{kind=link}

Looks as if everybody on Twitter (in the event that they didn’t simply disappear already) scrambled to publish their 2022 returns this yr, both to bury a horrific end result within the New 12 months’s rush, or as a result of they’re one of many few who can boast a minor loss (or perhaps a acquire!) final yr. As all the time, particularly in the event you’re nursing your personal portfolio (& delight) after an excruciating yr, it’s best to take all of this with a grain of salt…as a result of, alas, it’s Twitter’s job to floor the outliers & the blowhards, so #FinTwit is certainly NOT a great (and even correct) benchmark to reference as an investor in good years, not to mention unhealthy.

However as all the time, I’m right here with a real/auditable portfolio, the place all modifications (if any) to my disclosed holdings have been tracked right here & on Twitter on a real-time foundation, for over a decade now. [Seriously, if you’re a new reader, take a peep: There’s countless posts on old & current portfolio holdings, plus my entire investing philosophy & approach…some of which may even be useful & interesting today!] And this yr, my important (selfless) function is to make you are feeling higher about your personal efficiency. ‘Cos yeah, you most likely did significantly better than me…and in the event you didn’t, possibly it’s best to query your investing decisions!? And I need to remind you: a) it could possibly be worse, there’s loads of unhealthy ‘traders’ on the market who’ve been trapped in a savage bear marketplace for two years now (since Q1-2021), and b) as soon as once more that, esp. noting the previous yr, no person is aware of something…

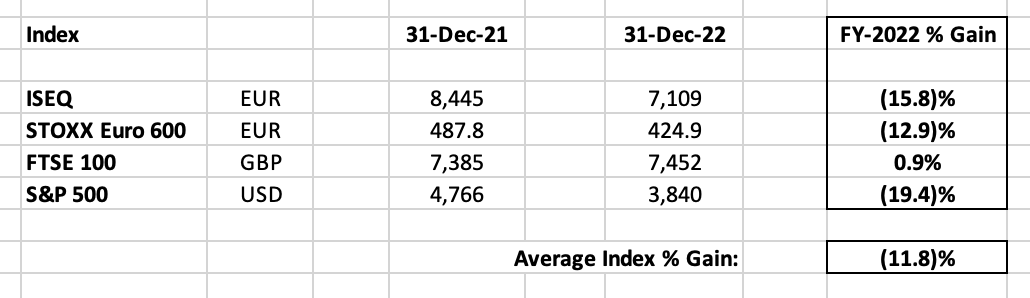

So let’s soar proper in, right here’s the harm in benchmark phrases – my FY-2022 Benchmark Return continues to be* a easy common of the 4 important indices which finest signify my portfolio, which produced a benchmark (11.8)% loss:

[*NB: As I flagged this time last year, I adopted the STOXX Euro 600 as my new European index in 2022.]

This general (11.8)% benchmark loss is considerably misleading, because it was considerably offset by the worth bias within the European index, and significantly within the FTSE 100 index which really managed to squeeze out a acquire for the yr. [Though notably, for US investors, this was offset by the dollar’s perverse strength, so there’s still little chance of seeing them diversify away from their all-in home-bias]. It was additionally mitigated by the resilience of many large-cap sectors, similar to shopper staples. Whereas down under, in smaller-cap/risk-on components of the market, the carnage was a lot worse…the FTSE 250 was down (20)%, Russell 2000 was down (22)%, MSCI Rising Markets USD Index was additionally down (20)%, whereas the MSCI Frontier Markets USD Index was down (26)%. The AIM All-Share Index did even worse, with a (32)% loss – for as soon as, silencing many of the perennial #UKFinTwit winners – whereas the crypto market’s Complete Market Cap collapsed by (64)%.

That is what occurs when the Fed defies expectations, and many years of market historical past, to maintain elevating rates of interest…producing a near-250 bps rise within the 10 12 months UST to three.88% as of year-end (after peaking at 4.33% in October). And no person actually noticed it coming…who’d have thought Powell would really attempt reimagine himself as Volcker-reincarnated?! As soon as once more, ‘Don’t struggle the Fed!’ proved the perfect piece of market knowledge. However that being stated, I’d should disagree with (some facets of) the consensus. I feel the entire larger rates of interest/decrease DCFs view of the market is much too naive (& quantitative) – whereas risk-free charges (& fairness threat premiums) clearly transfer larger or decrease, typically for years at a time, I feel it’s foolish to imagine some implied long-term market low cost charge simply marches up & down in lock-step. [And I note the same people who insisted the market shouldn’t have rallied over the years on QE-induced zero/negative interest rates, are the same people who insisted the market should & did collapse in the last year because of rising interest rates!?] In actuality, human worry & greed continues to be the first market driver – an surprising Fed stance sparked confusion & fears of upper rates of interest, decrease market costs, slower progress & potential recession, which ignites promoting, then promoting begets promoting, and shortly worth is fully driving narrative…and this spiral continues to feed on itself, ’til we lastly attain some kind of capitulation. [I don’t agree with the doomers who insist the next leg of a #GFC repeat-meltdown is coming…there’s nothing like the same leverage in the banking/financial system today].

