With this post, we crossed the “half-time” mark for the Belgian Stock Market. Among these 20, in random order selected stocks, 6 made it onto the watch list, among them a former holding of mine. Let’s go:

101. Newtree

According to TIKR, this 17 mn EUR market cap company “provides chocolates, spreads, snacks, gifts, and coffee products. It also offers products through online”. On their investor website, annual accounts are only available to 2018. “Pass”.

102. Elia Group

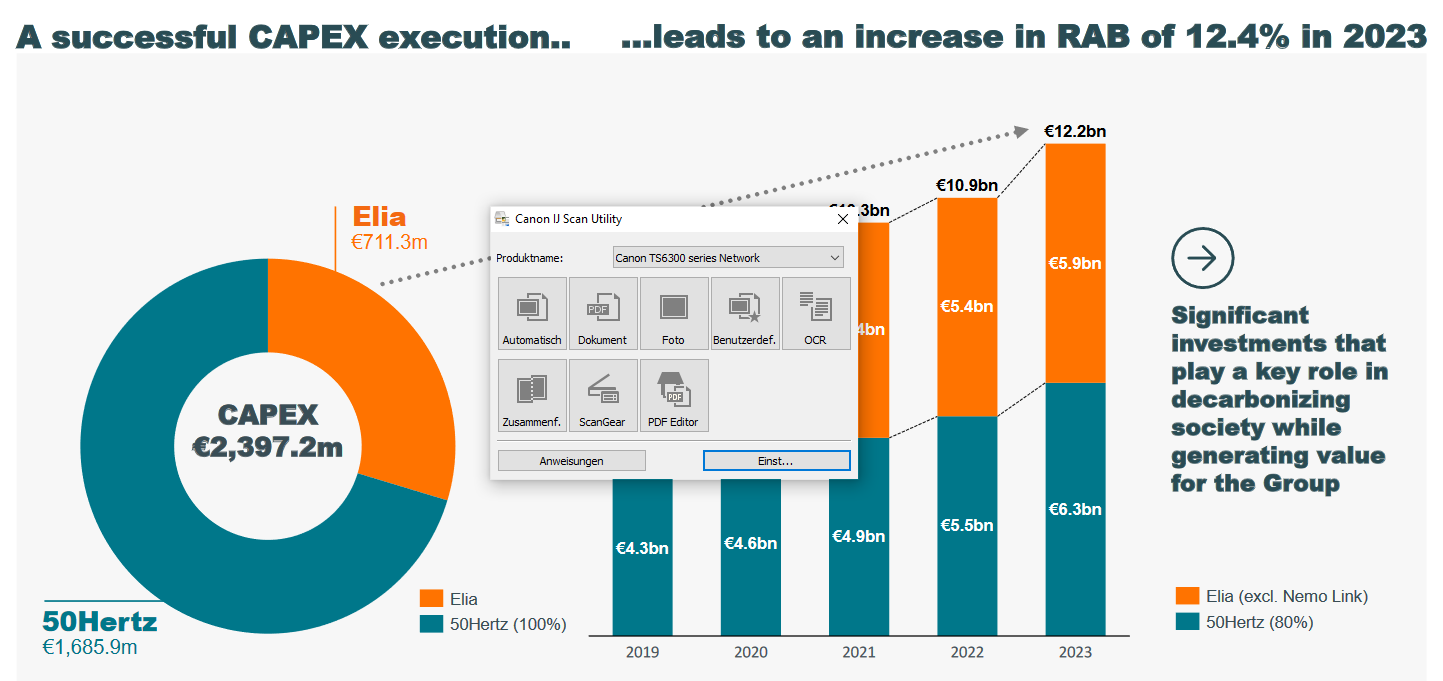

Elia is th 6,6 bn EUR market cap operator of the Belgian Electricity transmission network. They also own and run 50 Hertz, one of the larger German transmission network operators. Electricity transmission networks are fully regulated assets, i.e. if the network is working, the owner gets a guaranteed return based on the “Regulated Asset Base (RAB)”.

Usually those returns are somehow inflation indexed. In Elia’s case, the RAB is growing quite fast, but unfortunately profit is not growing. MAybe this has to to with the 9 bn of net debt. The valuation at ~11x EV/EBITDA or 1,3xEV/RAB is ok, especially as they have been able to grow RAB quite nicely:

The dividend yield of 2,2% is quite low for an infrastructure asset, but understandable with the type of growth.

Unfortunately, more than half of the company is owned by the Belgium Government. As I try to stay away from Government owned companies and the stock is not cheap enough for “deep value”, I’ll “pass”.

103. Arma (Expert MArket)

Arma is an Expert MArket stock where there is no recorded trade and no information available. “Pass”.

104. Immo Zenobe Gramme

This is another one of these Belgium companies that issue some kind of real estate certificates. The 12 mn market cap company has a relatively good stock price development for something RE related and seems to be a subsidiary of KBC. Nevertheless, “pass”.

105. Immobel

This 280 mn EUR market cap Real estate company has clearly seen better days. Although the stock price is down -75% from the peak, they still trade at 0,6x book value. “Pass”.

