{kind=link}

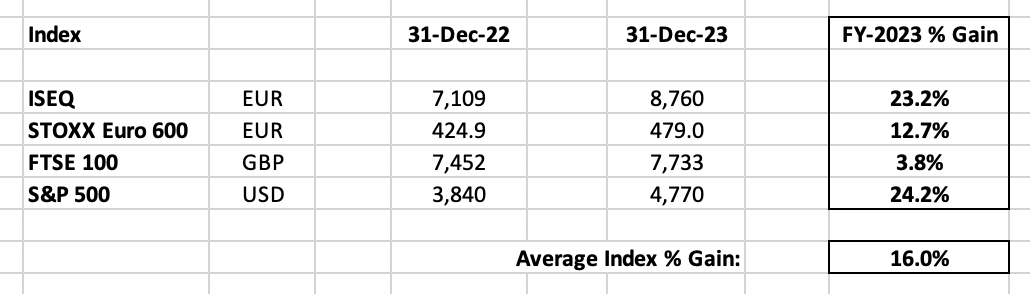

Effectively, 2023 clearly proved (as soon as once more) that no one is aware of something, so let’s skip the waffle & leap proper in – my FY-2023 Benchmark Return continues to be a easy common of the 4 principal indices that greatest symbolize my portfolio, which produced a benchmark +16.0% acquire:

The respective index rankings for the 12 months have been truly fairly typical. The S&P 500 was the clear winner, clearly pushed by the Magnificent Seven & a normal restoration in know-how shares (from a bear market that stretched way back to early-2021), as confirmed by a spectacular +44% acquire within the Nasdaq. Each the ISEQ & the STOXX Euro 600 have been led by the US, with the previous having fun with a very glorious return, truly benefiting (perversely) from large-cap revaluations as they ready to delist from the Irish market. In fact, the FTSE 100 was the perennial under-performer, whereas UK smaller corporations didn’t look any higher on common, with the FTSE 250 scraping out a +4.4% acquire whereas the AIM All-Share in some way managed an extra (8.2)% decline. [The Russell 2000 also under-performed, but still posted a very nice +15% gain in absolute terms]. In any other case, going out the danger curve, the MSCI Rising Markets USD Index loved a +9.8% return, the MSCI Frontier Markets USD Index was up +11.6%, whereas crypto blew the lights with a +108% acquire in complete market cap (pushed primarily by a +156% acquire in Bitcoin).

In fact, the backdrop to all of this was the surprising revival of a Goldilocks state of affairs for the US economic system/market. The inevitable recession (for typically undefined causes?!), as predicted by 9 out of 10 economists, by no means arrived…first they delayed it, and now even the economists appear to be giving up on it (it’s an election 12 months, in any case). As an alternative, we have now strong US progress & full employment, whereas inflation spiked proper down once more to an inexpensive 3.4%, and the market eagerly began anticipating Fed cuts in 2024. Which might all be summed up by the 10 12 months UST round-tripping to finish the 12 months down a single foundation level at 3.87%! Regardless, Biden continues to spend like a drunken sailor, nonetheless working $2-$3 trillion finances deficits, with the US nationwide debt now surpassing $34 trillion. [Just to be non-partisan, both parties are fiscally incompetent today & both share the blame for the debt with only two Presidents running an actual (rounding error) budget surplus in the last century!]

However like I stated, no one is aware of something…you actually are higher off ignoring macro 99% of the time, and devoting 99% of your time as a substitute to your portfolio. The one macro ‘conspiracy idea’ I need to share is to once more debunk the current/ridiculous notion that Powell is in some way an inflation-busting incarnation of Volcker. I don’t suppose that’s true in any respect, I feel he’s Biden’s whipping boy. Sure, the aggressive Fed hikes have been clearly essential to suppress the more and more unpopular inflation spike, and to strive offset a few of Biden’s continued fiscal incontinence – the quid professional quo was that Biden wouldn’t query/struggle increased charges – however this was additionally only a typical mid-cycle tactic of Presidents & politicians, they usually wager on the inflation spike being a brief post-COVID provide chain & welfare boondoggle/minimal wage hike phenomenon (& truly gained the wager!).

So why does this matter…as a result of now I feel the Fed put is again! Whereas reducing charges could show dangerous, and can clearly be path-dependent, it’s clear from the rhetoric (& ways) already ratcheting up that that is an all-or-nothing election 12 months…and Powell stands able to do no matter it takes. So the US continues to be place to be, however post-election I believe there’ll be a compelling case to contemplate aggressively re-allocating & diversifying your portfolio threat/publicity, i.e. globally, and by (area of interest) sector/asset class. [Unfortunately, US investors will mostly ignore this strategy]. That’s my sport plan…however as all the time, it’s a robust conviction loosely held.