I’m additionally puzzled by the disconnect between the Fed’s ultra-aggressive charge hikes, and traders (& voters) shrugging their shoulders over one other debt ceiling contretemps in Congress. How do you sq. tight financial coverage with an unprecedented & ultra-easy fiscal coverage – a $1.4 trillion finances deficit final yr (the actual fact it’s down from a $3.1T+ pandemic peak doesn’t make it any much less unhealthy), fairly probably a bigger finances deficit this yr, and $31.4T of presidency debt now excellent (on which the run-rate price might simply be an extra $0.5T authorities spending at right this moment’s rates of interest). To not point out, a ‘tight’ financial coverage isn’t what it seems in actual phrases both – with inflation nonetheless at 6.5% (vs. a 3.68% 5 Yr UST right this moment), from a 9.1% peak final June. For my part, we’re simply a distinct model of the same old US Presidential cycle: 12 months two is if you tighten – after 50+ years of deficits (& a pandemic spending frenzy), authorities’s completely incapable of doing that by way of fiscal coverage. Biden was additionally doing actually badly within the polls…for a lot of causes, however not-so-transitory inflation was the obvious & palatable cause, and combating it could additionally complement the entire ‘combating for the employees, and punishing the millionaires & billionaires’ narrative. Due to this fact, I think the White Home required an always-compliant Powell (who was additionally looking for re-appointment) to tighten by way of shock & awe rate of interest hikes, setting the stage for falling inflation & the chance to once more juice the financial system & market in 2023 (in response to a possible recession, which hopefully the market’s already discounted anyway), and ideally a glide-path to profitable Democratic elections in 2024. If I’m making Biden sound extremely sensible right here, I’m actually not…as with most politicians & authorities, most of this occurs by default (& by the seat of their pants), i.e. they repair the obvious looming downside, then repair the subsequent looming downside that resulted from them fixing the final downside!

Frankly, I feel expertise innovation & deflation (really, an excellent factor!) will preserve bailing us out right here, particularly now we stand on the cusp of the Fourth Industrial Revolution. I think we might look again in time on this era as simply one other blip on the financial/market charts, and persuade ourselves we’ve really invented a brand new paradigm of near-unlimited (pandemic-inspired) spending & debt, whereas additionally studying to regulate inflation (as soon as once more). And I’m nonetheless not satisfied this isn’t simply one other leg within the best bubble ever…

However c’mon, why do you have to hearken to anybody preach about big-picture macro, not to mention me…who bought blindsided by the Fed final yr, and severely underperformed my benchmark index. No one is aware of something, however we’re all the time fooled into pondering the macro outlook will probably be a lot clearer as soon as/if we are able to simply get previous the subsequent few tough/complicated months forward…so all we are able to actually do is deal with stock-picking, diversification & increase the psychological resilience to be a real long-term purchase & maintain super-investor.

OK, that’s sufficient bitching, moaning & excuses – right here’s the true harm – my very own Wexboy FY-2022 Portfolio Efficiency, when it comes to particular person winners & losers:

[Gains based on average stake size (with TFG the only portfolio holding that marginally changed, due to its DRIP) & end-2022 vs. end-2021 share prices. All dividends & FX gains/losses are excluded!]

[*Alphabet end-2021 share price adjusted to reflect the 20-for-1 stock split in Jul-2022. **Donegal Investment Group FY-Gain adjusted to reflect 46.2% of o/s shares redeemed at €15.30/share in Feb-2022.]

And ranked by measurement of particular person portfolio holdings:

And once more, merging the 2 collectively – when it comes to particular person portfolio return:

And yeah, that’s a savage (44.8)% loss for the yr…

And it particularly displays a expertise bear market (crypto is simply early-stage tech), with my different portfolio holdings’ positive aspects & losses really offsetting one another – what higher argument is there for extra (not much less) diversification? Particularly when my underperformance is fully attributable to KR1 – remove this holding, and my portfolio loss would even have been restricted to (13.7)% & broadly according to my benchmark. However in fact the haters who dismissed & excluded KR1 as a dumb outlier YOLO guess when it produced blockbuster returns/outperformance in my portfolio will flip up like unhealthy pennies to scrupulously insist it ought to clearly be included now…

Extra pretty although, they will question a 24.0% portfolio allocation to KR1 firstly of final yr, which now appears to be like inexplicable & irresponsible…what the hell type of diversification was that?! However I’ve been very express about this…for readers, followers & present/potential KR1 traders, I’ve repeatedly emphasised a 3-5% KR1 holding is completely adequate as an affordable/diversified crypto allocation in virtually any portfolio. However personally, my internet price base in KR1 is negligible (so proper or incorrect, I’m just about betting house-money right here), it’s nonetheless an enormous multi-bagger for me, it’s nonetheless so early for crypto & KR1 and each proceed to supply uneven risk-reward potential, and in actuality the draw back threat right here gained’t finally influence the general well being & wealth of my portfolio…as Invoice Gurley famous lately ‘you may solely lose 1x’ on a holding, and it’s extra vital to ‘take into consideration what might go proper’! So sure, this has clearly proved to be a painful outlier resolution within the short-term, however massively rewarding within the longer-term (& nonetheless to return, I anticipate!).