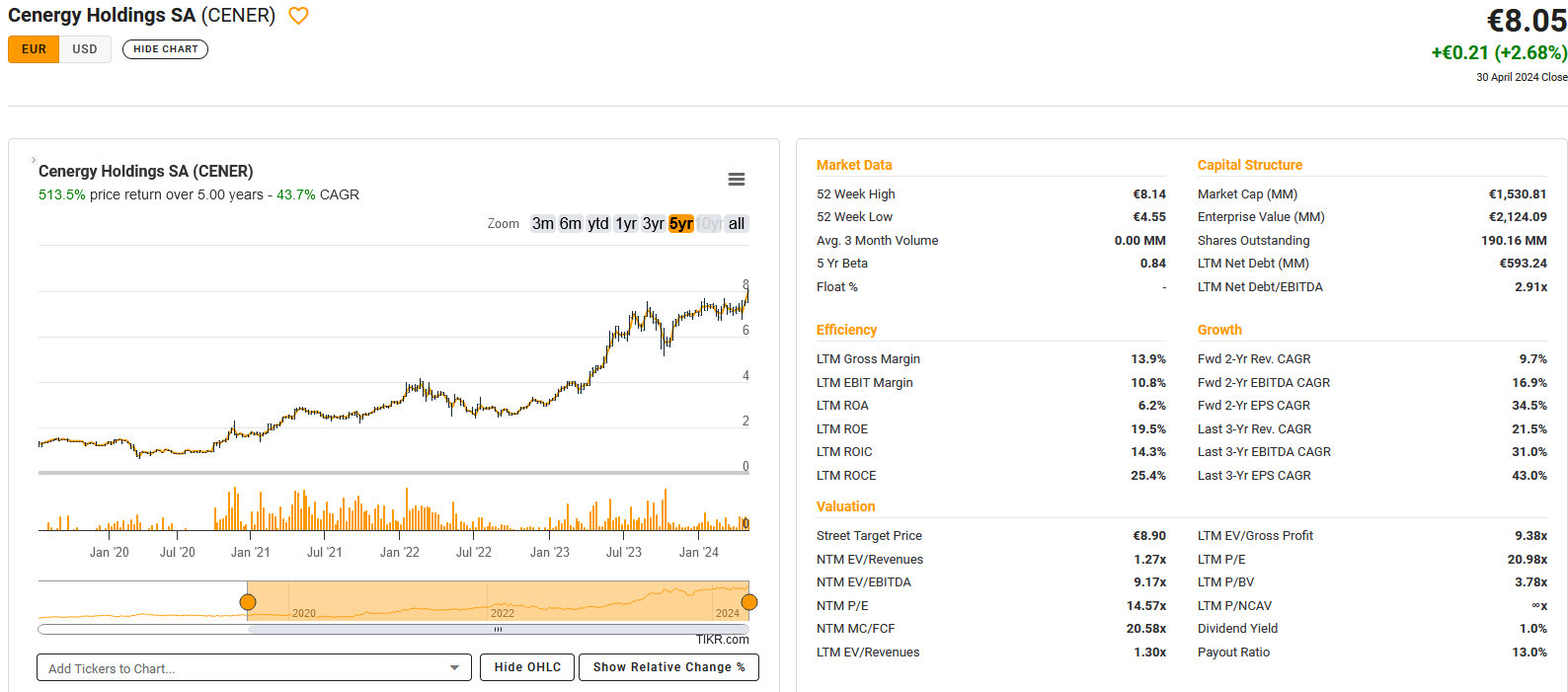

106. Cenergy

Now Cenergy, a 1,5 bn EUR market cap company looks very interesting. According to TIKR, “Cenergy Holdings SA manufactures and sells aluminum, copper, cables, steel and steel pipes, and other related products in Belgium and internationally.”

One doesn’t need to be EInstein to understand that manufacturing cables is good business these days and Cenergy’s stock price reflects that:

The company has been loss making in 2016/2017 but nicely recovered. Interestingly, 80% of the shares are held by a Greek Holding company. I honestly haven’t been aware that besides Prysmian, Naxan and NKT there is another listed cable manufacturer.

In any case, this is an interesting one which I will put on “watch”.