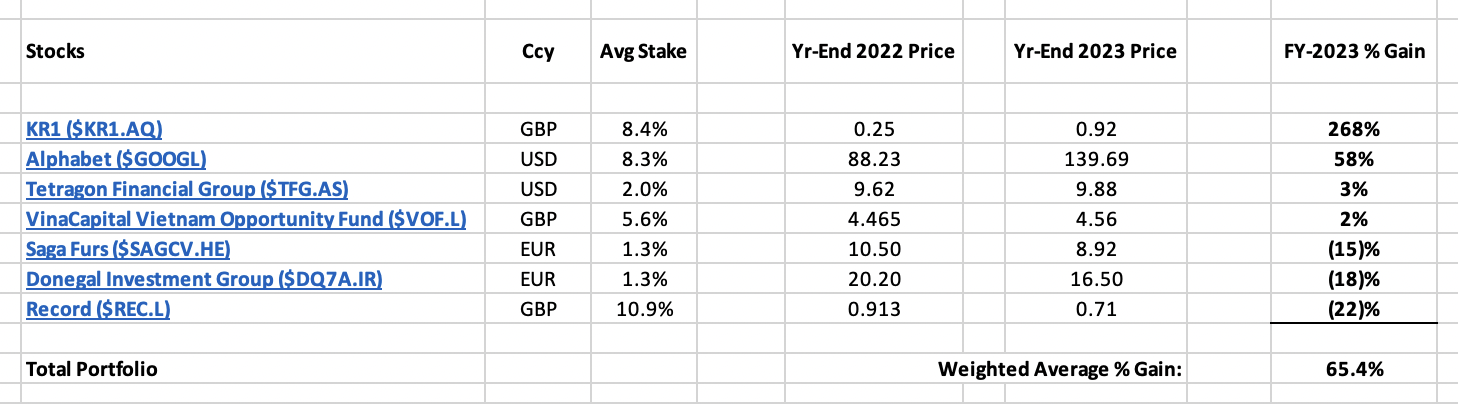

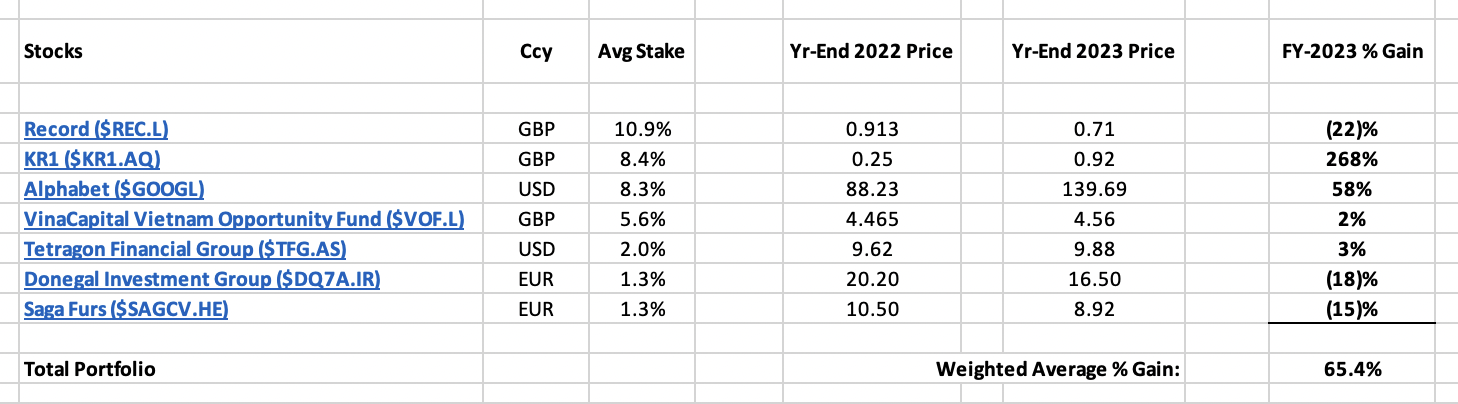

So let’s transfer on – right here’s my very own Wexboy FY-2023 Portfolio Efficiency, by way of particular person winners & losers:

[Gains based on average stake size (NB: NO actual changes in holdings, except for an imperceptible increase in TFG due to its DRIP) & end-2023 vs. end-2022 share prices. All dividends & FX gains/losses are excluded.]

And ranked by dimension of particular person portfolio holdings:

And once more, merging the 2 collectively – by way of particular person portfolio return:

I’m delighted to report a improbable general +65.4% acquire for my (disclosed) portfolio in 2023…it’s been fairly the (roller-coaster) journey!