And oddly sufficient, my Alphabet holding’s given me extra heartburn…not as a result of I ever thought of bailing out of it, however as a result of realistically I by no means anticipated to see the inventory decline a lot in a single yr. And I don’t know whether or not this is sensible or not, however when $GOOGL is down (39)% & barely outperformed my general (45)% portfolio return, KR1’s collapse doesn’t really appear so distinctive in spite of everything. And KR1’s efficiency right here is within the context of my disclosed portfolio, so fortunately its influence is mitigated IRL…i.e. it’s clearly a considerably smaller holding in relation to my precise general disclosed & undisclosed portfolio. I used to be additionally blessed with two undisclosed holdings which have been vital out-performers final yr, in absolute & relative phrases – each are (primarily) #content material firms & Prime 5 portfolio holdings for me right this moment (the truth is, one has surpassed Document plc to grow to be my prime holding), which is an astonishing end result in a yr the place the headline content material firms ($DIS, $NFLX, $WBD, $PARA) really declined by (50)% on common!

However once more, the shares/efficiency that matter listed below are what you discover in my auditable/disclosed portfolio…and as all the time, we are able to’t focus/obsess an excessive amount of over a single calendar yr’s return, irrespective of how good or unhealthy. What actually issues is what comes earlier than (& finally after)…the buried lede right here is my efficiency punchline, right here’s my Wexboy FY-2020 Portfolio Efficiency:

And my Wexboy FY-2021 Portfolio Efficiency:

In a really perfect world, after a +56.4% acquire in 2020, adopted by an additional +133.8% acquire in 2021, clearly you’d money out every thing on the prime, nod off on an enormous pile of cash, and wait fortunately & patiently for the subsequent bear market capitulation. Alas, investing (& actual life) is simply not like that – besides in a few of these old-school funding newsletters, apparently – and if I attempted to play that sport, I’ve little religion I’d have the precise psychological fortitude & sheer bloodymindedness required to hold on & rack up these type of positive aspects. However our minds all the time need us to consider we are able to have our cake & eat it too – and naturally we simply KNEW the present bear market was coming – however that’s our brains bamboozling us with hindsight, and our brains helpfully forgetting all the opposite (imaginary) bear markets we noticed coming & all our beforehand botched market timing adventures. It’s a easy reality: If you happen to ever hope to make large long-term multi-bagger positive aspects, you need to settle for you’ll additionally undergo large reversals alongside the way in which! And in the long run, bearing that in thoughts, I can fortunately settle for & rejoice what’s turned out to be a cumulative/internet +102% acquire during the last three years!

And now, because it’s been a full yr – my apologies for skipping my regular mid-year evaluation in 2022 – right here’s an up-to-date have a look at every of my disclosed portfolio holdings:

FY-2022 (22)% Loss. 12 months-Finish 1.3% Portfolio Holding.

Saga Furs kicked off final yr buying and selling on a sub-4 P/E & wanting primed for continued positive aspects, after a pandemic bounce-back delivered its finest income & earnings in recent times (FY-2021 public sale gross sales of €392M & €3.63 EPS). Alas, poor auctions subsequently erased hope of a sustained restoration, and sank the inventory, with traders presuming extra of the identical cyclicality we’ve seen during the last decade+, as Chinese language producers (& patrons) got here to dominate. Fortuitously, a late surge in demand (Sep sale was up 100%+ at €123M) & continued rationalization produced a (optimistic) revenue warning, with FY-2022 now marginally worthwhile (as confirmed late final week).

Whereas that is excellent news, the FY-2022 outcomes clearly don’t transfer the needle right here. That’s irritating, as my authentic/core funding thesis that Saga Furs was a singular public sale home enterprise in a distinct segment luxurious sector was appropriate…regardless of all of the ‘however it’s fur!’ doubters. Saga sells extra pelts now than a decade in the past, not forgetting a Millennial technology who went gaga over fur-trimmed Canada Goose coats (with $GOOS peaking at an $8B market cap some years again)! However I didn’t anticipate the Chinese language imposing a step-change in fur costs (decrease), or shoppers embracing decrease costs for poorer high quality/welfare pelts.

Meaning Saga stays, within the absence of a value-realization occasion, a micro-cap worth inventory…however not a price entice, because it continues to generate earnings (on common) & its sturdy steadiness sheet helps a better dividend payout. It was on a large 17% yield – however the brand new proposed dividend is insignificant – and averaged a €0.70/5.9% annual dividend over the earlier 5 years. It additionally trades at a near-50% low cost to its newest €22.82 fairness/share, which I stay assured could possibly be wound down comparatively rapidly for 100+ cents on the euro, if an final commerce/PE sale doesn’t materialize right here (which appears to be the top end result for its defunct Danish rival Kopenhagen Fur, with no apparent signal of a purchaser for its legacy enterprise/model).

ii) Donegal Funding Group ($DQ7A.IR)

FY-2022 +23% Acquire (exc. share redemption). Yr-Finish 1.3% Portfolio Holding.