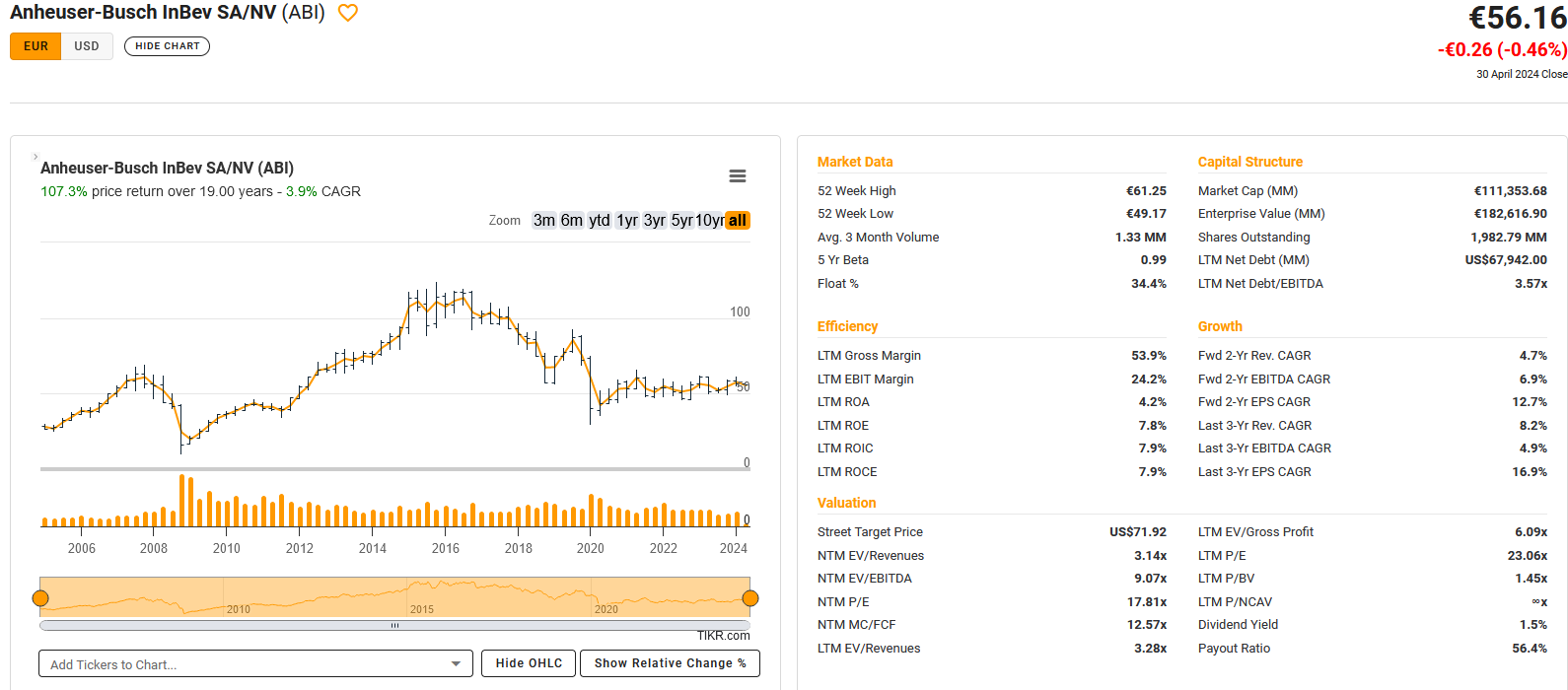

107. Anheuser-Busch InBev SA/NV (AB Inbev)

Technically, AB Inbev, the world’s largest brewer with a market cap of 111 bn EUR is a Belgian company, despite the fact that most of the business is done in the US and the company famously has been rolled-up by the Brazialian 3G (“Dream Big”) guys. As the other §G roll-ups (Kraft Heinz, Burger King), AB Inbev has been struggling for some time and the stock price did very little:

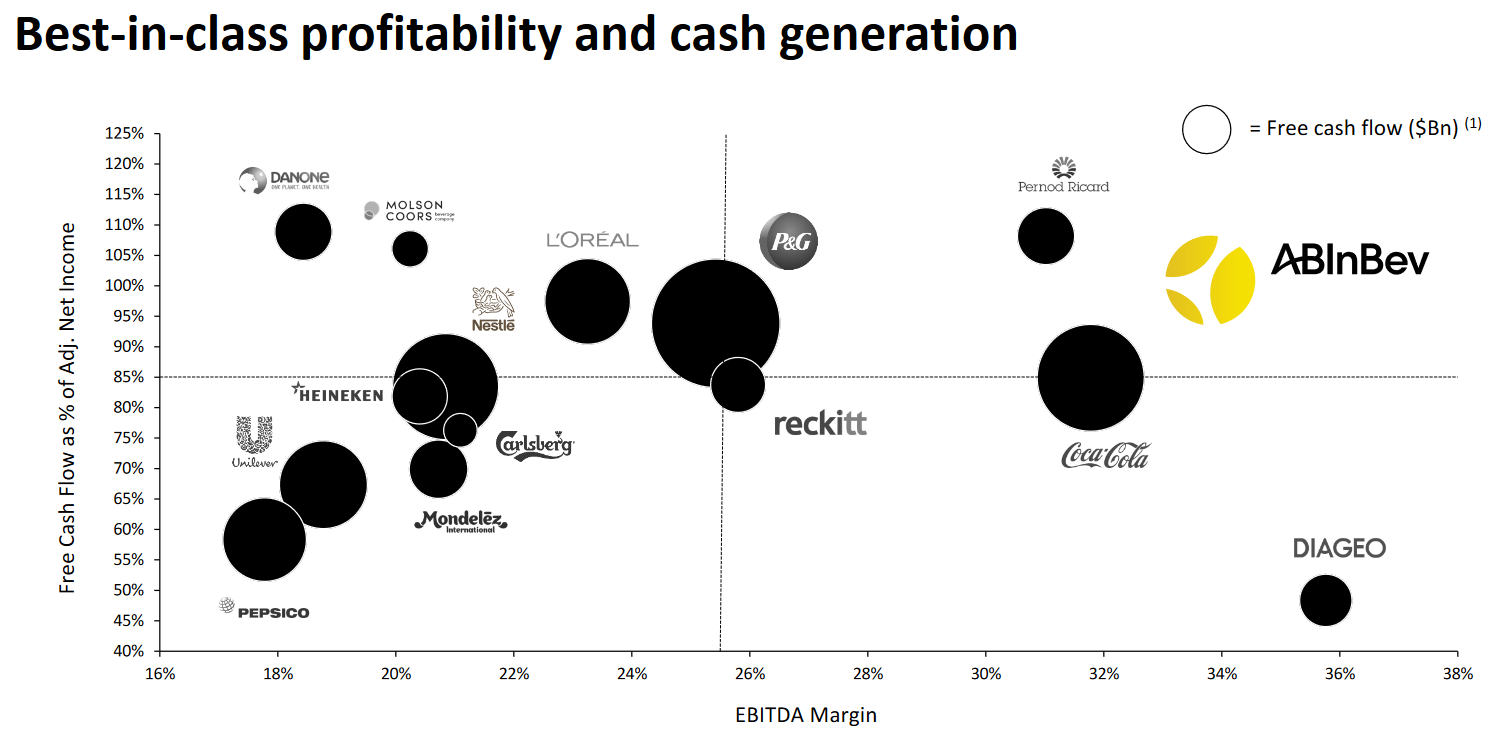

The stock is not very cheap, doesn’t pay a high dividend and has been doing nothing for many years. On the plus side are industry leading margins as can be seen in that chart from their IR presentation:

The big problem in my opinion is the still high amount of debt and really low return on capital. ROIC/ROCE is around 8% which is very low especially as they reinest most of their FCF into these low yielding assets.

They seem to have started buy backs, but only to a small amount, less than 1% of market cap. It would be interesting to understand, why return on capital is so low, normally the beer players have significantly higher returns compared to the Spirits guys who need to let their stuff age for a very long time.

AB Inbev s also a good reminder that bigger is not always better in the long run.

Still, I will put them on “watch”.

