{kind=link}

Copper is the invisible spine of the fashionable world. It’s required in each single wire, transformer, digital gadget, battery, EV, windmill, photo voltaic panel, motor, air conditioner, and rather more.

On high of this pre-existing demand, the inexperienced transition is boosting copper demand drastically. A standard automobile makes use of 23kg of copper, whereas an EV wants round 100kg[1]. The identical holds true for renewable energy, batteries, and the brand new electrical transmission required for the electrification of all the things.

This interprets into the demand for copper doubling by 2035.

it will likely be extraordinarily troublesome to ship that scale of provide over the timeframe. (…) With all this, there may be nonetheless not sufficient copper, even within the Excessive Ambition Situation. Underneath this state of affairs, the utmost annual shortfall can be within the mid-2030s, at 1.6 MMt in 2035. Then the pressures ease due to the rise in recycling and the slowing of development, significantly in power transition demand.

S&P World: The Way forward for Copper

So betting on copper is a wager on financial development, the inexperienced transition, and a extra environment friendly trendy world.

Greatest Copper Shares

As a central a part of each electrical system, copper is rarely going to get replaced by one other metallic any time quickly.

So let’s take a look at one of the best copper shares.

These are designed as introductions, and if one thing catches your eye, it would be best to do further analysis!

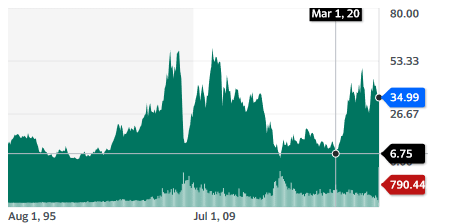

1. Freeport-McMoRan Inc. (FCX)

| Market Cap | $51.9B |

| P/E | 19.12 |

| Dividend Yield | 1.71% |

Freeport was created in a 1988 IPO after the invention of the Grasberg gold & copper deposit in Indonesia, nonetheless its most essential asset to this present day. The corporate additionally has a number of mines within the Americas (USA, Peru, Chile) and 25+ years’ value of copper reserves.

In 2022, FCX produced 4.2 Blbs of copper and 1.8 Moz of gold. The corporate ought to be capable of keep this degree of manufacturing no less than till 2025.

Freeport has a coverage to pay again 50% of free money stream to shareholders with buybacks and dividends. The corporate has a complete of $10.6B in debt, and $8.1B in money, with debt maturity after 2028.

The multi-decade reserves (44% within the US) and really manageable debt make Freeport a very good copper inventory for prudent traders. Its diversified places additionally cut back geopolitical danger.

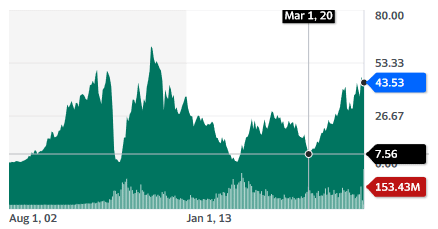

2. Teck Assets Restricted (TECK)

| Market Cap | $23.3B |

| P/E | 8.23 |

| Dividend Yield | 0.84% |

Teck is a big mining firm centered on steelmaking coal and base metals, principally zinc and copper. Teck has been engaged on splitting the corporate into two elements so the “inexperienced” copper phase is not going to be laden by the “ESG-unfriendly” coal phase.

Issues bought difficult when mega-miner Glencore tried a takeover to later spin off its personal coal enterprise along with Teck’s. This led to the splitting plans being withdrawn. One other separation plan continues to be within the making.

These distractions don’t change the truth that Teck is planning to double its copper output (At present 600k tons per yr) by 2027-2029 after which double it once more in the long run.

Teck is for traders prepared to abdomen the short-term confusion about splitting coal and copper operations and searching for sturdy manufacturing development.