In fact, I need to instantly minimize off the standard reply/whatabout-guys, who’ll need to particularly exclude my KR1 positive factors right here as some type of fortunate once-off (however clearly KR1 needs to be included within the dangerous years!), and focus as a substitute on my 2022 losses & do their ordinary gotcha try at some fancy yoy/cumulative return math. However so what…yearly, I proceed to watch & tweet about my portfolio, and do the identical complete year-end assessment as I all the time do, no matter whether or not it was a superb or dangerous 12 months. And in so doing, I’ve now constructed up – and shared with any investor on the market – a 12+ 12 months public/real-time/auditable funding portfolio & monitor document, most likely one of many solely such (free) blogs left on the planet. I nonetheless await the reply-guy who’s accomplished something remotely like that!?

And as Bessembinder reminded us, that is the fact of most profitable long-term monitor data & the general market itself…most of your positive factors will truly come from a small minority of shares, or perhaps a single inventory/two. That is one thing to (hopefully) be embraced – as I’ve stated, the problem isn’t discovering potential multi-bagger shares, the actual problem is determining methods to truly dangle on to them! [Which is frankly all about EQ, not IQ]. And that’s how I’ve held on to an enormous multi-bagger like KR1, and another disclosed (& undisclosed) multi-baggers in my portfolio…by specializing in the standard & trajectory of the enterprise itself, reasonably than its inventory value, and having the conviction & the abdomen to anticipate & truly endure some horrible & inevitable draw back volatility alongside the best way.

And that’s it, I feel my contribution at this level is usually the zen apply of doing virtually nothing…and I hope 2023 is an ideal instance, as most buyers would possibly intuitively presume a +65.4% annual acquire would require frenetic buying and selling & aggressive macro/sector calls, however in actuality I did NO buys/sells in my disclosed portfolio, and valuable little in the remainder of my portfolio both. The (in-) frequency of my weblog posts additionally now displays this, plus the very fact I diversify extra & purchase/common into extra/smaller positions (a venture-capital method) if I feel they provide substantial upside potential (a small holding’s all you want, if it seems to be a multi-bagger!). And I not watch any monetary media (or speak to brokers, except I’ve a selected request), as I can clearly collect all of the information/knowledge I would like on-line (on my phrases), I can tweet/work together in a managed method on Twitter, and I’m nonetheless all the time delighted to interact IRL as a substitute with administration & different buyers, fund managers & household places of work.

In fact, the proof is within the pudding, as is the conviction to do much less & truly resign your self to important drawdowns within the perception superior long-term returns are the last word prize…and it’s all tracked right here intimately on the weblog, my three 12 months portfolio return (once more, excluding dividends) is now a +113% acquire, whereas my 5 12 months return is a +284% acquire.

With that, let’s transfer on to my portfolio:

FY-2023 (15)% Loss. 12 months-Finish 0.8% Portfolio Holding.

One other powerful 12 months…not less than for Saga Furs’ share value. The enterprise itself did nice, chalking up its second-best leads to the final 5 years. Not that buyers truly seen final 12 months, regardless of the corporate’s periodic public sale experiences – a reminder how irritating micro-cap worth investing may be! It took a constructive revenue warning early this month to lastly heat up sentiment…with FY outcomes now launched, the inventory’s up +20% YTD, greater than reversing final 12 months’s decline.

FY-23 public sale gross sales got here in at €352 million, turnover at €47M & EPS at €1.39/share, with a proposed €0.66/share dividend due within the subsequent few months. At €10.70/share, this leaves Saga buying and selling on a 7.7 P/E & a potential 6.2% yield. As all the time although, absolutely the EPS doesn’t essentially matter, it’s the a number of buyers are prepared to use…which stays low, so long as buyers see no clear income/earnings trajectory right here. On the one hand, Saga’s on an inexpensive 6 P/E versus a median €1.77 EPS during the last three years – however on the opposite, it’s on an costly 19.5 P/E vs. a median €0.55 EPS during the last 5 years. [Albeit, mitigated by a 0.4 P/B, vs. €25+ equity/share, which I believe is fully realizable]. Clearly, opinion stays divided right here…

And in the meantime, the extra apparent upside potential would come from a sale (say, to a PE/Asian purchaser). Or a wind-down of the corporate, albeit there’s little signal of that…regardless of all of the headlines, shoppers have NOT rejected fur, and Saga truly offered 13 million pelts final 12 months & a median 10M pelts pa during the last 5 years. But when it may string two good years collectively, which may show an actual inflection level. Traders can hope that Denmark’s nationwide mink cull & Chinese language farm capability reductions throughout COVID proceed to assist pelt costs (except China ramps again up). And if/when rival public sale home Kopenhagen Fur is lastly wound up – this was introduced in late 2020, however auctions are nonetheless scheduled for 2024 – that might additionally add apparent scale & momentum to Saga Furs, as an efficient world fur public sale monopoly.

ii) Donegal Funding Group ($DQ7A.IR)

FY-2023 (18)% Loss. 12 months-Finish 0.8% Portfolio Holding.