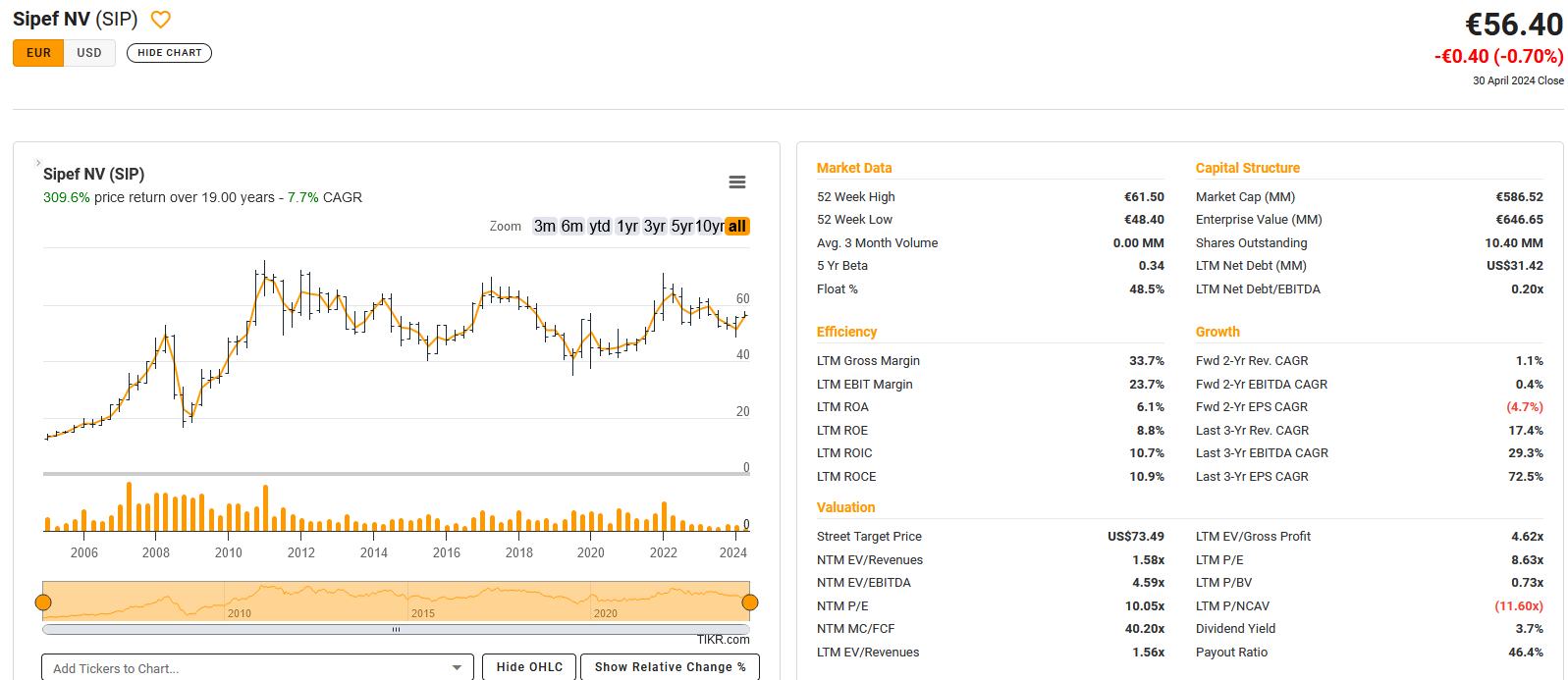

108. SIPEF

SIPEF with a market cap of 586 mn EUR is a quite “rare beast” in the stock market as it is one of the few European plantation companies. The largest shareholder with ~39% is Achermans van Haaren, the majority owners of DEME.

SIPEF mainly plants and harvests palm oil which is used among other things for soap. Palm oil has a pretty bad reputation from an ESG perspective, but SIPEF claims that their palm oil is “sustainable”.

The stock is quite cheap but has done little for a long time which is not so surprising for a capital intensive business that produces mostly commodities.

I think the stock could be interesting in the low part of a cycle but for me it is a “pass”.