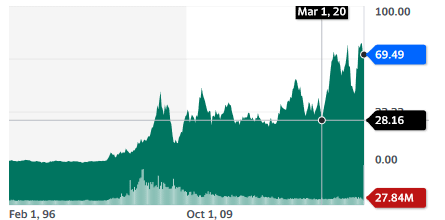

3. Southern Copper Company (SCCO)

| Market Cap | $57.6B |

| P/E | 20.20 |

| Dividend Yield | 5.76% |

The corporate operates in Peru and Mexico, with 11% of the shares in free float and 89% owned by GrupoMexico Mineria.

The corporate has among the many lowest manufacturing prices within the copper trade, together with Glencore and Freeport.

It expects to provide 939kt of copper in 2023 and has 44.8 million tons in reserves, the very best copper reserve of any listed firm. 77% of the corporate’s revenues are from copper, with the remainder from molybdenum (10%) and some different base metals.

Southern Copper plans to extend manufacturing by 210 kt of copper by 2026 and to 545 kt by 2032.

The corporate has been strengthening its steadiness sheet, with money & equal now at $5.1B for a complete debt of $6.2B.

This can be a pure play in copper with excellent reserves. This makes the inventory fascinating for traders searching for as a lot copper publicity as potential, produced for so long as potential. The jurisdiction dangers are nonetheless actual, compensating for the very low geological danger.

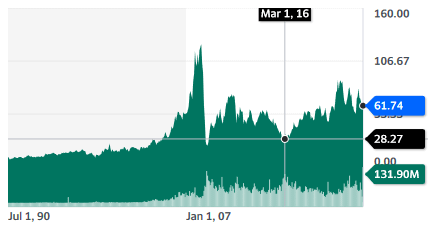

4. Rio Tinto Group (RIO)

| Market Cap | $102B |

| P/E | 8.05 |

| Dividend Yield | 8.02% |

The mining large is, for now, principally getting revenues from its iron mines in Australia. It’s nonetheless energetic in copper and trying to develop its presence on this market. Rio Tinto has additionally not too long ago entered the lithium market with the Ricon Mission in Argentina. It’s also producing diamonds and inexperienced aluminum with hydropower power.

Essential to those plans is the copper-gold Oyu Tolgoi mine in Mongolia. It’s being expanded to double the present manufacturing and needs to be the 4th largest copper mine on the earth by 2030, within the first quartile of the associated fee curve.

The corporate can also be “beneath immense stress to develop a US copper undertaking” value 1/4 of the USA’s whole copper reserves.

Rio Tinto additionally owns Nuton, a know-how firm that developed a technique to extract extra copper from ore than earlier than. It may free as much as 100 million tons of copper at present trapped in residual tailings. This know-how can notably be leveraged to signal offers to accumulate a small portion of different copper mines, like not too long ago with McEwen, Arizona Sonoran Copper Firm, or Regulus.

The corporate has a historical past of sustaining a steady dividend of 40-60% of the underlying earnings.

Rio Tinto is an organization for traders searching for basic publicity to mining and strong dividend yield, with a robust upside and development in inexperienced transition metals.

5. McEwen Mining Inc. (MUX)

| Market Cap | $385.5M |

| P/E | – N/A |

| Dividend Yield | – N/A |

McEwen Mining is a mining firm growing treasured metallic and copper property.

The corporate at present operates three gold & silver mines, with the manufacturing of 150k-170k gold equal ounces (GOE) anticipated in 2023. It not too long ago raised $82M, which might be sufficient to carry the Fenix undertaking in Mexico into manufacturing at a 26k GOE.

The long run flagship of the corporate is the McEwen Copper subdivision, with the Los Azules Argentinian mine undertaking anticipated to be the ninth largest on the earth, with 36 years of mine life.

McEwen Copper has not too long ago obtained funding from Rio Tinto’s tech firm Nuton and automobile producer Stellantis (16 manufacturers: Peugeot, Fiat, Chrysler, Citroen, Opel, Maserati, and many others.). It’s also owned at 13.8% by its founder Rob McEwen, the founding father of Goldcorp, who grew the corporate from $50M to $8B.

