{kind=link}

Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!!!

Abstract:

In my relentless effort to create probably the most boring and unremarkable inventory portfolio conceivable, I believe I recognized an excellent candidate with SFS Group from Switzerland. Regardless of having a market cap of ~4 bn CHF, this majority family-owned firm will not be very well-known and its merchandise and B2B enterprise mannequin look similarily unremarkable.

The corporate doesn’t have an simply identifiable moat, doesn’t pay excessive dividends or buys again inventory, will not be tremendous low cost and in addition not tremendous worthwhile, doesn’t develop like loopy and doesn’t have horny merchandise that one can see within the grocery store.

However I do assume it’s an nice addtion to my portfolio as it’s attractively priced and each, the enterprise in addition to the administration are of excessive (Swiss) high quality. Primarily based by myself estimates, the inventory trades at a PE of ~12x for 2023, regardless of having delivered EPS development in EUR of round 15% p.a. since its IPO in 2014 and maintaing double digit EBIT margins throughout the cycle.

Because the put up has turn out to be fairly lengthy, right here an summary of the chapters:

- Background

- Firm Historical past

- Enterprise Mannequin

- Why did I turn out to be ?

- The place does the expansion and margin enhance come from ?

- Moat and competivie benefits

- The Hoffmann Group acquisition

- Administration

- Shareholders

- Valuation

- Dangers

- Different stuff

- Professional’s and Con’s

- Abstract & Return expectations

- Sport plan

1. Background:

SFS Group has been on my watchlist since 2021 once I encountered them in my “All Swiss shares” collection. Again then, the inventory regarded too costly regardless of displaying some engaging traits (EBIT margins, ROC and many others.). Within the meantime, they’ve made a major M&A transaction and the share worth got here down by-25%.

2. Firm historical past:

![]()

Regardless of being a 95 12 months outdated firm, SFS Group solely IPOed in 2014 at a share worth of 64 CHF. In accordance with the very detailed firm historical past, they went worldwide in 1971 and added new enterprise and enterprise strains alongside the way in which on an opportunistic foundation. SFS Group’s Web site, it’s not really easy to grasp what they’re really doing. Due to this fact let’s leap into the enterprise first:

3. Enterprise mannequin

Successfully, they’re lively in 3 totally different segments that I attempt to describe in my very own phrases:

a) Manufacturing of a various vary of very small however “Mission vital” excessive precision components for quite a lot of clients. SFS elements will be present in vehicles, cellphones and even Airplanes

b) Manufacturing of fastening and riveting options which are used within the development and industrial sector

c) Distribution of instruments to manufacturing companies. Initially solely in Switzerland however since 2022 additionally through an acquisition internationally.

What these segments have in frequent, that they’re all centered on B2B enterprise fashions catering to bigger corperates. Inside these 3 segments, SFS operates 8 totally different divisions that appear to be kind of unbiased:

To get a a primary overview on their large number of merchandise, their very own product website is an efficient place to begin.

Certainly one of their slogans is “native for native”, so that they manufacture regionally in round 100 websites in 26 international locations around the globe. The HQ primarily coordinates and helps if additional know-how is required, as an example to develop new particular machines.

4. Why did I turn out to be ?

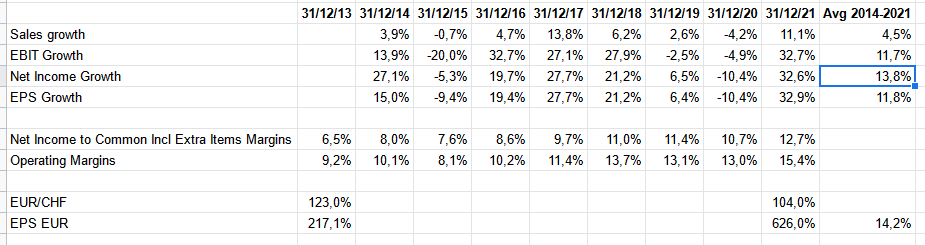

Since its IPO in 2014, SFS Group has delivered very strong outcomes regardless of having confronted ultimately 2 disaster and a really sturdy CHF. That is how margins and earnings developed from 2014 to 2021:

Regardless of growing gross sales solely by 4,5% (in CHF), SFS managed to enhance Web revenue by ~14% p.a. and EPS in nearly 12% by annum since its IPO. This was primarily achieved by bettering margins signifcantly. EBIT margins improved from 9-10% to fifteen% and internet revenue margins nearly doubled.