Have you ever ever seen such a profitable funding (a low-risk six-bagger in a decade) find yourself such a small place in a portfolio?! Looks as if a contradiction, however attests to how efficient a share cannibal Donegal’s been through the years (by way of share redemptions), and the way unhealthy I used to be at accumulating extra shares to exchange those I ‘misplaced’ alongside the way in which. And serves as a irritating reminder of how simple it’s to get waylaid into shopping for new & extra thrilling holdings as an alternative, and the way averaging up on a great inventory (even a multi-bagger!) might be such a great funding proposition.

With the sale of Nomadic Dairy in late-2021, and one other €20 million share redemption in early-2022 (at €15.30/share, for 46% of the corporate’s excellent shares), we’re near the end-game right here. Certain, I’ve most likely stated that earlier than, however now it’s a matter of timing with one main deal left excellent, i.e. sale of the seed potato enterprise. This has triggered the elimination of the top workplace (& its workers) final March, for €1 million pa in price financial savings, with the CEO & CFO retained by way of non-executive consultancy agreements (whereas remaining on the board).

Seed potato income is fairly secure at €25.2 million, whereas present profitability’s impacted by COVID/supply-chain points – however in regular years, its working margin averaged within the excessive single-digits (& maxed out round 10%). Nevertheless, Donegal’s head workplace, board, listed firm bills, and so forth. is totally absorbed by its enterprise models, so seed potato margins have all the time included some/all of this vital cost-allocation. It additionally boasts a multi-year R&D pipeline, whereas its general IP portfolio is doubtlessly way more helpful within the arms of a bigger acquirer. [Management could also acquire the seed potato unit/Donegal in a final transaction, but I rely on engaged stakeholders like Pageant Investments/Nick Furlong (with an 11%+ stake) to ensure a fair sale process/price here.] Due to this fact, I peg the seed potato enterprise’ M&A price at a considerable premium to its income run-rate – along with €2.9M internet money, €1.3M of property/different investments & €2.4M of contingent consideration receivable in 2023 from the Nomadic sale (I think this displays a 50% haircut & a max. €4.8M consideration will probably be obtained), Donegal Funding Group stays a compelling/low-risk funding buying and selling on a €30M market cap.

iii) Tetragon Monetary Group ($TFG.AS)

FY-2022 +13% Acquire. 12 months-Finish 2.0% Portfolio Holding.

Tetragon Monetary was one other worth beneficiary – inc. dividends, my precise return was +18% final yr. However large image, nothing a lot has modified…investor sentiment’s persistently adverse – a traditional instance of worth driving narrative – with the relentless widening of Tetragon’s low cost to extraordinary ranges (a 66% NAV low cost right this moment) & a excessive dividend yield coverage through the years, much less & much less shareholders boast a capital acquire on the inventory, which escalates adverse sentiment & generates new (& typically false/irrelevant) causes to promote.

In actuality, traders have loved +9.5%-10.5% long-term NAV/share returns, with administration returning a cumulative $800 million+ by way of share buybacks (inc. $67M final yr) – that’s $1.6 billion to shareholders, with dividends included. [Those dividends really add up…my average TFG entry price, net of dividends, is now sub-$4.75! Not to mention, I reinvest all dividends (at a huge NAV discount) via the company’s DRIP]. After all, administration might & ought to return capital way more aggressively…however what number of administration groups really shrink their empires? And administration’s (complete) voting management is a little bit of a purple herring right here – and never not like many well-known tech/media firms, which traders don’t hesitate to purchase – as with most long-term targeted owner-operators (principals & staff now personal 36.5% of TFG), public shareholders ought to settle for TFG will most likely strike a deal (or maybe get bought off piecemeal) solely when administration (primarily Reade Griffith, who’s nonetheless in his late 50s) decides it’s the best time, worth & acquirer!

So TFG’s a pretty funding for the best investor…one who takes benefit of the large low cost, focuses on long-term NAV returns (not simply the share worth), and acknowledges it’s now a guess on Tetragon’s $37.4B AUM different asset administration enterprise (& the compelling tailwinds it continues to take pleasure in). Its market cap is now simply 74% of the worth of its asset administration enterprise alone (the truth is, infrastructure supervisor Equitix accounts for 70% of TFG’s market cap alone), with an extra $1.4 billion+ funding portfolio thrown in totally free! And fund administration drives returns too, with a mean +7.0% NAV acquire in December during the last 5 years, primarily from an annual catch-up/revaluation of TFG Asset Administration. Clearly, it’s been a tricky yr – albeit, TFG NAV’s down simply (3.7)% YTD as of end-Nov – so we shouldn’t essentially presume that type of acquire this time ’spherical, however I already see a +1.8% NAV acquire from the $25M tender supply final month, and proceed to consider TFGAM valuations are affordable/applicable right here. We will see…the Dec factsheet is out Jan-Thirty first.

