{kind=link}

Welcome to The Interchange! If you happen to acquired this in your inbox, thanks for signing up and your vote of confidence. If you happen to’re studying this as a publish on our website, join right here so you may obtain it instantly sooner or later. Each week, I’ll check out the most popular fintech information of the earlier week. It will embrace every part from funding rounds to tendencies to an evaluation of a selected house to scorching takes on a selected firm or phenomenon. There’s lots of fintech information on the market and it’s our job to remain on prime of it — and make sense of it — so you may keep within the know.

Good day! I’m excited to report the introduction of two new additions to this text. First, the superb Christine Corridor might be co-writing with me transferring ahead. Christine and I’ve truly recognized one another for 19 years, having used to work collectively on the Houston Enterprise Journal. She’s been masking fintech for the previous few years and I’m thrilled she might be engaged on The Interchange with me transferring ahead. Second, in the event you learn to the tip, you’ll see a emblem created only for the Interchange by TC’s unimaginable graphic designer, Bryce Durbin. I’m ridiculously enthusiastic about it. — Mary Ann

Thanks a lot to Mary Ann for that greeting! I’m excited to be working together with her in masking the broad world of fintech and stay up for contributing to what I biasedly contemplate the go-to publication for this trade. — Christine

Now on to the information.

Celebrating female-led ventures

I, as a lot of you I’m certain, proceed to be dissatisfied within the lack of LP (restricted associate) {dollars} flowing towards female-led enterprise capital companies. So you may think about my pleasure once I obtained an e mail a couple of new enterprise agency, known as Vesey Ventures, that was based by three feminine former managing administrators of Amex Ventures who had lately closed a $78 million debut fund.

Vesey’s self-described mission is to again corporations “remodeling monetary providers” on the seed to Sequence B phases. It plans to take a position $1.5 million to $3 million as preliminary checks, and bigger quantities for follow-ons. Primarily based in the USA and Israel, the fund has to date backed 5 startups, together with Coast, Cyrus, Grain, Equi and Correct.

The trio wouldn’t say whether or not Amex is an LP in its new fund however implied there have been no laborious emotions once they all determined to go away (at the very same time in late 2021, thoughts you). Personally, in addition to the truth that this implies more cash on the market for fintech startups, I do love that Dana Eli-Lorch, Lindsay Fitzgerald and Julia Huang labored collectively for a couple of decade and obtained alongside so properly as colleagues and mates that they determined, “Hey, let’s do that on our personal.”

Clearly, their monitor file impressed sufficient LPs — together with seven “outstanding” unnamed monetary establishments — that they had been in a position to shut the fund in a really difficult macroenvironment. Throughout their time at Amex, they labored on investments in corporations equivalent to Plaid, Stripe, Melio and Trulioo. In addition they labored quite a bit on serving to fintechs construct partnerships with incumbent monetary establishments — expertise they plan to make use of to supply portfolio corporations bespoke “Technique Sheets” alongside time period sheets.

Vesey defines fintech in its broadest sense — which means that it invests exterior of conventional classes of economic providers equivalent to client and B2B. It additionally appears to be like at vertical software program, embedded fintech, the way forward for commerce and the infrastructure layer — equivalent to cybersecurity, danger and compliance.

It made my week to have the chance to cowl this information, not going to lie. Right here’s to more cash flowing to feminine buyers, and founders, too!!

Talking of which, I additionally lined the $15 million elevate for Kindred, a home-swapping community. Whereas that firm is extra proptech than fintech, I’m mentioning it as a result of it was additionally based by ladies who beforehand labored collectively — on this case, at Opendoor — and noticed a possibility to department out on their very own. — Mary Ann

Vesey Ventures founding companions Lindsay Fitzgerald, Dana Eli-Lorch and Julia Huang Picture Credit: Vesey Ventures

Fintech funding in Q1

This week, we took a have a look at international fintech funding for the primary quarter of 2023 and located some notable tidbits.