As an Euro investor, one also needs to take note of, that over this era, the CHF elevated considerably towards the EUR from 1,23 to 1,04. So in Euro, EPS would have elevated even 14,2% p.a. vs. the 11,8% in CHF.

Now comes the attention-grabbing half: This enhance in margins and earnings went together with a steady lower in valuation as we will see within the subsequent desk:

Possibly the valuaion on the IPO was priced too wealthy, however for a “Swiss high quality” firm, SFS doesn’t look costly as of late. As we will see within the inventory chart, IPO buyers may not be too completely satisfied, as SFS has even underperformed the SMI because the IPO:

To me, an organization with steadily growing margins is value taking a look at anyway and mixed with a declining valuation much more so.

5. The place does the expansion and margin enhance come kind ?

Trying one degree beneath the Group to the segments, we will see a really attention-grabbing, diverging improvement:

The three segments diverge fairly broadly. The smallest section, the Swiss centered Distribution section has kind of stagnated, each in high line and working revenue. The most important section, Engineered Parts, has carried out very soldily. Nevertheless the star section was clearly the Fastening methods section that nearly doubled gross sales and improved working revenue by 5x. This section is clearly the primary driver for the time being and appears to have carried out very properly in 2022 as properly.

6. Moat & Aggressive benefits

In my understanding, SFS doesn’t have a “arduous Moat”. Nevertheless, they appear to have some aggressive benefits. Particularly within the Engineered division, the competivie benefit appears to be the detailed know-how in sure manufacturing applied sciences, together with the design of particular machines, that enable them to supply excessive precision elements in areas around the globe.

Many merchandise that they produce are solely a small portion of the ultimate product in absolute worth, however fairly necessary for the performance which is usually a superb place to have as a provider. They appear to be very consumer centric and attempt to turn out to be a improvement accomplice moderately than an exchangeable provider for his or her shoppers.

On a extra strategic degree, the truth that SFS remains to be a household owned firm. appears to present them entry to sure M&A transactions the place the vendor doesn’t need to maximise the value however desires to make it possible for the corporate stays a comparatively independently run enterprise. So far as I perceive, the Hoffmann Deal was an instance but additionally doable as a result of hey are nonetheless household owned.

So total, no arduous moats however a mix of aggressive benefits that enable them to earn respectable margins and returns whereas rising at a passable velocity.

7. The Hoffmann Group Acquisition

In late 2021, SFS introduced that they may take over the German Hoffmann Group, a privately owned, 1 bn EUR gross sales device distribution and producer. For SFS , that is clearly the most important transaction in its historical past and as such clearly a danger. SFS has paid ~1 bn for Hoffmann, I haven’t seen any specific EBIT/revenue numbers for Hoffmann but.

A number of components would possibly mitigate the dangers:

- SFS and Hoffmann collaborate since greater than 20 years and in line with Breu have related values and tradition

- Hoffmann will run as an unbiased division

- The Hoffmann CEO will be a part of the manager board

- A sure a part of the acquisition worth has been financed with on stability sheet money and shares, the remaining leverage will not be vital. (<1,5 Web debt/EBITDA)

In one of many interviews, the CEO talked about that with this acquisition they plan to open up a 3rd platform on high of the manufacturing and Fastening sector, as distribution to this point was solely an area Swiss enterprise. In addition they appear to mean to develop this platform internationally. As well as, a few of SFS merchandise may be bought through Hoffmann (Fastening).

The Acquistion was consumated as of Could 1st 2022. This leads to an attention-grabbing impact that the 2022 outcomes will solely embrace 8/12 of the earnings influence, whereas debt and addtional shares are already totally accounted as of 12 months finish. so EV/EBIT and EV/EBITDA at 12 months finish 2022 are usually not totally represetative.

Simply the impact of totally together with Hoffmann in 2023 will enhance gross sales by one other ~12,4% vs. 2022 (all different issues equal).

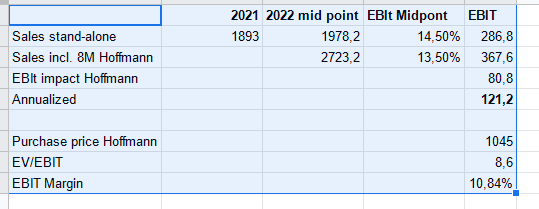

Thus far, SFS has circuitously talked about how worthwhile the acquired enterprise is. Nevertheless, administration has dropped some hints, particularly of their second investor day with this slide:

With this info, one can estimate the anualized 2022 EBIT of Hoffmann in addition to the EBIT margin and the implied a number of that SFS paid which I did on this desk utilizing mid factors for all estimated ranges:

So total, the Hoffmann acquisition appears to have been carried out at a fairly affordable a number of. Though the EBIT margin is decrease than the common EBITT margin of the SFS Group, a double digit EBIT margin remains to be good and buying this for an EV/EBIT of round 8,6 is clearly not overpaying.

