fund that tracks the final market, the S&P 500, to be actual[1].

However why would Warren Buffet, one in all historical past’s greatest inventory pickers and lively buyers, select such a passive technique for his immense wealth as soon as he’s gone?

There are a number of causes:

- 64% American merchants lose cash within the inventory market.

- Lively administration entails charges that erode the opportunity of actual revenue.

- Passive investing is affordable compared.

- The final market has supplied passive buyers with a gentle fee of return when averaged over a protracted time frame.

Buffet is so sure of the prevalence of passive investing that again in 2007, he made a wager with a cash administration agency in New York. He wagered that over a 10-year interval, the S&P 500 would outperform any 5 hedge funds grouped collectively.

10 years later, Warren Buffet shared in his letter to shareholders the outcomes of the wager: He’d gained.

So, suppose you had been to comply with the Oracle of Omaha and passively make investments out there. What common return are you able to anticipate?

The Common Inventory Market Fee of Return

Traditionally, the inventory market has been rising at a compound annual fee of 10%[2]. And, when you think about inflation, which normally hovers round 3-4%, the compounded annual fee of return drops to about 7% per yr[3].

Now, there’s rather a lot to unpack right here:

- How can we measure the inventory market fee of return?

- What’s the impression of inflation on an investor’s returns?

- How dependable are these averages?

Let’s take a better look.

How Do We Measure the Common Fee of Return?

Merely, we monitor a proxy, aka one thing consultant of the inventory market as an entire, and have a look at its development year-over-year.

Like most analysts, we use the S&P 500 as a stand-in for the broader market.

What’s the S&P 500 Index?

The S&P 500 is a basket of the most important 500 firms within the inventory market. These 500 firms characterize round 80% of your entire inventory market capitalization. In less complicated phrases, for each $100 put within the inventory market, nearly $80 leads to a type of 500 firms.

Because of this, the S&P 500 is an efficient illustration of the broader inventory market.

How Do We Monitor the Development of the S&P 500?

To start with, we monitor development over a selected time interval. So, if we have a look at the index’s development throughout a given yr, we’d have a look at the place the basket began initially of the yr and the place it completed by the top. The distinction provides us a development share.

As an example, in the event you invested $100 within the S&P 500, and one yr later, you collected $110, then the index would have had an annual fee of return of 10%.

Listed below are the annual charges of return of the S&P 500 over the previous 20 years:

| Yr | Annual return with dividends | Yr | Annual return with dividends |

|---|---|---|---|

| 2003 | 28.36% | 2013 | 32.15% |

| 2004 | 10.74% | 2014 | 13.52% |

| 2005 | 4.83% | 2015 | 1.38% |

| 2006 | 15.61% | 2016 | 11.77% |

| 2007 | 5.48% | 2017 | 21.61% |

| 2008 | -36.55% | 2018 | -4.23% |

| 2009 | 25.94% | 2019 | 31.21% |

| 2010 | 14.82% | 2020 | 18.02% |

| 2011 | 2.10% | 2021 | 28.47% |

| 2012 | 15.89% | 2022 | 18.01% |

Supply: Aswath Damodaran, NYU Stern Faculty of Enterprise

How Do We Perceive the S&P 500’s Annual Charges of Return?

As you go over the above desk, there are some things it is best to keep in mind:

- The returns range wildly from yr to yr. Some years noticed losses, corresponding to 2008 and 2018.

- Losses and positive factors aren’t equal. A 50% loss can wipe out a 100% acquire.

- The charges above take into the buildup of dividends in addition to capital positive factors.

- The above charges are nominal charges. They have a look at the returns earlier than contemplating taxes, charges, and inflation. If we deduct all prices incurred by buyers, we get the actual charges of return.

- The S&P 500 grows at an exponential fee, additionally referred to as a compounded fee, slightly than a linear fee. So, if it had a median annual fee of return of 10%, then it might develop by 159% inside 10 years, not 100%.

We will see that there are good years and dangerous years, as anticipated, however how do they common out over the lengthy haul?

What’s the Common Return Over Intervals Longer Than a Yr?

Annual returns are usually very unstable, so buyers want to examine long-term charges of return over 5 years, 10 years, and even 30 years.