A 12 months of inactivity at Donegal Funding Group, with no contemporary information re its final remaining seed potato division…therefore, the regular share value decline, principally from boredom (reasonably than precise promoting, with valuable little buying and selling quantity). Turnover did hit €30 million, the very best (by a small margin) in 5 years, but it surely’s the type of enterprise that will get offered primarily based on common turnover & margins, plus the worth of the R&D pipeline – so it’s all about discovering the correct purchaser, sooner reasonably than later. But it surely’s two+ years now since administration offered its penultimate Nomadic Dairy division, so this delay in a remaining sale/liquidation is clearly irritating.

Alternatively, it’s been a improbable long-term funding, and any deal delay is arguably mitigated by continued seed potato profitability. And this limbo hurts bigger shareholders extra: De facto CEO Ian Eire, Chairman Geoffrey Vance & the remainder of the board personal an combination 6.4% stake (value a a number of of their ongoing compensation), whereas Nick Furlong/Pageant Investments personal a a lot bigger 12.6% stake & clearly haven’t shied away from taking a extra aggressive activist position prior to now when required.

Donegal money is now at €6.9 million, reflecting a remaining €3.3M contingent consideration for Nomadic Dairy, whereas sundry property & investments, seed potato earnings & some additional normalization of receivables ought to add one other €1-2M+ internet. Versus right this moment’s €25M market cap, that’s a sub-€17M/0.6 P/S valuation for the seed potato division. Which is affordable…sure, working revenue was held again this 12 months (to a 6% margin), however the division enjoys 7-10% working margins in good years. And this consists of full absorption of remaining HQ/itemizing/board expense, so the division’s underlying margin is way increased once more, to not point out its pipeline of R&D spending/new varieties. All instructed, this could suggest a considerably increased valuation within the fingers of the correct acquirer – arguably, someplace between a 1.0 & 2.0 P/S a number of, making an allowance for Nomadic’s 1.8x sale a number of (for related causes). This gives engaging/event-driven upside potential for buyers…and in the meantime, we apparently have a brand new flooring at €16.50/share, with administration just lately resuming (small up to now) open market share buybacks.

iii) Tetragon Monetary Group ($TFG.AS)

FY-2023 +2.7% Achieve. 12 months-Finish 1.6% Portfolio Holding.

We’re additionally caught in a holding sample with Tetragon – albeit, my precise return final 12 months (together with a 4.4% dividend yield) was an inexpensive +7.3%, i.e. not far off TFG’s longer-term internet +9-10% pa complete returns. YTD NAV/share return (to end-Nov) has been weak at +1.8%, however let’s await the subsequent factsheet (due Jan-31) which often sees a pleasant bump (a median +8.7% acquire within the final three years) from the TFG Asset Administration year-end valuation course of & crystallization of underlying incentive charges. Administration’s maintained a $0.11 quarterly dividend & periodic tender gives (totaling $60 million final 12 months), and have returned $1.6 billion+ to shareholders for the reason that 2007 IPO. This seems far much less spectacular although, if you notice final 12 months’s $0.1B complete payout comes from a $2.8B steadiness sheet.

Alternatively, Tetragon’s advanced right into a extra compelling proposition – TFG Asset Administration is a portfolio of 100%/majority-owned different asset managers (now at $42 billion AUM & persevering with to take pleasure in a secular fund-raising tailwind), which now quantities to almost 50% of complete NAV. In reality, TFGAM’s now value 160% of TFG’s present market cap (with a $1.5B funding portfolio thrown in at no cost!). As for its legacy governance/payment construction, it hasn’t stopped TFG producing internet +9-10% pa NAV/share returns & I see no cause this will’t proceed…so if the 66% NAV low cost doesn’t shut, buyers can nonetheless hope to make the identical returns, whereas if it does begin closing (or will get eradicated) then shareholder IRRs doubtlessly go exponential. Alas, prior/disgruntled shareholders can by no means appear to know this math…to the good thing about new buyers.

The true downside right here is administration: Principals & workers personal a 38% stake, however Reade Griffith is (by far) the dominant stakeholder, and he & Paddy Pricey nonetheless personal TFG’s exterior administration contract. As with many owner-operators, the share value & valuation are fairly irrelevant ‘til they lastly need to exit…in the meantime, they’re extremely compensated to take care of/develop complete NAV, with NO signal of an IPO or sale. Which seems to replicate them desirous to retain their exterior administration contract, and/or keep on to handle the AUM, which doesn’t fly in an IPO/sale…so administration’s actually the poison-pill right here. This combo. of management & greed additionally leaves us with an alternate asset supervisor stapled to a $1.5B funding portfolio – it’s neither fish nor fowl & buyers don’t need/worth that mixture extremely (in response, listed asset managers have typically diminished their degree of invested capital vs. AUM).