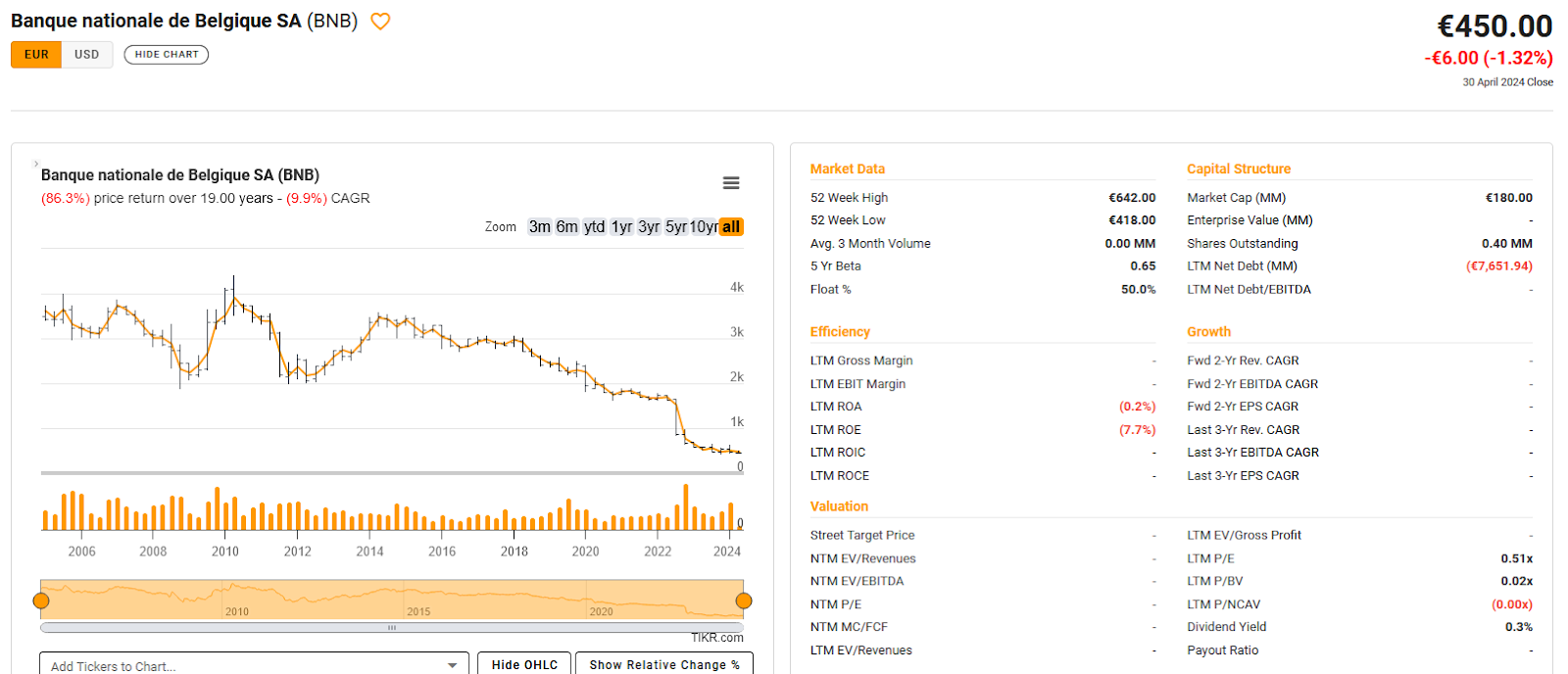

109. Banque Nationale de Belgique

This is actually the Central Bank of Belgum which is surprisingly stock listed and has a market cap of 180 mn EUR. I covered the stock (and the Swiss Central Bank) many years ago in the blog.

The stock price has been quite weak since then, so good that I didn’t follow up here:

The problem here is clearly that the juicy dividends have disappeared.

The problem seems to be that the Belgium National Bank is loss making. It would be interesting to understand if and when this could turn around. So I will put this “old friend” on “watch”.

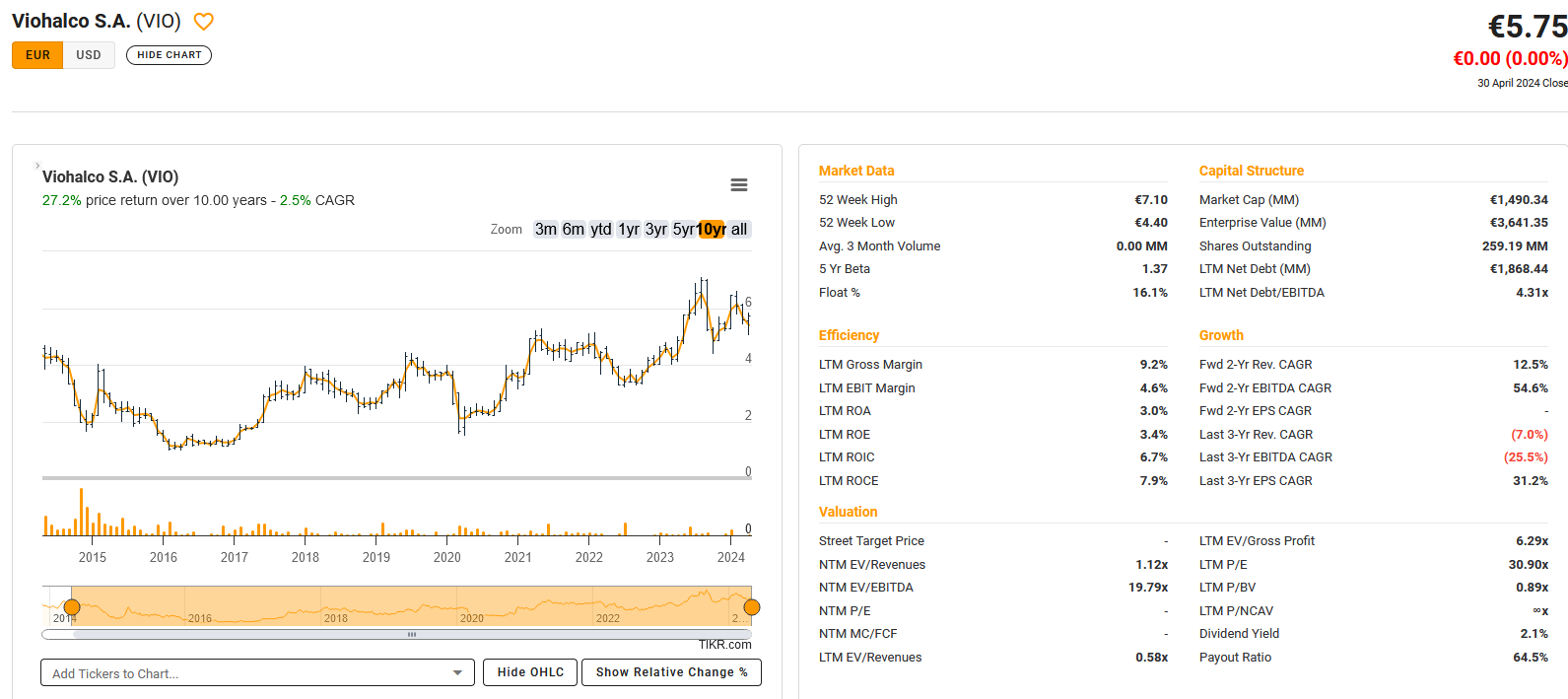

110. Viohalco

This seems to be the Hodiong Company of Cable maker Cenergy (Nr. 106) plus real estate and a lot of debt. The market cap is 1,5 bn. The Stassinopoulus family seems to own a fair amount of shares. The boss Nikos seems to be one of the richest people in Greece.

They seemed to have moved the company from Greece to Belgian 10 years ago. There seem to be more metal based activities in this Holdco, like Aluminium.