The calculation is sort of related: You have a look at the place the index began and the place it completed. The distinction provides you the speed of return over that interval. So, if $100 invested within the S&P turned to $300 5 years later, then the 5-year fee of return can be 200%.

Nonetheless, issues get difficult if you calculate the typical annual fee of return over that interval. Bear in mind: Since investments develop exponentially, you possibly can’t divide the full return after 5 years by 5. As a substitute, it’s worthwhile to use this system:

🧮️ Common Annual fee of return = (((Complete return/100+1)^(1/variety of years))-1)*100

Utilizing the above system, one can find {that a} 200% 5-year return interprets to a median annual fee of return of 24.5%.

With that mentioned, listed here are the returns of the S&P500 over totally different time scales as of the time of this writing: (And, to make the numbers extra tangible, we included how a lot a $100 funding within the S&P 500 would have grown over that point interval.)

| Time horizon | Cumulative return | Common Annual Fee of Return | The return of a $100 funding |

|---|---|---|---|

| 5 years | 63.20% | 10.12% | $163.20 |

| 10 years | 239.79% | 12.9% | $339.79 |

| 20 years | 583.97% | 10.05% | $683.97 |

| 30 years | 1596.35% | 9.87% | $1696.35 |

There are some things price highlighting within the above desk:

- When taken over lengthy intervals of time, the typical annual charges of return of the S&P change into way more secure and constant compared to the annual returns we noticed above. They common round 10%.

- The cumulative 30-year return is nearly 3 instances the 20-year return despite the fact that the typical annual return is much less in the course of the thirty-year interval. This reveals two necessary issues: the ability of compounded development and the significance of time within the funding world.

- All of the above returns are nominal, in order that they don’t account for inflation.

Let’s see what occurs once we rectify that omission.

How Does Inflation Have an effect on an Investor’s Returns?

Inflation in an financial system raises costs, impacting the buying energy of cash. Because of this, $100 at the moment can’t even come near what that very same $100 may have purchased 30 years in the past.

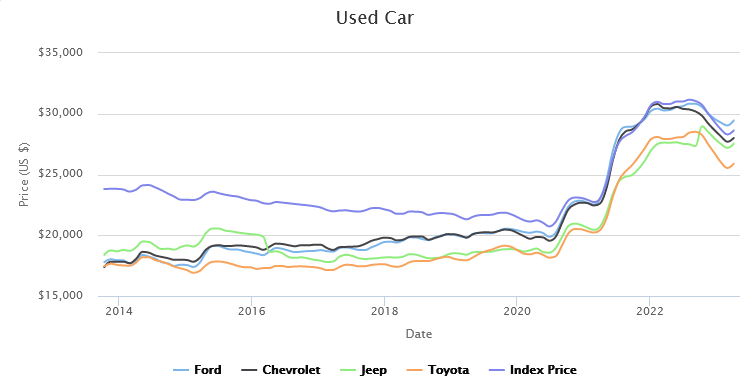

To see the impact of inflation, let’s have a look at the costs of used vehicles over the previous decade:

Supply: cargurus.com

Because the chart above reveals, whereas the costs of various manufacturers may need fluctuated over time, all of them elevated over the previous decade. So, you may need been capable of purchase an honest used Toyota for a bit of over $15,000 again in 2013, however at the moment, you’ll need a tad over $25,000.

Throughout that very same decade, $15,000 invested within the S&P 500 would have grown to $50,850, shopping for two Toyotas at at the moment’s worth.

And that is how inflation impacts your investments: In nominal phrases, your funding of $15,000 greater than tripled within the decade between 2013 and 2023. In precise shopping for energy, your funding barely doubled.

How Does Inflation Have an effect on the S&P 500’s Returns?

When economists measure inflation, they don’t depend on the used automobile market. As a substitute, they use one thing referred to as the client worth index, or CPI for brief, which appears at a number of client items and averages their collective worth. Then, they chart the rise in costs of the CPI to calculate the annual inflation.

Traditionally, the annual inflation fee within the states has been 3.8%.