In reality, buyers could not even need a portfolio of other asset managers (& I’d disagree strongly with this), judging by Tetragon’s closest peer – Goldman-backed Petershill Companions ($PHLL.L) which additionally trades on a large 46% NAV low cost. Consequently, a piecemeal sale of TFG’s asset administration companies & portfolio now appears the most effective path to realizing worth, although God is aware of when this would possibly occur. However administration’s left an enormous amount of cash on the desk right here…and is lacking out on an unimaginable alternative to reinforce worth, as I imagine TFG may simply increase $0.5 billion+ of liquidity in a month/two to fund a young provide. Even at a premium, TFG may purchase its personal enterprise/portfolio at 40 cts on the greenback – no different investments, new or previous, remotely match that pay-off (no matter what Paddy Pricey claims on each investor name!).

However I’ve to confess, Tetragon’s portfolio is heating up…its 75% stake in infrastructure PE supervisor Equitix alone accounts for 87% of its present market cap, and it now seems like a compelling goal (on an inexpensive valuation) within the wake of Blackstone’s International Infrastructure Companions deal & Normal Atlantic’s acquisition of Actis in the previous couple of weeks. Ripple most popular inventory accounts for an additional 10% of TFG’s market cap…this has already been marked up 50%+ YTD in 2023 & may add some pixie-dust if this crypto rally goes exponential. In abstract, nothing’s modified with TFG’s administration & low cost, however Equitix & Ripple could (lastly) persuade me to contemplate including to my present holding…

iv) VinaCapital Vietnam Alternative Fund ($VOF.L)

FY-2023 +2.1% Achieve. 12 months-Finish 4.6% Portfolio Holding.

It was a fairly regular 12 months for the Vietnamese market…which is uncommon, as it may well flat-line for months & even years at a time & then explode increased (or decrease!). [Same is true of VOF]. The VNI was up +12% final 12 months – one of many best-performing markets in SE Asia – albeit, mitigated by a near-(3)% weakening within the dong (vs. the greenback). VinaCapital Vietnam Alternative Fund once more outperformed with a +17% complete return (in greenback phrases), aided by its share buyback programme (which retired 3.25% of o/s shares final 12 months). Sadly, VOF itself solely noticed a +2.1% enhance…inc. dividends, my complete return was simply +4.5%. Nevertheless, this shortfall can principally be attributed to ‘noise’, which tends to clean out over time, i.e. a 5%+ strengthening of the pound (vs. the greenback, word VOF’s priced/trades in sterling), and a 3% widening within the fund’s NAV low cost (~18% as of year-end).

Large image although, nothing’s modified: Vietnam’s a beautiful economic system/market to spend money on, with a younger/educated workforce that’s nonetheless low-cost versus the remainder of the world (& extra importantly, vs. China), however is greater than able to transferring up the value-add export curve. And the #NewChina funding thesis is as compelling as ever – Vietnam nonetheless enjoys an accelerated progress trajectory, it’s a main marketplace for Chinese language outsourcing, and it has a robust & rising commerce relationship with the US. It additionally presents little of the political threat buyers face with China…in actual fact, continued US-China tensions could add a major tailwind, with US re-allocation of sourcing to Vietnam & the back-channeling of Chinese language manufacturing/exports by way of Vietnam.

Subsequently, with rising markets funding typically uncared for & turning into extra problematic (with China being a dominant element of the MSCI index), I proceed to cherry-pick Vietnam as a best-in-class market…one that gives 6%+ GDP progress, common 3.3% inflation (final 12 months), anticipated +10-15% earnings progress in 2024 (& a 0.70 PEG ratio), and a 30% public fairness valuation low cost vs. regional friends. [Here’s VinaCapital’s 2024 Vietnam Outlook]. I additionally contemplate VinaCapital to have the most effective long-term monitor document, whereas the multi-asset nature of the fund (public fairness, non-public funding in public fairness, OTC/pre-IPO shares & actual property) is important for what continues to be a frontier market. A 19% NAV low cost right this moment, some activist grumbling & the funding supervisor’s $23 million/2.6% stake in VOF are all persuasive too. Technically & essentially, I’m firmly satisfied there’s a 100%-150%+ rally forward of us right here within the subsequent few years…the VNI breaking free & away from 1,200 would sign a decisive inflection level.

FY-2023 (22)% Loss. 12 months-Finish 6.7% Portfolio Holding.