[NB: On a look-through/control basis, TFG actually owns about 91% of its current $37.4B of AUM vs. a $1.2B balance sheet value – back of the envelope, that’s a 3.6% of AUM valuation. Cheaper than you might expect, due to real estate/bank loan AUM – but accounting for that, overall it looks sensible in alt. asset management terms].

iv) VinaCapital Vietnam Alternative Fund ($VOF.L)

FY-2022 (13)% Loss. 12 months-Finish 5.6% Portfolio Holding.

As you’d count on, final yr’s bear market was punishing for a small frontier market like Vietnam – and exacerbated by tighter liquidity & an anti-corruption marketing campaign in the true property sector – the VN Index ended the yr down (33)%. This could have been compounded by a weak VND, which lastly succumbed (after years of stability) to the sturdy greenback final summer season, just for a outstanding late-year restoration that left the dong simply (3.7)% weaker in 2022. Fortuitously for traders, diversification saved the day, by way of: i) portfolio out-performance resulting from a considerable allocation (43% in combination) to unlisted/quasi-private fairness/personal fairness investments, and ii) sterling weak point, which was one other substantial tailwind regardless of a weaker VND. Some narrowing of the NAV low cost additionally helped…and inc. dividends, this restricted my loss to (11)%, a few third of the native index decline!

Which units us up properly for 2023: GDP progress was near +9% (& accelerating) on the finish of Q3, with FDI, export progress, retail & infrastructure spending all working at +13%-20% ranges, whereas inflation nonetheless stays effectively underneath management at simply over 4%. The market’s now buying and selling round an 8.5 P/E, a 40% low cost to regional friends & with continued 15-20% earnings progress. We might some slowdown in exports to the West this yr, however that appears prefer it’s already been aggressively discounted, and prone to be offset by continued post-COVID tourism progress & the stimulus of a China re-opening. The latter, in fact, is a reminder of my large image thesis…that Vietnam’s completely positioned as a nation & an financial system to be the #NewChina. Not solely can it substitute Chinese language manufacturing in world commerce (& duplicate the financial/funding trajectory of China in earlier many years), it might probably additionally outsource Chinese language manufacturing & be a possible (oblique) conduit for US-China commerce, if political & commerce relations proceed to undergo. VOF now trades on a 13% NAV low cost, and breaking the crucial 1,200 degree on the VN Index (we’re now simply over 1,100, after lately bottoming sub-1,000) is once more a key indicator for a possible multi-year bull market forward.

FY-2022 (39)% Loss. 12 months-Finish 8.3% Portfolio Holding.

I nonetheless discover it arduous to consider Alphabet’s 2022 decline was double the S&P’s!? However that is primarily a tech bear market…the truth is, for a lot of tech sub-sectors & traders, the bear market’s virtually two years outdated now (since Q1-2021). Fed charge hikes have eviscerated ‘jam tomorrow’ DCF valuations…and whereas clearly that’s an apparent set off, I feel it’s finally a little bit of a cop-out (per above). In actuality, it’s a bear market…so after a sure level, unhealthy shares infect good shares & even #BigTech, promoting begets promoting & worth actually drives narrative. [With negative sentiment re Facebook & Zuck’s all-in metaverse bet AND positive ChatGPT sentiment both impacting Alphabet negatively]. Maybe the larger problem for traders – which arguably we’ve dealt with fairly badly – has been the battle to handicap/worth the pandemic surge in digital/expertise revenues & income, and the inevitable post-pandemic slowdown since (we see this additionally in e-commerce shares, which have collapsed in response). Personally, with present & potential holdings, I’ve compelled myself to focus simply as a lot on 2019/pre-pandemic financials when evaluating their progress, prospects & valuations as of right this moment.

And Alphabet, it’s apparent income progress slowed considerably final yr. Nevertheless, the sturdy greenback had an inevitable influence, so it’s vital to additionally deal with cc income progress which slowed from +26% in Q1 to +11% in Q3, nonetheless a compelling progress charge. However that progress (& slowdown) comes on prime of +41% income progress in 2021 (to surpass $0.25 trillion in annual income!). And within the wake of +13% income progress in 2020. That’s an unbelievable income/enterprise trajectory…and to butcher Buffett, I’m completely pleased to just accept that type of lumpy income progress in any long-term holding! And the continued progress (& dominance) in Alphabet’s enterprise is simply as unbelievable. The $5.4B acquisition of Mandiant will proceed to reinforce its cyber-security status & alternative. Alphabet now provides 9 merchandise with 1B+ customers, six of which boast 2B+ customers. [All of which are basically free for users…worth remembering every time US/EU regulators (& jealous corporate peers) demonize Alphabet for its ‘abusive monopoly power’!] YouTube has now carved out a 9% share of complete viewing hours (within the US), because it continues to steal market share from TV, cable & different streaming providers, and assert itself because the dominant free & subscription streaming (& music streaming!) service on this planet. DeepMind is now transitioning to a industrial enterprise…in 2020 it tripled income in a yr, and in 2021 it quintupled income to $1.7 billion in simply two years! [Yes, it’s internal revenue from the rest of Alphabet, but I’m confident: i) it’s billed on (basically) arms-length terms, and ii) DeepMind could just as easily have opted to grow its business externally from day one, and just as spectacularly!] Now image its income in 2024, and what DeepMind’s implied valuation may be if we apply the identical 29 P/S a number of OpenAI’s apparently commanding in its new funding spherical (on a projected $1B income in 2024, vs. zero right this moment!).