Let’s see how this inflation fee impacts our S&P common annual returns:

| Time interval | Nominal annual fee of return | Actual annual fee of return |

|---|---|---|

| 5 years | 10.12% | 6.21% |

| 10 years | 12.9% | 10.03% |

| 20 years | 10.05% | 7.37% |

| 30 years | 9.87% | 7.21% |

Though the distinction between the nominal and actual returns might sound meager (in spite of everything, it’s solely 3-4%), this distinction turns into huge if you have a look at its cumulative impact. Listed below are the cumulative nominal and actual charges of return:

| Time interval | Nominal cumulative fee of return | Actual cumulative fee of return |

|---|---|---|

| 5 years | 63.20% | 35.84% |

| 10 years | 238.79% | 162.25% |

| 20 years | 583.97% | 316.95% |

| 30 years | 1596.35% | 712.11% |

| 50 years | 13,964.77% | 1,968.92% |

Inflation of 3-4 % will minimize your nominal cumulative fee of return by greater than half in thirty years. And if you wish to see how large of an impression inflation can have, have a look at the 50-year S&P return (the typical annual inflation fee over these fifty years was round 4%).

Can You Anticipate an Common Annual Return of 10% Subsequent Yr?

Effectively, the brief reply is not any.

The S&P 500 has supplied buyers with regular positive factors, however this consistency wants time to materialize. There are a couple of causes you shouldn’t anticipate the S&P 500 to give you 10% this time subsequent yr:

1. The Inventory Market is Unstable

As we noticed within the desk above, the S&P 500 could be erratic, churning out various outcomes yearly. However, in response to the above desk, listed here are some issues to note concerning the efficiency of the index over the previous 20 years:

- There have been 2 years when buyers misplaced cash, and one (2008) was so devastating that buyers misplaced greater than one-third of their cash.

- There have been 4 years the place the S&P 500 grew by solely single-digit percentages, corresponding to 1.38% in 2015 and 4.83% in 2005.

- There have been 5 years the place the index grew by 2.5-3 instances its common annual fee of 10%.

- Solely 2 years, 2004 and 2016, fall within the common vary we’d usually anticipate.

- Plenty of the wild swings could be attributed to world occasions we will all keep in mind. As an example, the 2008 plunge is because of the monetary disaster. When COVID-19 first hit, the inventory market skilled a brief bear market, shedding nearly one-third of its worth in a month!

These fluctuations can have a dramatic impression in your returns.

2. Market timing Can Have an effect on Annual Returns

As we simply noticed, the inventory market just lately misplaced round 35% of its worth in a single month. So, in the event you had invested $100 within the S&P 500 in April 2019, all of your positive factors for 2019 would have been worn out by that month, and your annual fee of return by March 2020 can be -8.81%.

And that is the issue: Massive occasions, outliers, and black swans can skew your outcomes. Market timing issues rather a lot.

