It is a comparable thought to WMC, Acres Industrial Realty (ACR) ($73MM market cap) can also be a mortgage REIT buying and selling at the same low cost to e-book worth (38% of BV) however with out the close to time period catalyst of a possible sale. ACR has gone by a couple of title and supervisor modifications through the years, it was initially Useful resource Capital (RSO), then grew to become Xantas Capital (XAN), and following a 2020 margin name of their CMBS portfolio, present administration got here in and as soon as once more rebranded. That is my third chew on the apple and is much less of a brief time period occasion pushed thought and extra a 2-3 12 months transformation path again to a standard industrial mREIT.

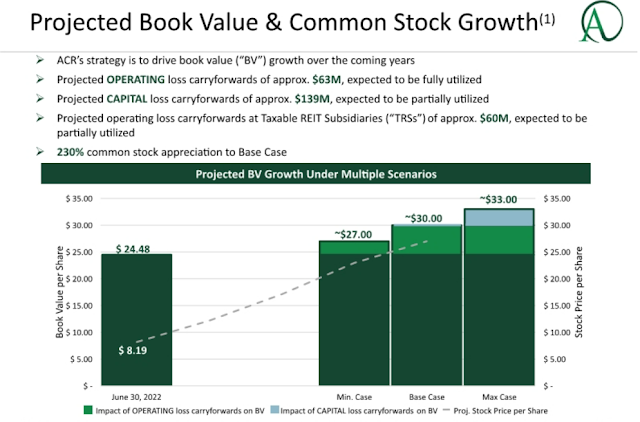

Whereas ACR would not have the close to time period catalyst of WMC, the property and steadiness sheet are cleaner at ACR and a majority of a budget worth will be attributed to its small dimension, present market situations and lack of a dividend, the latter being the primary attraction of mREITs to retail buyers. The explanation ACR would not pay a dividend is 2 fold, each of which ought to attraction to readers of this weblog: 1) since shares commerce at a big low cost, administration have been shopping for again shares, roughly $30MM price (vital for an entity this dimension) since November 2020, with $10MM remaining on their authorization; 2) following the 2020 margin name, ACR has a big quantity of each internet capital losses and internet working losses (“NOLs”). To monetize the web capital losses, ACR has created a facet pocket of opportunistic fairness actual property investments with turnaround plans that if executed ought to generate taxable revenue or positive aspects. These proceeds would then be reinvested within the core enterprise of originating and holding transitional industrial actual property loans. The tax asset is valued at $21.6MM (once more, significant for an entity this dimension), however has a full valuation allowance towards it on the steadiness sheet. As soon as the tax property are soaked up and the shares commerce nearer to e-book worth, the REIT will flip the dividend again on and retail buyers ought to return.

ACR lays out the tax monetization technique in one in all their slides, however this does not embrace the potential for extra accretive buybacks. Shares presently commerce for $9.26 vs. $8.19 under and I would not rely on it buying and selling for e-book ($24.48) anytime quickly, however the math they format is kind of enticing.

ACR’s core enterprise is originating and holding “transitional” industrial actual property loans, this sometimes means ACR will assist a developer or investor finance a value-add property, the fairness proprietor will execute on their plan over a pair 12 months interval after which will refinance the property at stabilization, taking out ACR’s mortgage within the course of. Over 3/4ths of ACR’s loans are to multi-family properties, I stay fairly bullish on this sector, a minimum of from a lender’s perspective. With rates of interest rising, potential new householders will probably be caught renting for a couple of extra years and ACR’s heavy focus to FL and TX (44% between the 2) ought to have continued demographic tailwinds as individuals/companies migrate to sunny skies and decrease price of dwelling geographies. If multi-family properties do get hit, ACR does have an inexpensive fairness cushion under every mortgage with a weighted common loan-to-value of 72%. ACR’s loans are floating fee, thus ought to have minimal length threat, though as charges proceed to extend, that added curiosity expense borne by their debtors will begin to improve credit score threat at a sure level.

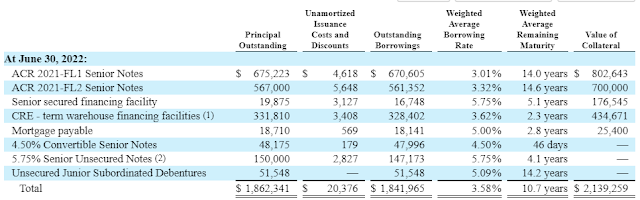

To fund their loans, ACR predominately depends on the CRE CLO market.

Newly originated loans are positioned within the “CRE – time period warehouse financing amenities” and as soon as of adequate dimension, they’re going to increase long run CRE CLO financing (additionally floating fee) and switch the warehoused loans into the CRE CLO. ACR retains the junior bonds and fairness of the CLO. CLOs are nice as a result of they are not mark-to-market automobiles and provides the supervisor flexibility to repurchase drawback loans contained in the SPV to keep away from any assessments failing that may trigger money flows to be diverted from junior tranches. Throughout the top of covid, CRE CLOs continued paying all noteholders and no check failures occurred, in contrast to within the CMBS market the place the collateral has an observable mark and was financed by way of repurchase agreements that have been marked-to-market every day. The CRE loans inside ACR’s CLOs are entire loans that aren’t syndicated and haven’t got dwell marks out there on them. ACR is probably going nonetheless being punished for 2020, however the supervisor is gone and the CMBS property that trigger the blow up are gone too. The CLOs originated by the previous supervisor all carried out tremendous.

There’s an exterior supervisor right here, Acres Capital, with a reasonably conventional mREIT charge settlement that features a base charge of 1.5% of fairness and 20% of earnings above a 7% hurdle, that is not nice, however they in any other case appear to be doing the suitable factor even when it goes towards their incentive within the close to time period (like shopping for again a big quantity of inventory). One factor I do not like concerning the charge settlement, the supervisor receives 25% of their incentive charge paid in inventory, at this low cost that is extremely dilutive to minority shareholders. However total, they personal 6+% of the corporate and appear to be affordable company stewards. There’s additionally the presence of two subtle credit score buyers which is a plus, Oaktree stays a big shareholder following the 2020 bailout with 9% and First Eagle Credit score Administration (giant CLO fairness investor, they handle ECC which owns CLO fairness and bonds) with 12.5% of widespread, plus a superb slug of the popular inventory (test these out when you like yield).

Disclosure: I personal shares of ACR