I am not 100% sure what to do with that one, but in doubt, I’ll “pass”.

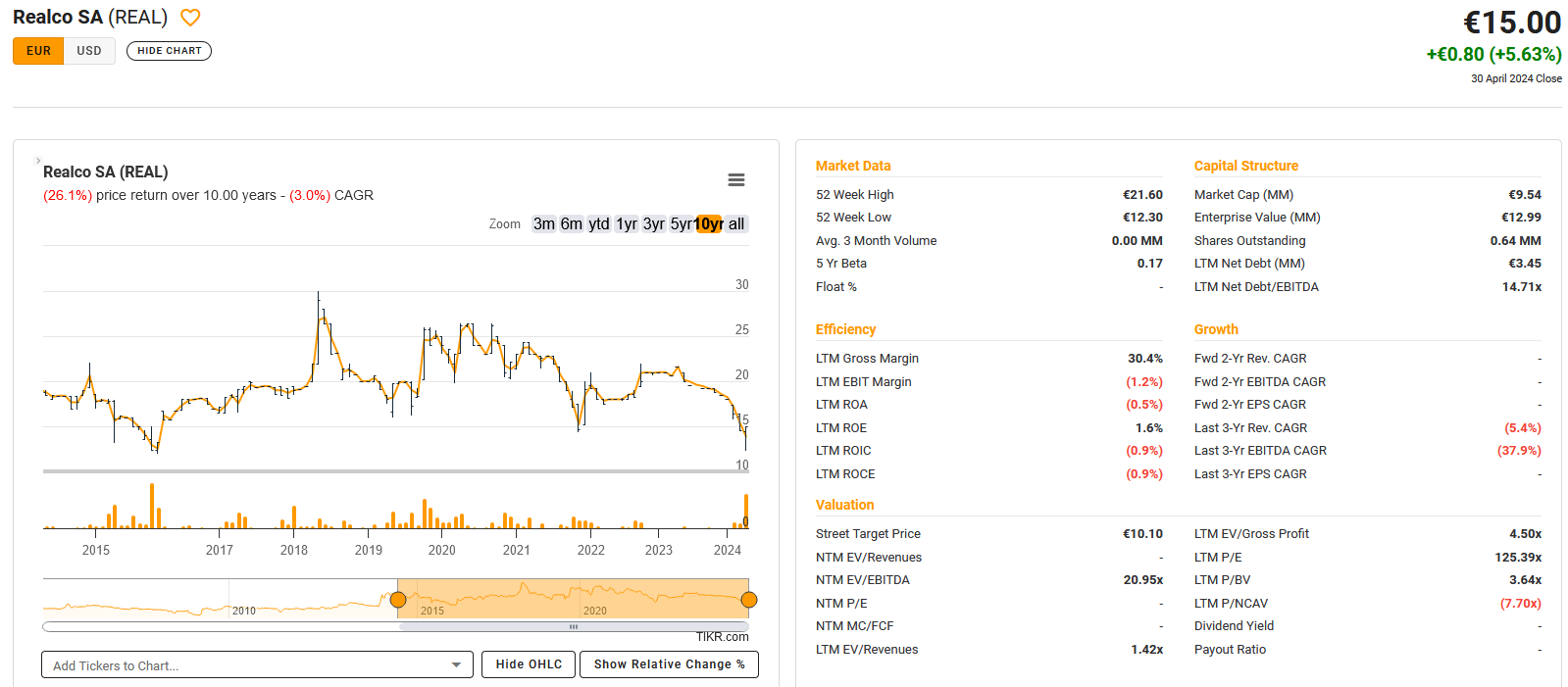

111. Realco

According to TIKR, this company “engages in the development, production, and sale of enzyme-based hygiene solutions and processes primarily in Belgium”.

Market cap is around 10 mn EUR, the share price has been going sideways with some volatility for the last 10 years.

Since 2020, the company has been loss making. “Pass”.