Document was my most disappointing loss in 2023 – although luckily, a monster 7.4% dividend yield diminished my complete return to a (16.5)% loss – with the market reacting negatively to a transition 12 months, amidst a extremely spectacular medium-term progress trajectory. This kicked off with a Capital Markets Train-In, the place the subsequent era of administration was launched. Founding Chairman Neil Document then introduced his retirement (Jul-2023), adopted by CEO Leslie Hill (end-March 2024) & then CFO Steve Cullen (Summer season-2024). [To be replaced by Richard Heading – currently, Group Finance Director at £2.7 billion IG Group – who should bring valuable investor relations experience, and can hopefully attract a new institutional shareholder/two]. It will come as no shock to present shareholders, although the timing could have been accelerated in what’s proved a 12 months of consolidation, after earnings greater than doubled within the final two FYs.

This consolidation grew to become extra obvious in mid-2023, with a troublesome comp vs. a surge in FY-2023 efficiency charges (to £5.8M), and was mirrored accordingly within the share value. Subsequently, this was acknowledged by administration after disappointing interims, citing a decrease degree of efficiency charges & delays in regulatory approval (of its continued diversification into new fund merchandise/launches). [NB: Performance fees (from active duration hedging) are actually more consistent now, but even in a blockbuster FY-23 they still only amounted to 13% of total revenue]. Once more, this may occasionally have accelerated Hill’s retirement choice – the logic being the brand new CEO Jan Witte & group have to ‘personal’ the medium-term targets she set after turning into CEO. However as I beforehand careworn, the one goal that slipped is FY-25 timing – bear in mind, REC’s FY-25 begins this April – Document stays assured of its £60M income/40% working margin targets. And given the doubling in EPS to five.81p/share within the final two FYs, and an implied EPS goal of ~10p/share, I see no wavering in conviction of longer-term targeted shareholders (like me) if supply’s doubtlessly delayed by a 12 months/two right here.

However on Friday, we acquired Document’s Q3 buying and selling replace…and it was a monster! AUME was up +18%/$15 billion within the quarter to a brand new $99.5B document excessive, pushed by $7.9B of internet inflows, whereas efficiency charges have been at £3.5 million (that’s £5.0M YTD, simply shy of final 12 months’s £5.8M). That places common AUME YTD at $89.5B, which can enhance to $91.5B by end-This fall (all else being equal), up +10% versus $83.1B final 12 months…however since Document’s a UK enterprise, so we have to deal with common sterling AUME which is homing in on £72.8B, up +6.5% vs. £68.4B final 12 months (sterling’s stronger yoy). The consensus EPS drop this 12 months (to sub-5.2p/share) now seems wildly off & matching final 12 months’s 5.81p EPS is unquestionably again on the playing cards. And this Q3 momentum – which seems prefer it’s continued into This fall, together with an anticipated new infrastructure fund launch (& ideally a brand new crypto fund launch with Dair Capital) – is persuasive proof Document’s income & working revenue targets are literally inside attain. I depart it to the brand new CEO to set a brand new/revised goal date, if he needs.

In the meantime, REC trades on a 12.3 P/E & an ex-cash 10.5 P/E. Which seems fairly rattling low-cost vs. its current/potential earnings trajectory – bear in mind, during the last 3-5 years, Document’s AUME/internet inflows, income/earnings & share value have all massively outperformed, in opposition to the back-drop of a vicious & unrelenting bear market within the UK-listed asset administration sector. And it’ll proceed to be an owner-operator enterprise, with the brand new administration group recruited internally/already steeped within the tradition, whereas Leslie Hill & Neil Document will nonetheless personal (& monitor) an combination 37%+ stake regardless of their respective retirements…albeit, this does increase the distinct risk of an final sale, or takeover method!?

FY-2023 +58% Achieve. 12 months-Finish 9.9% Portfolio Holding.

Wow, what a spectacular annual acquire for a mega-cap like Alphabet! An apparent key driver was the inevitable restoration from a price-drives-narrative 2022 bear market (within the wake of a decrease high quality/tech inventory bear market since early-2021), an amazing reminder to focus much less on value & extra on an organization’s basic KPIs & trajectory when you ever hope to HODL it longer-term. And an important warning to disregard the extra grandiloquent #FinTwit accounts, who insisted Alphabet was a brief & even a zero after ChatGPT’s Nov-2022 launch!? In actuality, and I feel many misremember this now, $GOOGL truly bottomed (at sub-$85/share) virtually a month BEFORE ChatGPT was launched (as did $META), and rose slowly however steadily within the following months, earlier than accelerating increased in Mar & Jun-2023. Even the notorious $100 billion+ dump in early-Feb, when Bard was demoed & it made a small factual flub (reasonably quaint, contemplating the hallucinations ChatGPT/LLMs are able to!), is now barely discernible on the value chart.