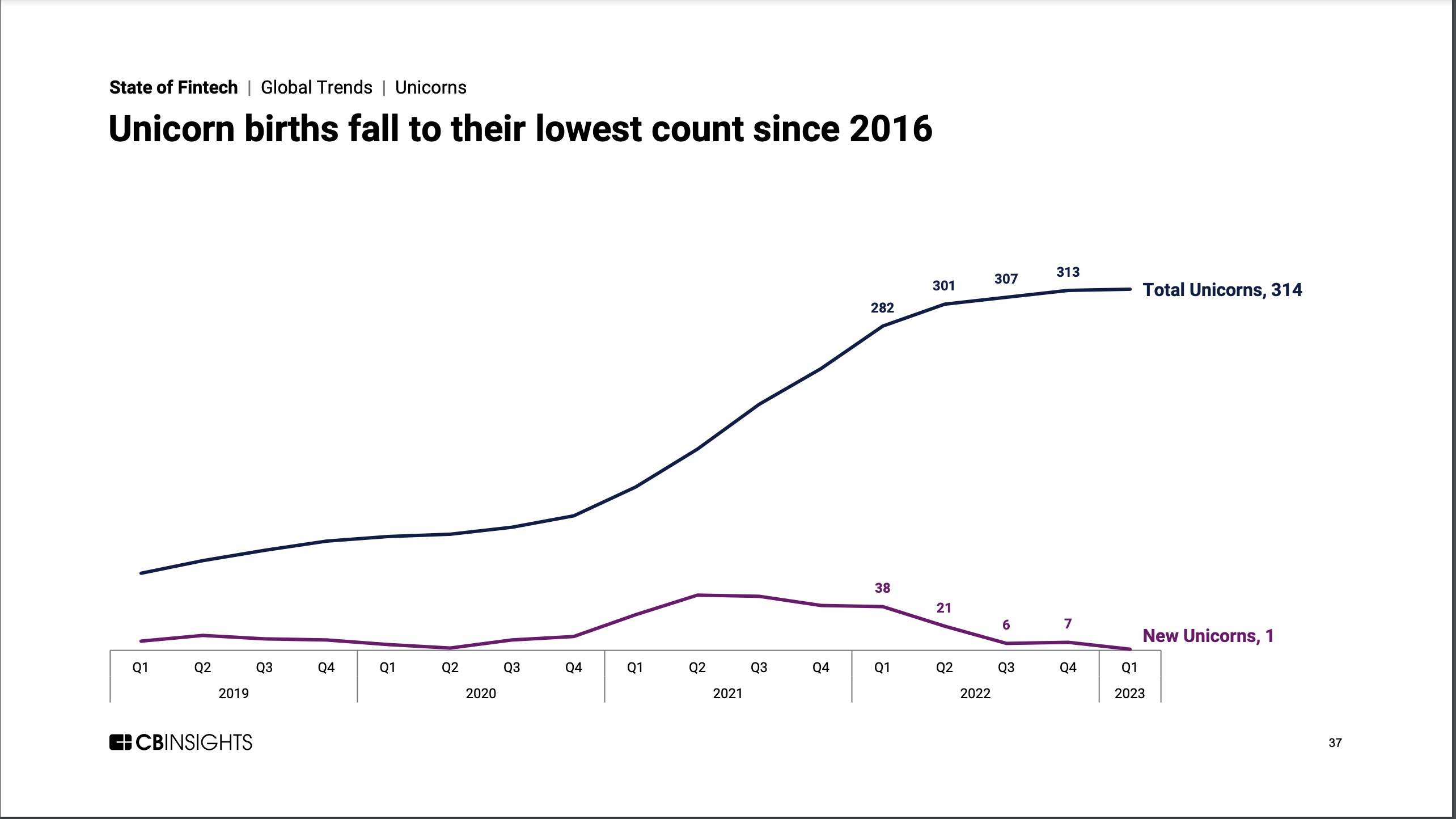

First issues first, funding for the quarter totaled $15 billion, which is up 55% from the fourth quarter, however clearly exhibiting a market correction because of the staggering quantities fintech corporations raised in each 2021 and 2022.

And, it’s vital to notice that of that $15 billion, $6.5 billion was Stripe’s elevate. With out that deal, CB Insights stated funding would have amounted to $8.5 billion, or a 12% drop in funding from the fourth quarter of 2022.

In the meantime, 2022 was flush with fintech corporations reaching unicorn standing, with 72 unicorns minted that yr, and 38 within the first quarter alone. That was seemingly aided by the plethora of obtainable capital flowing into the sector, nonetheless; within the first quarter of 2023, only one fintech firm was minted a unicorn: Egypt-based MNT-Halan, which in early February raised $260 million in fairness financing at a $1 billion valuation. Based on the CB Insights’ newest State of Fintech report, that is the primary time that has occurred because the finish of 2016.