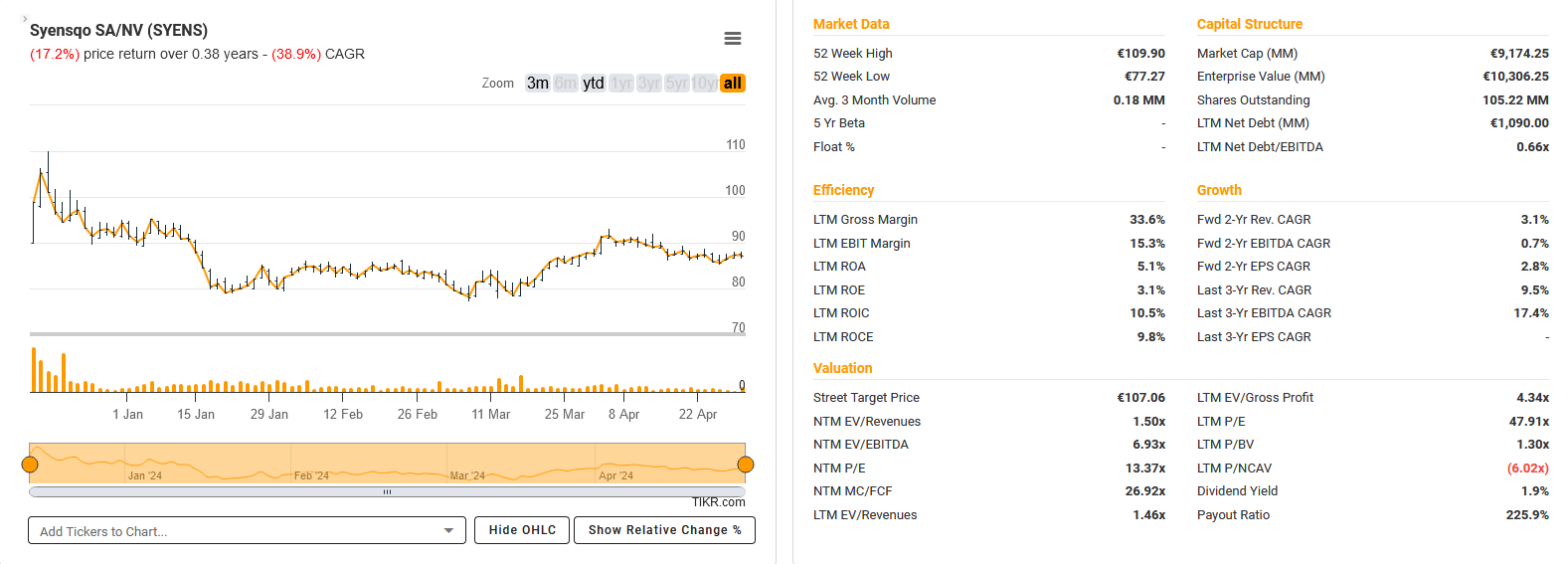

112. Syensqo SA/NV

Syensqo, a 9,2 bn EUR market cap company is a recent spin-off from Belgium Chemcial Conglomerate Solvay.

The stock so far traded downwards from the Spin-off date:

David Einhorn had announced that he had bought a position early 2024.

This is what Einhorn wrote in January:

As I think that Chemical companies could now be very interesting as a cyclical play, this one goes on “watch” with some priority.

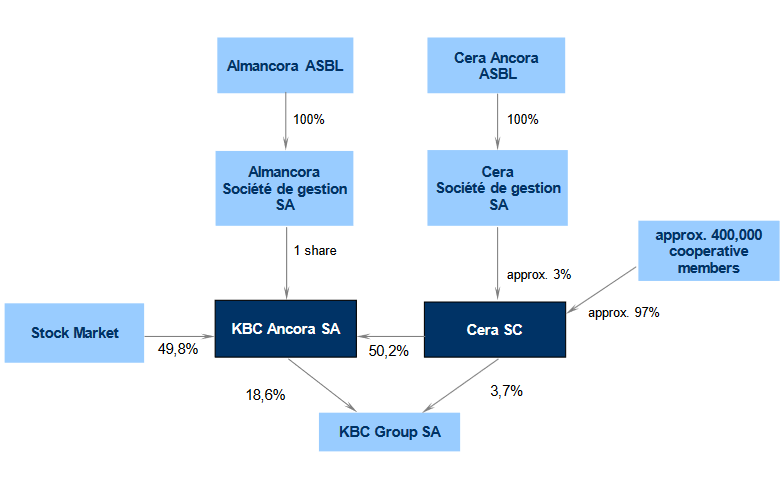

113. KBC Ancora

KBC Ancora is a Holding company that owns a stake in KBC Bank and has a market cap of 3,5 bn. The ownership structure of KBC is quite complicated:

Not my type of stock, so “pass”.

114. Mithra Pharmaceuticals

This 15 mn EUR market cap company has seen better days and is burdened with 300 mn in debt. According to TIKR it “develops, manufactures, and markets complex therapeutics in the areas of contraception, menopause, and hormone-dependent cancers in Belgium, Europe and internationally”.

The company is loss making and with this amount of debt, the clock is ticking. “Pass”.

115. Deceuninck

Deceunink, a 348 mn EUR market cap company “engages in the design, manufacture, recycling, and distribution of multi-material window, door, and building solutions in Europe, North America, Turkey, and internationally.”

As many of its peers, the stock looks cheap with the exception of the P/E but hasn’t done much over 10 years:

The high P/E compared to EV/EBIT seems to be the result of their sizeable Turkish operations that only look good before currency adjustments. Overall, nothing that excites me much, “Pass”.

116. Finasucre (Expert Market)

This Expert Market stock actually saw some trading in 2023. According to Euronext, the company “specializes in the production and marketing of sugar. In addition, the group develops production activities of renewable energy, alcohol, molasses, beet pulp, animal feed, natural ingredients, lactic acid and biodegradable and recyclable plastics.”

There is also a connection to Cie Bois Sauvage through an investment into an Insect Breeding start-up and other companies.

They also publish an annual report.

According to the annual report, they have 80 shares outstanding which gives them a market cap of around 280 mn EUR. Despite their operating businesses, they seem to have a lot of securities, participations etc. Book Value of equity is twice the market value.

I don’t know about the background of the Group, but overall this looks quite interesting. If time allows, I would want to digg deeper here. “Watch”.

117. Messer Belgium (Expert MArket)

Not sure if that is a part of the Messer Industrial Gases group, but this stock hasn’t traded at all according to the list. “Pass”.

118. Commerciale Belge (Expert Market)

Here Euronext has at least a description: “Compagnie Commerciale Belge is an investment company that specializes in the acquisition of shares in unlisted companies. At the end of 2014, the company holds 45.12% of Belreca.” Last trade was in 2019. “Pass”.

119. Infrabel (Expert Market)

This Expert market stock traded last in February 2024. According to Wikipedia, this seems to be the Government owned Railway company. They actually issue annual reports and even made a profit in 2022:

But investing with a Government is not my kind of thing, “pass”.