It must be talked about nevertheless that Hoffmann didn’t grew that a lot for a few years. That is from a 2021 presentation and would possibly clarify the comparatively low cost worth:

One other attention-grabbing facet is that ~25% of Hoffmann’s gross sales appear to be their very own device manufacturers.

8. Administration

The CEO Jens Breu (since 2016) has an attention-grabbing background. He isn’t from the founding household and in addition not a “MBA/McK clone” however began as an industrial apprentice and labored his approach up after becoming a member of SFS in 1995. I’ve watched a few movies with him and I’m truthfully tremendous impressed together with his down-to-earth method.

On the age of fifty years, he clearly has some years to go, however mixed already with a whole lot of expertise. He’s additionally member of the Supervisory board of Daetwyler, one other, 3,5 bn market cap “Hidden Swiss Champion”. Total it appears that evidently SFS Group principally develops Administration from inside as a substitute of hiring “Mercenaries”, an method I like loads.

The supervisory board comprises members of the founding famlies Huber and Stadler. The long run CEO and Supervisory board head Heinrich Spoerry retired (as a result of age) in 2021 and was changed by the previous CEO of Schindler, Thomas Oetterli. Oetterli himself was a part of the Supervisory board since 2011, so continuity appears to be ensured. The Supervisory board could be very Swiss, as a coicidence, one of many members (Urs Kaufmann) heads the Supervisor board at Schaffner Group, one other o my Swiss holdings.

Curiously, one member of the founding household, Claude Stadler is Govt Director and HEad of Company providers, proudly owning round 400K shares (or 40 mn CHF) however he appears to maneuver out by the top of 2024 with a purpose to deal with the household workplace.

Compensation for the overall government board was ~7 mn CHF in 2021, with 1,6 mn CHF for the CEO which I believe is kind of low. Jens Breu owns ~28k shares and will get round 2500 shares per 12 months as a part of his compensation bundle.

9. Shareholders

Even after the capital enhance to finance the Hoffmann transaction, the founding households Huber and Stader personal greater than 50%, joined now by the heirs of the Hoffmann Group with 4%. There are not any different “well-known” or noteworthy buyers in line with TIKR.

10. Valuation

Utilizing SFS’s forecasts from above, the midpoint estimated EBIT for 2022 would by 370 mn CHF. Assuming ~10 mn of curiosity bills and 20% in taxes, this would lead to 7,55 CHF per share in Incomes for 2022 or, at a share worth of 105 CHF a trailing p/E of ~13,9. For a top quality firm like SFS this isn’t tremendous low cost however fairly cheaup.

Nevertheless, wanting into 2023, issues seems much more attention-grabbing. Assuming a 4,5% development charge in earnings plus the impact of the total 12 months for Hoffmann, I anticipate round 433 mn EBIT and ~8,70 CHF EPS. This may imply a P/E of solely 12x and an EV/EBIT of ~11x for 2023.

another “Swiss high quality manufacurers”, we will see that this seems actually low cost, though gamers like VAT and LEM are clearly extra worthwhile:

Daetwyler nevertheless, could be clearly a peer to SFS they usually commerce at round 2x the valuation of SFS Group.

What I discovered attention-grabbing is, that promote facet analysts who cowl SFS have considerably decrease estimates wich for my part don’t mirror the Hoffmann acquisition:

The Bloomberg consensus is just 6,72 EPS GAAP for 2022 and seven,00 for 2023 which is considerably even beneath the low finish of managment estimates. For some causes, the promote facet appears to disregard this acquistion.