As an alternative, $GOOGL bear market capitulants greeted the emergence of ChatGPT with horror…with worth driving narrative once more, prompting Twitter claims that Google Search is now useless! Which is a bit foolish – to not denigrate its spectacular output/progress, however ChatGPT additionally jogs my memory of the standard journalist, i.e. that bizarre mixture of copy & paste confidence & cluelessness. In actuality, Google Search has been/is the perfect AI in every day use on the planet – and has been particularly designed & refined to fulfill the respective wants & needs of customers, advertisers & Google – in our every day lives, we principally need easy details & figures backed up by authentic supply hyperlinks, whereas ChatGPT (very similar to journalists) serves up paragraphs & no hyperlinks!? But when that’s what customers now need & demand, I don’t doubt Google/DeepMind can ship – the truth is, I used to be already betting on a digital AI assistant subscription to return, harnessing & amalgamating Google Search, Voice, Cloud, YouTube, DeepMind, and so forth. Don’t be fooled by an method that’s extra tempered & accountable – as Yann LeCun lately famous, ‘If Google & Meta haven’t launched ChatGPT-like issues, it’s not as a result of they will’t. It’s as a result of they gained’t!’. I liken it to Waymo vs. Tesla – whereas Tesla FSD’s demonized within the media, and different firms pull again on their autonomous driving funding, Waymo retains its head down, continues to construct & is now the one firm with rider-only service (& no human driver) in a number of cities.

Within the short-term, we face (as all the time!?) an unsure outlook & a possible recession – however in that state of affairs, I consider Google & digital promoting are nonetheless poised to win a fair higher share of advert spend (from outdated media). To not point out valuation, $GOOGL trades right here on a sub-19 P/E & a 4.1 P/S a number of – vs. 30% unadjusted working margins – cheaper than most shopper staples multiples! It additionally presents a lot decrease regulatory/person threat than $META (for a similar P/E), and Different Bets spending/losses stays underneath management & ought to nonetheless be handled as (uneven risk-reward) venture-capital funding by traders. In the long run, AI’s clearly an unbelievable alternative – in addition to a possible risk – so long-term, I proceed to guess on what I consider is the perfect AI firm on this planet.

FY-2022 (75)% Loss. 12 months-Finish 8.4% Portfolio Holding.

What an abominable yr it’s been for crypto…and for KR1. It actually doesn’t matter whether or not it was really ready for a possible crypto winter & boasted a fortress steadiness sheet accordingly…in a bear market turbo-charged by deleveraging & fraud, traders have been all the time going to throw KR1 out with the bathwater. The unbelievable long-term alpha the workforce has delivered & will proceed to generate for shareholders is irrelevant within the eye of the storm, as a result of all that issues within the short-term is the unavoidable beta of a crypto collapse. Once more, that’s why my final write-up was titled ‘KR1 plc…the #Crypto #Alpha Wager’ – I proceed to advocate KR1 as the perfect listed crypto alpha generator on the planet, however this suggestion solely is sensible if/if you personally settle for & personal the beta of the underlying crypto market, i.e. have developed your personal conviction in blockchain as a foundational expertise, and have the precise sang-froid (& intestine) to stay with the inevitable draw back volatility of crypto. After all, most traders will declare that up-front…however alas, most by no means get to benefit from the large multi-baggers, as worry & greed inevitably shakes them out far too early, at finest with a revenue that appears tiny in hindsight, at worst they bail out on the worst attainable time & worth (bear in mind, all the perfect long-term performers appropriate 50%-90% alongside the way in which).

However anyway, regardless of the crypto winter, it’s enterprise as regular for the KR1 workforce. They proceed to examine extra gadgets off the laundry record – appointing a brand new auditor (PKF Littlejohn), including a brand new web site FAQs to handle excellent points/issues, including one other spectacular NED (Aeron Buchanan, who’s labored alongside Gavin Wooden on Ethereum, Polkadot & the Web3 Basis), and so forth. Additionally they settled KR1’s excellent 2020 & 2021 efficiency price liabilities, per the brand new govt providers settlement (which locks the workforce up solely with KR1), i.e. by way of the issuance of latest shares on the applicable NAV/share worth. [For example, a £30.1 million 2021 performance fee was settled via issuance of 24.6M new KR1 shares last July at 122.7p a share (vs. a market price of 26.5p at the time)]. This implies the workforce’s now earned (in combination) a 25%+ stake in KR1…and eventually has the pores and skin within the sport to replicate the owner-operator method they’ve taken from day-one (again when KR1 launched, the workforce did NOT grant themselves a free promote, not like most different crypto administration groups on the market). And most of this stake’s solely been transferred to the workforce within the final 13 months, within the midst of a crypto winter, so it’s solely now we are able to hope to see new incentives begin to drive new behaviour, e.g. higher Investor Relations to return, and ideally an up-listing finally to the LSE (or AIM) to broaden the potential pool of KR1 traders.