However the extra basic drivers of Alphabet’s positive factors final 12 months have been two-fold: Firstly, after a 2022 slowdown within the wake of a spectacular COVID-driven +75% acquire in revenues (vs. 2019), plus a restructuring of the corporate’s expense/worker bloat, Alphabet started to steadily speed up once more from a Q1 +3%/+6% cc income acquire to a +13% income acquire in This fall. Second, it slowly grew to become obvious to the typical investor that Alphabet was NOT caught out/quick re AI…which was apparent to longer-term shareholders, who have been already very conversant in the identical cautious/incremental method to autonomous driving at Waymo. As Yann LeCun famous on the time: ‘If Google (& Meta) haven’t launched ChatGPT-like issues, it’s not as a result of they’ll’t, it’s as a result of they gained’t!’. However all credit score to Sundar Pichai – recognizing the investor disconnect, he cracked the whip & opened the floodgates, kicking off a string of merchandise/occasions: Bard, PaLM, a merger of Google Mind & DeepMind, SGE, Assistant with Bard, Duet AI, Google Lens, Vertex AI, Gemini, and so on. This makes Alphabet the plain (software program) AI play for me – versus Nvidia, a {hardware} AI play – constructing on the foundations of Google Search (plus DeepMind), which I nonetheless contemplate was & is the most effective/most beneficial AI on the planet. And now it’s turning into clear LLMs are comparatively open-source & require enormous funding & cloud/power sources to essentially scale up, it’s Alphabet’s user-base that may & will cement its dominance…ie the actual worth lies within the software & exploitation of AI in customers’ day by day lives & corporations’ day by day operations, for which Alphabet is ideally suited with 15 merchandise that have already got 500 million+ customers, and 6 of these now boasting 2 billion+ customers!

In fact, there’s huge worth to be tapped elsewhere in Alphabet’s portfolio – Waymo’s opening extra cities up for autonomous (taxi) autos, Ruth Porat will quickly transfer from her CFO position to CIO of its Different Bets, and YouTube continues to be in Beast mode! In reality, it more and more seems to be a two-horse race between YouTube & Netflix now – it has a brand new CEO Neal Mohan, it’s efficiently bridged between streaming & a (much less controversial) type of social media, its Shorts rollout has been spectacular (70 billion day by day views, 2B+ signed-in customers every month), it’s far larger than Netflix (YouTube complete revenues hit near $40B a 12 months in the past, together with $11B of subscription revenues which already quantity to a 3rd of Netflix’s revenues) & a greater enterprise mannequin too (i.e. UGC, with a primarily contingent expense base). In fact, YouTube (& different divisions/investments) may doubtlessly obtain a lot increased multiples spun-out, and Porat will map out a master-plan for that, however proper now that’s a tailwind administration can nonetheless comfortably wait to launch/depend on sooner or later.

In the meantime, $GOOGL is setting new all-time highs, however nonetheless trades on a 23 P/E. [I’m ignoring the Q4 after-hours (5.8)% decline right now, as its seems like an over-reaction to an overall beat & minor ad revenue miss]. And once I think about its steadiness sheet money/investments, the capitalization of Different Bets losses (in expectation of future/a lot bigger payoffs), and its persevering with funding within the core Google Search/YouTube companies & Google DeepMind, Google Cloud, Waymo, and so on., its underlying core a number of seems a lot the identical to me right this moment because it did in my authentic writeup. Taking that & its relentless compounding of income/earnings into consideration, plus the potential for additional (AI-driven) revaluation, I stay extremely assured in Alphabet as a High 2 portfolio holding…and I eagerly await $200/share as a brand new goal/milestone to re-evaluate its continued basic trajectory & new upside potential goal(s).

FY-2023 +268% Achieve. 12 months-Finish 23.8% Portfolio Holding.

Sure, the crypto-winter’s properly & actually over…and it was a improbable 12 months for KR1 shareholders! Per my estimate, KR1’s NAV was up +179% to finish the 12 months at 110p/share, with the share value out-performing as its (absurd) NAV low cost steadily narrowed from a 20-40% vary to a 0-20% vary. [Alas, it’s wider again this year, with negative sentiment unfairly spilling over from the most recent crypto-miner collapse]. Not that you just’d comprehend it from the group, who caught to their knitting & prevented the media/investor relations highlight, focusing as a substitute on making 9 new seed & follow-on investments, at a price of $4 million. [Including two new DAO/early-stage VC fund investments, which helps spread their seed investment access/potential even wider]. KR1 now boasts 100+ investments during the last 7.5 years…clearly a uniquely diversified portfolio, versus the standard listed crypto inventory/fund. In the course of the 12 months, KR1 additionally ticked off two extra investor relations/company governance targets: i) It prolonged the government providers settlement to late-2030 – a crucial/invaluable ‘lock-up’ of the core KR1 group for the unique good thing about shareholders, and ii) it lastly beginning publishing a month-to-month RNS (one month in arrears), detailing a exact NAV/share, its month-to-month staking earnings & its present High 10 portfolio holdings – e.g. right here’s the Nov NAV RNS, it’s a easy snapshot that additionally permits extra engaged shareholders to rapidly/simply monitor the NAV & portfolio on a real-time foundation.