Trying to 2024 and additional, I believe it’s life like to imagine a strong mid-single digit development charge

11. Dangers

Thus far now we have centered on whats good and attention-grabbing. However there are clearly dangers. Amongst them are:

- the enterprise is geared in direction of the manufacturing and development trade. A significant and prolongued slowdown on this sectors may even hit SFS

- An M&A transaction in that dimension is at all times a danger

- The Hoffmann transaction will increase the burden in direction of Europe, particularly Germany

- The corporate has publicity to China particularly within the very worthwhile Fastening division

Structurally, the largest wager one is making with SFS is that European manufacturing is not going to die. Studying the press as of late, as soon as once more many individuals assume that Europe will turn out to be a historic theme park for wealthy Asian vacationers. This may be clearly not optimum for SFS. Personally nevertheless; I do imagine that prime high quality manufacturing has really a reasonably good future in Europe. The latest disaster has proven that suply chains shouldn’t be too lengthy and that the outsourcing of producing will not be a good suggestion.

As well as, the approaching Power transition requires a whole lot of manufacturing and because it seems like, the US and Europe is not going to make the identical mistake once more and outsource all the things to China. My feeling is that prime worth manufacturing might have a reasonably respectable future.

12. Different matters (Reporting, Capital allocation, Cashflow era and many others.)

What I do like about SFS that they’ve superb reporting. One very particular merchandise that I like is how the current returns on capital. The present Return on invested capital (ROIC) in addition to ROCE.

Beneath Siwss GAAP, they’re allowed to deduct Goodwill immediately from Fairness after they make an acquisition. Due to this fact the ROIC (based mostly on Fairness and internet debt) would look fairly good however they’re displaying and are monitoring the “actual” numbers:

As well as, they at all times present clearly which a part of the expansion is natural and which is due to M&A. Many firms don’t do that.

Total, capital allocation for my part is nice. They appear to be disciplined in M&A, have a transparent dividend goal and are occassionally shopping for again some inventory though they used the prevailing treasury shares for the Hoffmann acquistion. One mustn’t anticipate massive and even debt financed share purchase backs from SHS. Following the Hoffmann acquisition, they’ve clearly communicated that they prioritize lowering debt and that they even goal a internet money optimistic place. I can stay with this.

The enterprise as such is producing respectable cashflow. Clearly with Hoffmann, the dynamics would possibly change just a little bit as distribution is just a little bit totally different to an industial.

My impression is that SFS is run very conservatively. They appear to personal most of inheritor actual property, slaary ranges for Managment are ample and steering is at all times conservative. SFS is “constructed to final”.

One different subject I discovered very attention-grabbing is that SFS has been ranked because the quantity 8 of all Firms lively in Switzerland with regard to Digital Transformation. Throughout the Manufacturing trade they have been rated #1. Though one ought to at all times be cautious with such rankings, that is clearly an attention-grabbing facet and an extra poece of the puzzle.

Lastly, I additionally like the truth that SFS doesn’t do quarterly stories. For a long run funding, this protects my at the very least 2 instances a 12 months the place I don’t must learn or analyse stories.

13. Execs and Cons

Earlier than transferring to a conclusion, as at all times I’ll attempt to summarize whats good and what’s not so good:

Professional:

- household owned, long run orientation

- an excellent enterprise (low worth however mission vital excessive precision consumable components)

- an honest valuation (particularly in comparison with Swiss friends)

- good managment

- Strong funds, conservatively run

- decentralized construction

- resilient enterprise (vitality, enter materials)

Cons:

- very massive acquisition closed in 2022

- unsexy and arduous to clarify merchandise

- not tremendous low cost

- no clear moat

- Publicity to manufacturing / China

14. Abstract & return expectations

SFS Group is neither an “wonderful large moat” firm nor a brilliant low cost alternative. Nevertheless it’s a superb enterprise/firm at a really respectable valuation. Getting superb firms at respectable valuations is definitely my candy spot, particularly when I’m satisfied that the corporate is run with a view to the long run which I believe is right here the case.

I additionally like the truth that the corporate will not be very horny from the surface. It doesn’t entice a whole lot of consideration which is one other large plus for me.

On the present valuation, I’d anticipate a return of round 10% p.a. with out considering any a number of enlargement. That’s based mostly on a 2023 FCF yield of 4-5% and a long run development charge of additionally 5-6% that I believe is life like and even conservative, contemplating the observe file. So my base case could be to double my cash in 7 years plus dividends..

I subsequently determined to allocate ~4% of the protfolio into SHS at a median worth of round 104 CHF/per share throughout January.

15. Sport plan

Though the discharge of the earnings on March third might possibly set off a sure revaluaton if EPS is available in as I anticipate, my plan is to carry this positon long run. If my EPS expectations transform appropriate and relying on their steering and the share worth response, I’d enhance the place by one other 1% or 2%.

Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!!!

Appendix: Some bonus materials.

https://www.moneycab.com/particular person/jens-breu/