In the meantime, like true decentra-heads, the workforce’s averted the fraud, leverage & custody threat of centralized exchanges (like FTX) & continued to deal with new investments, their (parachain auction-focused) staking returns have been unbelievable with £21.0M earnings from digital belongings in 2021 & one other £16.6M in H1-2022, and the 8,000%+ share worth & 9,500%+ NAV/share returns they’ve delivered (since 2016) are each spectacular & incomparable (vs. different crypto shares, all of which have produced negligible/catastrophic returns for traders). And with so many crypto shares nonetheless heading for zero, I now name KR1 the ZERO funding thesis…it has zero {hardware}, zero energy-use, zero debt, (primarily) zero choices excellent, zero dilution (final inserting was in 2018!), zero liquidity points (loads of fiat/ETH/USDC liquidity available & $100s of hundreds of thousands of every day liquidity in its prime portfolio holdings), zero capital required (it funds its modest 2% expense ratio & generates income/free money stream from its staking operation), zero efficiency charges (’til NAV exceeds £215M once more), and 0 taxes (KR1 is Isle-of-Man resident).

For traders, KR1 was/is the one crypto inventory that may survive any crypto winter (irrespective of how lengthy & extreme), and proceed to ship multi-bagger returns within the subsequent crypto summer season to return, and nonetheless trades on an absurdly low cost valuation (vs. the 100%+ NAV CAGRs it’s really delivered)…the truth that KR1’s share worth has mainly DOUBLED since year-end attests to how compelling that pitch might be (when sentiment lastly improves). As all the time, I like to recommend a 3-5% KR1 holding as an affordable crypto allocation for nearly any portfolio.

FY-2022 +10% Acquire. 12 months-Finish 10.9% Portfolio Holding.

Below CEO Leslie Hill’s, Document went from energy to energy final yr. Whereas long-term compounding of its underlying AUME stays a secular tailwind, Document might be susceptible to market reversals too…nevertheless this tends to be mitigated by the truth that FX hedging mandates typically goal a core portfolio proportion/quantity (& are due to this fact comparatively proof against market losses), by new fund inflows & by some purchasers really growing hedge ratios resulting from market volatility. Nonetheless, final yr’s savage bear market (for the standard 60:40 portfolio) was fairly the headwind, however with the assistance/scaling up of a brand new $8 billion passive hedging mandate, Document’s $ AUME really hit new all-time-highs (as of end-Dec). This success was compounded by sterling weak point – a majority of Document’s AUME is in CHF, EUR & USD, which has served as an amazing post-Brexit sterling hedge for traders – with £ AUME up 13%+ yoy. The plan to reply extra to consumer wants, exploit long-standing relationships, and diversify into higher-margin/non-currency merchandise additionally progressed effectively, with the brand new (frontier market) Sustainable Finance Fund reaching $1B+ in AUM, together with the launch of a brand new Liquid Municipal Fund for German institutional traders (and with extra/related product launches to return). Administration’s even added slightly crypto pixie-dust, as deliberate – nice timing, and crowd pleasing for traders, if we’re really rising from this crypto winter – by way of some small seed/early-stage investments within the area to ‘get a seat on the desk’ & discover potential future product alternatives.

The P&L development is equally spectacular. For FY-2022 (to end-Mar), income was up +38%, working margin expanded from 24% to 31%, and each EPS & the entire dividend have been up 60%+. [Inc. dividends, my total return last year was actually +16%]. This momentum continued within the FY-2023 interims, with income up +35%, working margin at 34%, and EPS up +57%. The actual kicker is within the efficiency charges: Within the final couple of years, administration’s targeted on renegotiating (& successful) passive/dynamic hedging mandates to incorporate higher efficiency price potential, the place Document really provides worth by way of the tenor of its consumer hedging (i.e. by way of lively administration of FX ahead hedging length & arbitrage alternatives). With the growing post-QE normalization of curiosity & FX markets (i.e. higher volatility & dislocation!), Document can count on to earn such charges way more persistently…accordingly, it’s now earned efficiency charges for the final 4 consecutive quarters, together with £5.8M within the present FY-2023! The corporate now appears to be like set to repeat its interim efficiency, implying a 6.3p+ FY EPS, one more earnings shock. [Analyst estimates have not anticipated AUME growth, margin expansion, or performance fees]. After all, that is all per the CEO’s medium-term objective to succeed in £60M in income (from £35M in FY-2022) & a 40% working margin by FY-2025 – as defined in administration’s current Investor Meet displays & within the upcoming CMD. This could indicate continued 25%+ EPS progress in FY-2024 & FY-2025 to succeed in 10p EPS within the subsequent 2.5 years…that’s an unbelievable earnings trajectory, esp. if you evaluate it to Document’s potential/ex-cash (it now boasts 11p/share of internet money & investments) sub-14 P/E as of right this moment, for a real owner-operator enterprise (the CEO & Chairman nonetheless personal a 38% stake).