Although MNT-Halan was the one firm to earn a horn, the primary quarter was ripe with “megarounds,” the time period for offers valued at $100 million or extra. There have been 16 offers like this, totaling $9.2 billion, a rise of 179% over the fourth quarter of 2022 and accounting for 61% of complete funding within the first quarter, CB Insights reported. After Stripe’s $6.5 billion deal got here Rippling, which raised $500 million in mid-March as Silicon Valley Financial institution was melting down. Notably, deal rely was down, dropping 24% quarter over quarter. — Christine

Picture Credit: CB Insights

Apple pushes additional into fintech

Does each tech firm wish to turn out to be a fintech? As reported by Romain Dillet: “Apple Card prospects within the U.S. can now open a financial savings account and earn curiosity by an Apple financial savings account. To be taught the specifics about Apple’s new providing, click on right here. When the corporate initially introduced the brand new monetary product again in October, Apple stated that it couldn’t share what rate of interest could be paid out on these accounts as a result of charges are fluctuating a lot as of late. As of immediately, Apple goes to supply an APY of 4.15%.” You may learn extra particulars on the transfer right here.

In the meantime, Moody’s Traders Service issued a brand new report summarizing its view that buyers’ potential to understand increased yields on their money by the tech big’s new financial savings account (which is being provided in partnership with Goldman Sachs) — if properly built-in into the Apple ecosystem — “is credit score detrimental for incumbent banks and money alternate options equivalent to cash market funds.”

As we all know, the brand new financial savings account deepens Apple’s providing of economic providers merchandise, which already features a digital pockets, bank card and its purchase now, pay later credit score providing, Apple Pay Later. As Moody’s factors out, “the enlargement aligns with a typical expertise agency technique to extend the scope, utility and enchantment of their digital platforms.”

“If Apple promotes the financial savings product aggressively, it might entice a big quantity of financial savings to the Apple ecosystem and away from conventional banks. By means of the partnership, Goldman Sachs may gain advantage from elevated deposit funding by the broad attain of Apple’s digital ecosystem,” stated Stephen Tu, a vp with Moody’s Traders Service, in a written assertion.

Moody’s additional added: “Whereas there are already many higher-yielding money alternate options accessible for many customers, Apple’s higher-than-average charge of curiosity on the account mixed with its easy and simple to make use of ecosystem might incentivize customers to shift funds to the Apple platform from incumbent monetary establishments.” — Mary Ann

(Disclosure: My husband works for Apple, however not in any capability associated to this challenge.)

Different weekly information

Lili claims tremendous app standing with new accounting platform

Greenwood — a digital banking platform for Black and Latino people and companies — goes reside for all, cancels waitlist (TechCrunch lined the corporate’s 2021 $40 million elevate right here.)

UK-based Finastra companions with Plaid to present customers entry to fintech apps

Airbase provides guided procurement to spend administration platform

On-line actual property agency Opendoor cuts 22% of workforce (TechCrunch lined the corporate’s earlier spherical of layoffs, which affected 18% of its workers at the moment, final November.)

Bain Capital Ventures’ Matt Harris printed a chunk on how banks must be working with startups: Classes from Historical Rome: How banks can be taught to like startups

Fundings and M&A

Seen on TechCrunch

Accounting automation startup Trullion lands $15M funding

And elsewhere

Wealthtech-proptech-fintech crossover Plotify raises $12.5 million in fairness financing

Actor Ryan Reynolds Buys Place in Canadian Funds Tech Firm Nuvei

Insurtech Capitola raises $15.6M Sequence A from Munich Re

Clerkie raises $33M Sequence A funding from prime buyers to handle the damaged debt system

French expense administration agency Mooncard luggage €37M Sequence C funding

YELO Funding, a university financing startup, declares $1.2 million in pre-seed funding

TiiCKER, a shareholder loyalty and engagement platform, raises $5M in seed spherical

Residential expertise firm Habi receives $100M credit score facility from Victory Park Capital

Waste administration funds startup CurbWaste raises $4M

Now, right here’s that emblem I promised! Isn’t it fairly?!

Picture Credit: Bryce Durbin

That’s it for this week. It felt slightly gradual however hey, typically, that’s okay 🙂 Hope you all are having unbelievable and fun-filled weekends! See you subsequent time. xoxoxo, Mary Ann and Christine