The massive pleasure for the group got here end-Oct with Celestia‘s mainnet launch. [In fact, they’d highlighted Celestia in two separate paragraphs in the interims…which is actually them jumping & down with excitement, as long-term shareholders will know!] An authentic $75K seed funding in Unusual Loop Labs – the authorized entity behind Celestia – granted them 7.5 million TIA tokens, initially value $17M & now value $137 million simply three months later. That’s an astonishing 1,800-bagger+ return in lower than three years, amongst many different mega-multibaggers the group has scored up to now. [Note these are locked up ‘til the first/second anniversary of mainnet…on the other hand, as Celestia becomes more valuable, we may also speculate how much additional value potentially still resides in KR1’s equity stake?!] To not point out, the group may stake TIA instantly (at a 21%+ APR, now 16%+), so we noticed an enormous step-up in month-to-month staking earnings from £395K in Oct to £939K in Nov, and this earnings might be increased once more in Dec & Jan because the $TIA value has continued to climb.

In reality, we’re now a $28 million+ pa staking earnings run-rate. [And no, this isn’t some once-off bonanza – over the last three years, KR1 actually earned an average £16.5M pa in staking/parachain income!] And KR1 enjoys a 98% internet margin on this earnings…and I imply precise internet margin, not some absurd ‘adjusted’ margin crypto-miners cite to idiot buyers. I name it the ZERO funding thesis…since KR1 eschewed Bitcoin & proof-of-work from day one, focusing as a substitute on proof-of-stake, it now boasts zero {hardware}, zero power use, zero debt, zero dilution & zero capital required (to not point out a zero Isle of Man tax charge). Subsequently, that 98% internet margin is precise internet revenue, with no incremental G&A, {hardware}/power prices, curiosity, or taxes. [NB: This income may incur a 20% performance bonus, since NAV surpassed its prior high-water-mark earlier this month, but only if it’s crystallized at end-2024 (dependent on the overall portfolio)].

In fact, the long-standing grievance right here is the silence/lack of apparent progress re an up-listing to the LSE/AIM, plus the continued absence of a constant skilled investor relations operate. Alas, a standard grievance with owner-operators – the group personal 25%+ of KR1 (& don’t require contemporary capital), so the share value/valuation is fairly irrelevant ‘til they lastly search an exit, plus they have a tendency to imagine they need to ‘deal with the enterprise & the share value will handle itself’. Which is completely true: As a result of as of year-end, KR1’s NAV/share & share value have BOTH compounded at a unprecedented +98% pa since Jul-2016 (that’s +16,327% vs. +16,040% up to now!), so clearly its Aquis itemizing has proved NO obstacle, and as soon as once more we’re reminded (per Charlie Munger!) {that a} compounder’s share value return will inevitably converge with its precise return on capital.

That being stated, there’s LOTS of cash being left on the desk right here – e.g. $RIOT, $MARA & $BRPHF commerce on a a lot increased common 2.6 P/B, regardless of mediocre long-term shareholder returns – and the KR1 group harm themselves probably the most (arguably leaving $70 million+ on the desk personally!). The IR operate may be simply solved with a group rent, on an inexpensive wage & variable bonus tied to share value/valuation – that’s the quid professional quo shareholders typically anticipate from a $0.2 billion firm, and in return for group bonuses up to now & right this moment’s compensation construction. As for an up-listing, noting its unimaginable success on Aquis, possibly the London Inventory Alternate needs to be advertising and marketing KR1 re a (twin) itemizing at this level?! And noting the SEC’s lastly authorized US Bitcoin ETFS, plus the UK PM/authorities’s pro-crypto stance, we want a extra constructive & proactive stance from the FCA too. Clearly, KR1’s been extremely profitable up to now, it deserves to be championed as an investor in UK (& European) crypto start-ups, and a far bigger pool of buyers ought to have fast & quick access to purchase its shares.

As all the time, I like to recommend any investor ought to now contemplate a 3-5% crypto allocation of their portfolio, ideally by way of KR1’s distinctive diversified portfolio & monitor document…specifically, UK buyers who’ve NO different viable UK peer shares to contemplate investing in (& they’ll’t purchase the brand new US Bitcoin ETFs both). So once more, I urge all shareholders to contact/be in contact with the group to push for an up-listing & knowledgeable IR operate. In the meantime, KR1 trades on a 0.63 P/B & a 6.6 P/E, and I imagine it may well & will proceed to compound worth for shareholders & ought to commerce on a a number of of its present valuation…particularly now, when AI is digital abundance, crypto is digital shortage, and the world wants each.