The latest capital elevate from Nuton and Stellantis for Los Azules put the undertaking worth at $550M, greater than McEwen Mining’s market cap of $366.6 million. Collectively, Nuton and Stellantis have invested a complete of $210M in Los Azules.

Traders will wish to regulate the potential dilution of McEwen mining possession in McEwen Copper, as the corporate is prone to have lower than $50-100M of free money stream accessible yearly to finance the $2.4B wanted capex to develop Los Azules. After all, debt and proportional funding by Stellantis and Nuton may present further funding as nicely.

Nonetheless, Los Azules is a really precious asset, and the latest valuation signifies a possible undervaluation of McEwen. Traders prepared to attend and to wager on copper worth in a 5-10 years horizon might be most on this massive undeveloped deposit.

6. Ivanhoe Mines Ltd. (IVN.TO)

| Market Cap | CAD14.2B |

| P/E | 24.11 |

| Dividend Yield | – N/A |

Ivanhoe is a number one mining firm producing zinc, copper, and treasured metals. It operates in South Africa and the Democratic Republic of Congo (DRC).

Ivanhoe produced 333kt of copper in 2022 and plans to ramp up manufacturing to 11.4 Mtpa by 2026 and a most of 19 Mtpa from 2030 to 2054. The corporate represents roughly 4% of the full GDP of the DRC.

The jurisdictions the place Ivanhoe Mines operates are removed from superb, between a troubled South Africa and a really underdeveloped Congo. What’s going to drive traders to this inventory is the promise of terribly massive reserves and a possible doubling of manufacturing within the 2020s. The inventory has gone up virtually 5x since its 2020 lows, so a few of this development may be already priced in.

Greatest Copper ETF

Within the mining sector uncovered to jurisdictions and geopolitical danger, diversification could be crucial. So that you may be enthusiastic about ETFs concentrating on the sector as an entire.

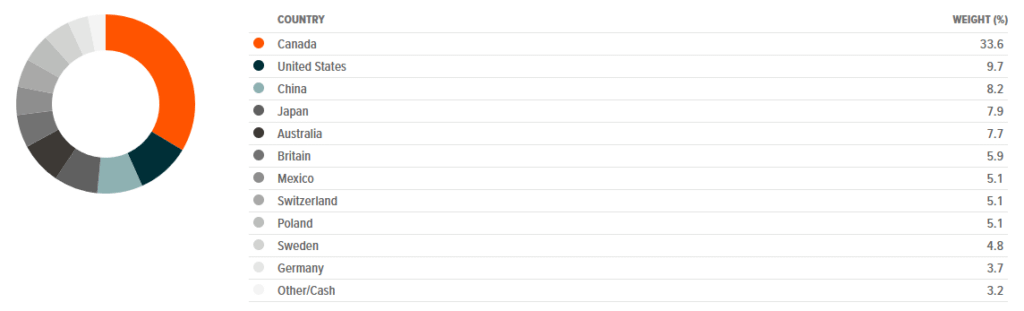

World X Copper Miners ETF (COPX)

This ETF invests solely in mining corporations energetic in copper. It’d nonetheless give some degree of publicity to different metals, with its high 5 holdings together with Lundin Mining, Teck, and BHP.

Whereas Canada and the USA seem as high holdings (see under), traders will wish to examine the place the mines are literally positioned, even these with a list or headquarters in North America.

Greatest Copper ETNs

COPX is the one completely copper-focused ETF, with different mining ETFs probably together with copper however with publicity to different base metals and/or treasured metals. One other solution to wager on copper is to purchase the commodity itself by means of two accessible ETNs (Change Traded Notes):

Conclusion

Copper is an important element of the inexperienced transition and trendy know-how, and we’re prone to barely have sufficient of it if inexperienced objectives are even to be partially reached. Copper miners are prone to do nicely, even when the sector is thought for its excessive volatility and sensibility to recessions.

There’s a sturdy argument for publicity to this key commodity, however traders will wish to take note of valuation, manufacturing prices, and jurisdiction/geopolitical danger.