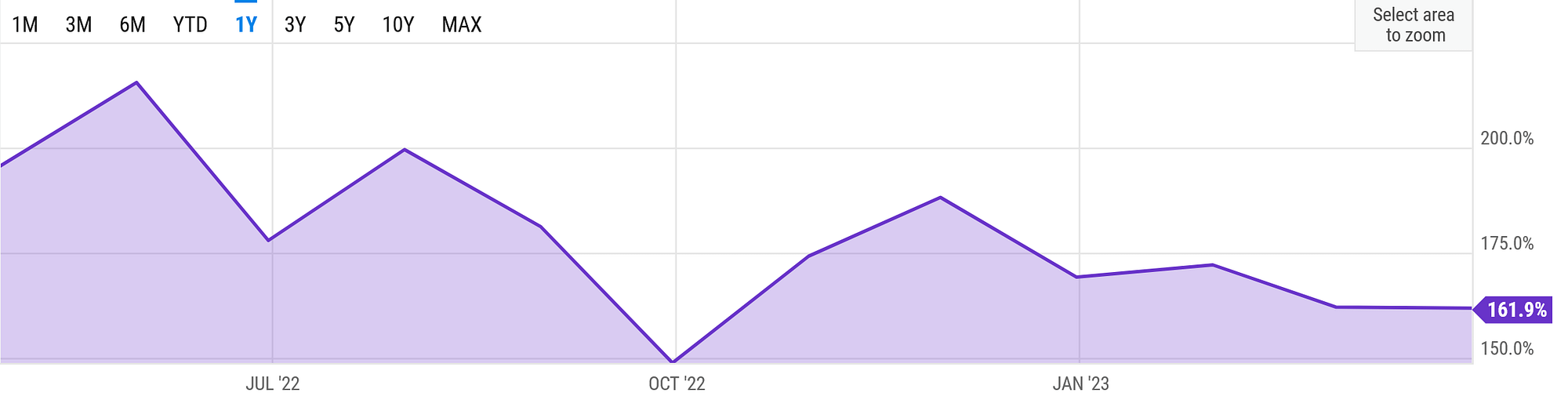

Even whereas researching this piece, I discovered the S&P 500 5-year and 10-year returns to range tremendously, relying on if you measured them.

10-year common inventory market returns during the last yr have been unstable.

Supply: Y-charts

If I had measured the cumulative 10-year S&P return again in Could 2022, I might have discovered it to be greater than 200%.

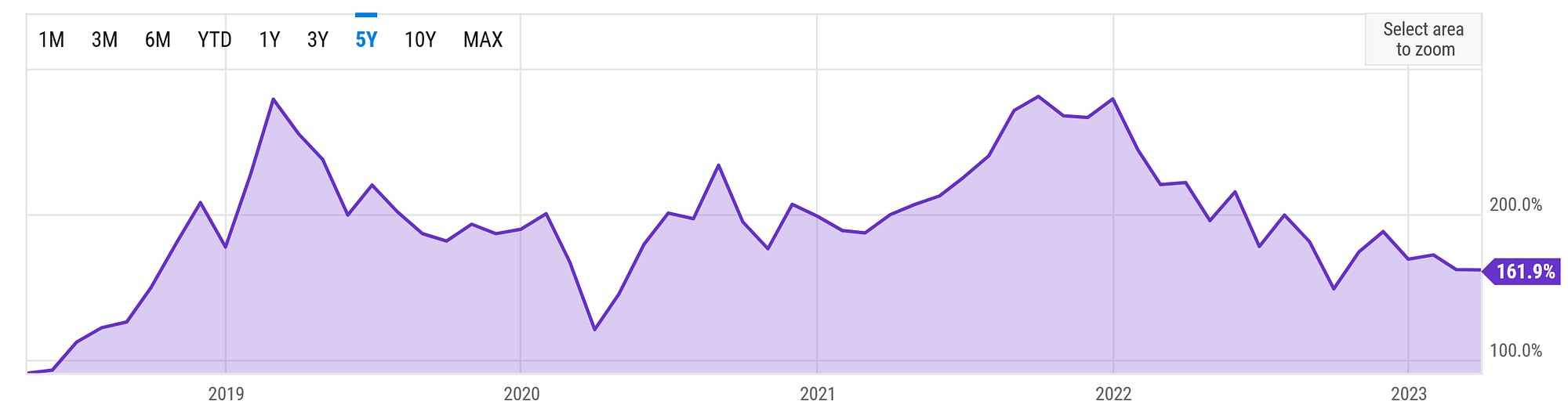

And, if we even take a step again additional, we’ll see bigger fluctuations:

10-year common inventory market return over the past 5 years is much more unstable than its 1-year counterpart.

Supply: Y-charts

To see the impact of market timing in motion, have a look at the above graph, and deal with the correct half. You’ll see a big peak proper initially of 2022, putting the 10-year return at nearly 300%. So, what occurred finish of 2021 and early 2022 to trigger this sudden plummet?

Effectively, rather a lot, truly:

- For starters, Russia attacked Ukraine, crippling provide chains around the globe.

- Individuals got here out of quarantine to seek out the Fed grappling with raging inflation by elevating rates of interest, and rising rates of interest have a tendency to harm over-leveraged firms.

- There have been additionally looming considerations about China’s financial system.

And the massive downside was that these occasions, these outliers, had been unpredictable. Granted, the rising tensions between Russia and Ukraine may need raised the alarm, however we nonetheless had been by no means 100% positive whether or not Russia would pull the set off or not. Equally, whereas we will all speculate over whether or not the Fed or the central financial institution will elevate rates of interest, we’re by no means sure till it occurs.

All that is to say that timing the market successfully is nearly not possible.