And now, to complete up, I need to return to an evaluation I final shared within the grim coronary heart of the pandemic. All of us speak on FinTwit about top quality progress shares, and what that truly means in quantitative (e.g. ROIC) & qualitative phrases (e.g. moats). And whereas I do know what I like in observe – excessive margin/asset-light firms which boast sturdy steadiness sheets & free money stream – I typically discover the dialogue itself fairly irritating. Qualitative evaluations can get very subjective very quick, whereas there’s no definitive quantitative display screen for prime quality compounders – besides maybe long-term inventory efficiency, nearly as good a filter as any, ‘cos winners actually do are likely to carry on successful! – and you may rapidly find yourself going ’spherical in circles anyway. For instance: Excessive ROIC firms typically commerce on excessive multiples, low ROIC firms typically commerce on low multiples…so RoI can simply find yourself being a considerably meaningless filter for figuring out true relative worth.

And I can’t assist pondering of what Buffett stated: ‘Investing will not be a sport the place the man with 160 IQ beats the man with 130 IQ’. The implied/unstated half right here is that what actually issues, given an affordable minimal IQ degree, is an investor’s EQ. i.e. Have they got the emotional intelligence to make persistently rational & unemotional choices, no matter private & market sentiment (or turmoil), and to acknowledge of their intestine (& not simply their mind!) that having/cultivating the persistence & sang-froid to easily purchase & maintain is what finally produces the perfect long-term returns? As Jesse Livermore put it so famously, ‘It by no means was my pondering that made the large cash for me. It all the time was my sitting’. And for me, this implies IQ is for purchasing, and EQ is for holding…which boils down to 2 key enterprise attributes that give me all of the consolation I would like to carry a top quality compounder by thick & skinny:

Excessive insider possession & sturdy steadiness sheets.

Proprietor-operators are administration, founders & founding households who focus totally on long-term funding & worthwhile income progress, sturdy free money stream conversion, organic-led progress vs. acquisitions, and a powerful worker & customer-centric tradition…and invariably on a powerful steadiness sheet, so you recognize they will & will survive & thrive by the worst of instances (& keep away from going bust, or diluting shareholders into oblivion). And better of all, they’ve actual pores and skin within the sport – not like common company administration, their (substantial) stake within the enterprise is much extra helpful than their annual compensation bundle – in order that they eat their very own cooking, they expertise the identical elation & disappointment as you do over the share worth, and every single day they sweat & each evening they get to put awake worrying in your behalf, as you sleep soundly figuring out they’ll proceed to compound your & their wealth as they’ve previously.

I like to recommend you return to my authentic/extra detailed commentary in 2020, so right here I’ll simply present two snapshots (& transient feedback) on how I’ve assembled my general disclosed/undisclosed portfolio…first, by insider possession:

By default, most listed firms (esp. mid/large-cap) should not owner-operators – administration/founders personal lower than 5%, and even lower than 0.5%, of the corporate – and investing in such firms, to some extent, is clearly unavoidable. There’s additionally (a lot rarer) firms, whose owner-operators management a dominant 50%+ stake – these require a better funding hurdle, and a crucial filter is how administration’s really handled minority shareholders previously. However exterior these two extremes, there’s a really perfect possession vary of 5%-50% – and specifically, a candy spot the place insider possession is between 20%-40% – it’s taken years of labor & persistence, however 65% of my present portfolio is co-invested alongside such owner-operators.

And by steadiness sheet energy:

Granted, 13% of my portfolio’s invested in holdings with 1.0+ Internet Debt/EBITDA multiples….part of the market the place (US) FinTwit appears to spend most of its time?! And one other 18% is invested in 0.0-1.0 Internet Debt/EBITDA firms, and/or sub-25% (on common) Internet Debt/Fairness firms, which appears an affordable degree of threat to take. However that leaves 69% of my portfolio invested in firms that take pleasure in (vital) ranges of steadiness sheet internet money & investments (vs. present market caps) – a crucial monetary attribute that’s invariably under-priced & under-appreciated – with near 50% of my portfolio really invested in firms that boast 7.5%-30% of their market cap in internet money & investments!

These are some good treasure chests, guarded by motivated owner-operators, and hopefully surrounded by respectable moats! Hopefully they encourage you to understand these particular attributes, and/or discover different standards that make sense/show you how to to really purchase & maintain top quality compounders. And I’ll say it once more: If you happen to ever hope to make large long-term multi-bagger positive aspects, you need to settle for you’ll additionally undergo large reversals alongside the way in which! Having/cultivating the persistence & emotional intelligence to stay with that dichotomy is crucial…for me, it’s been the true key to the multi-baggers I’ve loved in my portfolio, to my +102% internet return within the final three years, and (regardless of the apparent reversal since) to my +26% pa decade-long funding monitor document I celebrated simply over a yr in the past.

Right here’s to an amazing 2023…