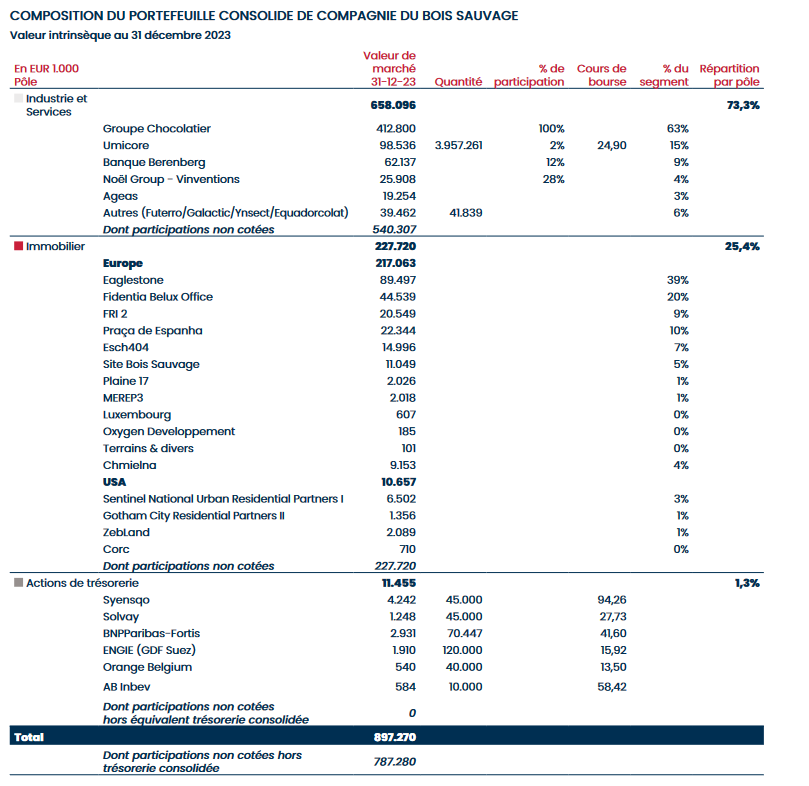

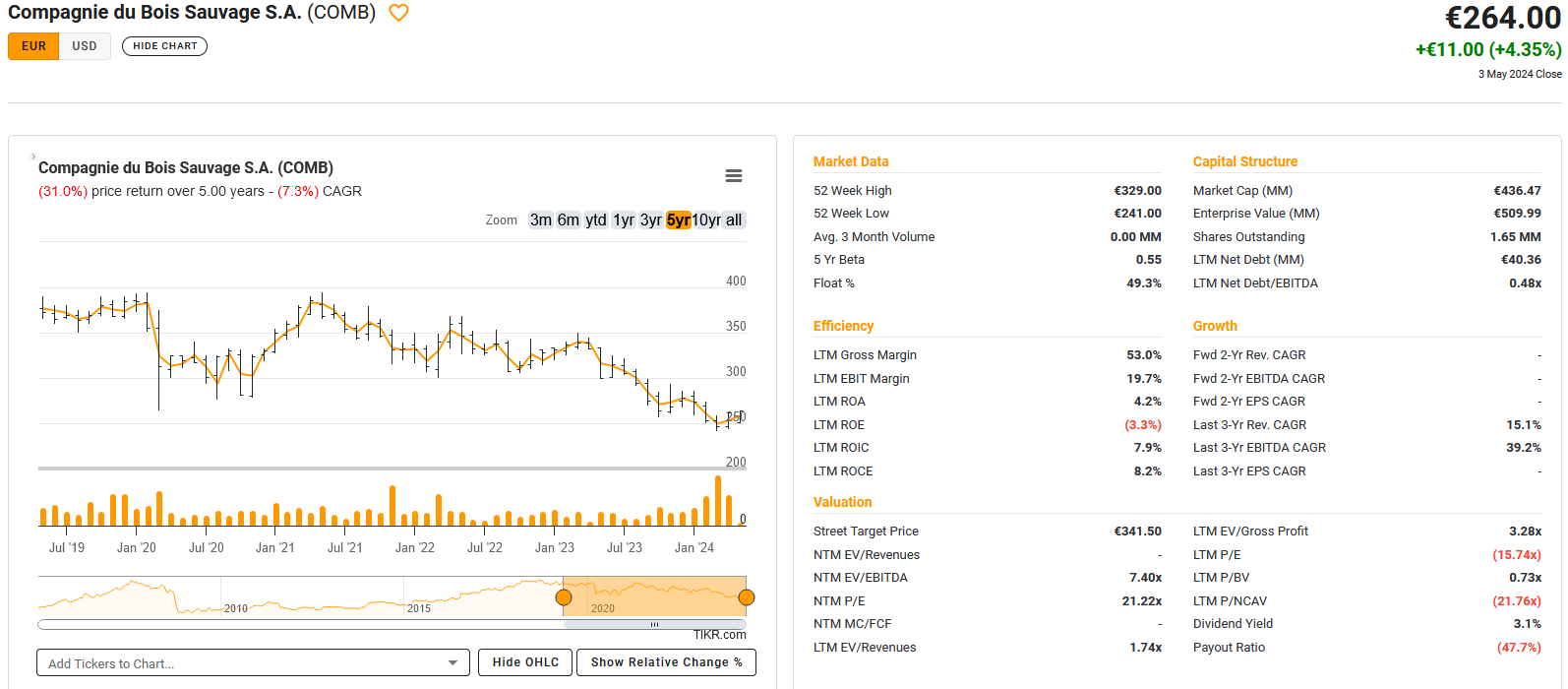

120. Cie Bois Sauvage

Bois Sauvage is a 436 mn EUR market cap Holding company that I have owned in the past. The company owns businesses in quite diverse sectors, the largest these days being (high end) Chocolate (63% of NAV), Real estate, a stake in a German Private Bank (Berenberg) and other interests.

This is the NAV calc from the 2023 annual report:

What makes the stock clearly interesting is that it trades at a discount of > 50% to the NAV. For the last couple of months, the share price suffered, not least because of the high price of Cocoa that is clearly an issue for Chocolate related businesses.

The P&L is noisy as losses in the securities portfolio (Umicore) are booked through P&L. In addition, the real estate exposure is also maybe not the most popular asset class at the moment.

The majority of the shares are held by the Paquot family. Guy Paquot, who created the Group died in 2019 during a Safari.

On the plus side, the Chocolate business actually owns Cocoa plantations in Ecuador and Bois Sauvage has resumed buying back shares and has no financial net debt.

This is clearly one of the most interesting stocks so far. Therefore they go on “watch”.