So, in the event you can’t time the market, then what do you have to do?

How Can You Make the Most Out of Passive Funding?

The excellent news is that even in a unstable market the place the effectiveness of an lively technique is questionable, there’s loads that you are able to do as a passive investor.

1. Bear in mind That Time Is On Your Aspect

If there’s one factor you are taking away from this piece, then let or not it’s this: Purchase and maintain your funding for so long as you possibly can as a result of time is at all times in your aspect.

On the one hand, the longer your funding time horizon is, the extra doubtless the market fluctuations will even out, netting you the anticipated annual fee of return we talked about.

However, if you go away your cash invested for a protracted time frame, you might be letting compounding work its magic. To drive the purpose house, I need you to go over the above tables once more and see that whereas the 30-year S&P return was a decent 1596.3%, the 50-year S&P 500 return was a shocking 13,964.77%.

2. The Market Will Fluctuate

Having simply highlighted the significance of staying out there for a couple of a long time at the least, we have to discuss how one can deal with the inevitable ups and downs that include investing.

Anytime one thing occurs out there, your first intuition may be to attempt getting forward of it, corresponding to exiting when the market appears that it’s about to plunge. Nonetheless, following these instincts may do you extra hurt than good.

To start with, we simply talked about that timing the market is sort of not possible for the skilled investor, not to mention for the typical Joe. And, to make issues worse, your margin of error is slim to non-existent.

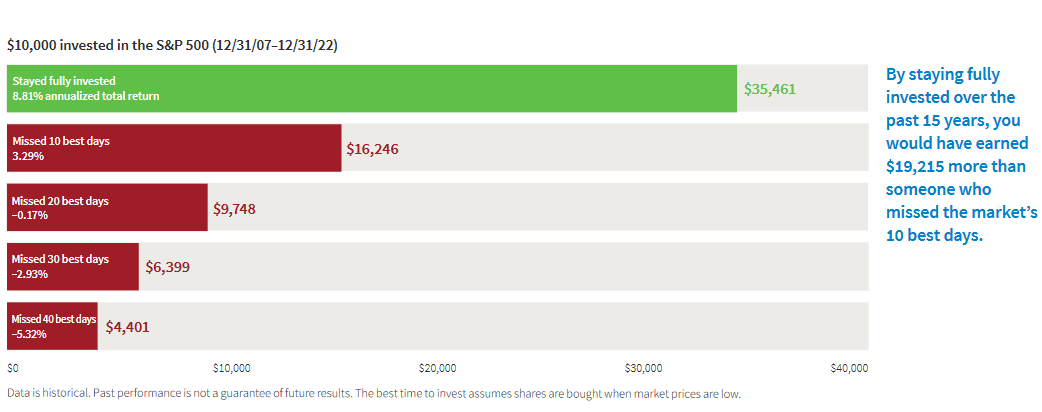

Lacking simply 10 days out of the previous 15 years would have been sufficient to wipe out greater than half of your income throughout that 15-year interval.

Supply: Putnam Investments

I need you to take a second and actually attempt to recognize what the above graph is attempting to say. In the event you had missed solely 10 days out of the previous 15 years, your cumulative return on funding for these 15 years would have been round one-quarter of the returns loved by somebody who had left their cash out there for your entire interval. That’s a margin of error smaller than 0.2%

And, in the event you had missed the 20 greatest days of the market, you’ll have ended up shedding cash after these 15 years.

So, you wish to consider the market like a wave that goes up and down, and your job is to journey each the crests and troughs of that wave. When the market is doing properly, keep in mind that that is solely short-term, and don’t get too excited. When the market goes down, don’t promote your belongings, and be affected person.

Placing It All Collectively…

On common, the inventory market provides you with a median annual return fee of 10%, which turns into nearer to 6-7% if you account for inflation. Nonetheless, you possibly can’t get pleasure from these charges of return until you might be keen to remain invested for the lengthy haul and stick out the dangerous instances. In brief, it’s worthwhile to develop a time horizon of a long time, not years.

And, in the event you ever doubt the ability of compounding over time, simply keep in mind that Warren Buffet made 90% of his wealth after turning 60, which is similar 90% that can discover its method into the S&P 500 when the Oracle of Omaha is not with us!