{kind=link}

Monetary literacy is a core requirement for a safe life. Many People nonetheless stay financially illiterate. In response to the Monetary Trade Regulation Authority, FINRA, for brief, greater than 6 out of each 10 People don’t have a grasp of elementary monetary ideas, making them vulnerable to accumulating unhealthy debt, making unwise spending choices, or simply not being ready for the longer term.

As if that wasn’t unhealthy sufficient, listed here are some somber details that emphasize the urgency right here:

- Nearly 8 out of 10 People don’t have any financial savings and reside paycheck to paycheck.

- Round 189 million People have at the least one bank card, with the common bank card proprietor holding nearly 4 completely different playing cards. In consequence, bank card debt has reached $1.04 trillion, with the common rate of interest at 24.16% as of March 28, 2023.

- Nearly 44 million People reside day by day with the immense weight of $1.5 trillion in scholar mortgage debt weighing down on their shoulders.

- In combination, the American inhabitants is grappling with a $12.58 trillion debt monster.

So, what is strictly monetary literacy, and who ought to be educating it to us?

What’s Monetary Literacy?

Merely put, monetary literacy is all about elementary monetary expertise that you should utilize in your on a regular basis life. These expertise embody budgeting, managing your private funds, and investing, and they are often the distinction between you being a company slave for the remainder of your life and also you residing the life you need, like retiring early, getting your children by faculty, and having fun with your life.

What Are These Basic Monetary Abilities?

Monetary literacy doesn’t solely provide you with extra management over your future; it prepares you for the tough blows that hit us all throughout stormy instances. So, to construct a sturdy ship that may make it to shore and face gargantuan waves alongside the way in which, here’s what you’ll want:

- Budgeting: How a lot of your month-to-month revenue do you spend on on a regular basis purchases? How a lot of it do you save for a wet day? What about investing?

- Investing: How do you select your investments? And do you consider your threat profile, or do you simply make investments haphazardly?

- Borrowing: How are you relating to borrowing cash? Do you consider rates of interest, or is your mortgage extraordinarily overpriced with out you understanding it?

- Taxes: Do you reap the benefits of the completely different allowances supplied by the IRS relating to saving on taxes, or do you let the taxman take extra of your annual revenue than needed?

- Private monetary administration: How do you combine the entire above expertise collectively? The place are you strongest, and the place are you weakest?

Combining these expertise may help you’re taking cost of your funds and handle your cash extra successfully.

Why is Monetary Literacy Essential?

Except for offering monetary stability, monetary literacy has a number of benefits:

- It makes you a greater negotiator. In any case, if you perceive how cash works, you should have a greater appreciation of the phrases of a deal. Additionally, you can find it simpler to decipher and interpret completely different monetary paperwork and contracts.

- It improves your general psychological well being. There’s something to be mentioned concerning the consolation and feeling of psychological security that comes from understanding that had been you to lose your job tomorrow, you and your loved ones would nonetheless be taken care of.

- It makes you a greater contributor to society. Not solely does it encourage you to put aside a portion of your finances in the direction of charity, but it surely additionally empowers you to be a extra lively participant in group affairs.

- Monetary literacy can cut back social inequality. It is among the finest instruments to allow folks to enhance their socioeconomic standing and rise out of poverty.

There’s actually not a lot debate over this. Whereas some might say (precisely) that monetary literacy alone won’t resolve many financial issues, nearly any particular person is best off with monetary literacy than they’d be with out it.

Why Ought to We Educate Monetary Literacy?

On one stage, that is apparent. If we have to study private finance, we must be taught. We are able to study by trial and error, however that’s not a good way to do it: by the point the teachings are realized, we might be deeply in debt.

There’s additionally a much less apparent however much more compelling motive to show monetary literacy.

Dangerous Monetary Habits are Taught Too

Most of us most likely don’t notice that we’re being inspired from an early age to undertake unhealthy monetary habits, however the fact is that we’re. From childhood onward, promoting urges us to need extra and to outline our self-worth by what we personal and the way we glance.

As we become older, extra strain piles on.

- We’re urged to attend costly personal faculties, even when it means plunging into an ocean of debt.

- Purchase now pay later (BNPL) plans promise straightforward funds and the power to purchase no matter we would like.

- Automotive sellers provide shiny new rides with no down cost.

- Bank card firms ship us prequalification notices with seductive signup bonuses.

- Lenders promise quick, straightforward money, simply signal on the dotted line and get your cash.

That’s only a few: the checklist might go on for miles. All over the place we glance, we’re urged to spend and to borrow, to need extra and purchase extra. There’s all the time an “straightforward” resolution, get it now and pay another time.

Each single considered one of these “offers” prices cash, typically quite a lot of cash.

It may be an overstatement to say that firms are spending trillions yearly to show monetary illiteracy, however not by a lot. The cash spent on attempting to show us good monetary habits is dwarfed by the cash spent to advertise unhealthy monetary habits.

Educating monetary literacy is one small step towards addressing that imbalance.

Who Ought to Be Educating Us Monetary Literacy?

1. Ought to It Be Our Colleges?

One fashionable view is that colleges ought to educate college students the fundamentals of monetary literacy. You’ve most likely even seen this view on social media.

So, ought to colleges educate college students monetary literacy?

Properly, 21 states appear to consider so, mandating that colleges embody the topic inside their curriculum. And, there are many causes to assist this determination: Not solely does it encourage college students to start out saving as early as doable, but it surely additionally helps them perceive the lifelong repercussions of their faculty loans.

Furthermore, a number of research point out the effectiveness of our colleges taking an lively position in our monetary schooling. As an illustration, one research discovered that after taking a private finance class, college students grew to become 23% much less prone to finance their collegial journey with loans and debt. Furthermore, those self same college students grew to become far more assured about their capability to speculate and far more appreciative of the ability of getting financial savings within the financial institution[2].

What’s extra, even academics are feeling extra assured about integrating monetary literacy into their curriculums.

Sadly, colleges are sometimes restricted in how a lot monetary schooling they will ship.

Whereas it could be nice to have colleges educate monetary literacy, there are obstacles. Monetary literacy isn’t obligatory in most states, and many faculties simply don’t hassle with it. Many academics don’t really feel snug educating the topic and aren’t in a position to give you age-appropriate lesson plans and educating supplies.

Extra importantly, a college’s affect is proscribed. Monetary literacy is not only about speaking data. It’s additionally about adapting our behaviors and reining in the psychological components that might lead us astray. Colleges are usually not all the time in one of the best place to form habits.

2. Ought to Monetary Literacy Be Taught at Residence?

Personally, I consider that among the duty of educating monetary literacy does fall on the mother and father, and the reason being that they will instill the right behaviors and beliefs early on of their kids.

They will obtain this in a number of methods:

- They will begin speaking about cash and funds when the children are younger. And these conversations can play an important position in how the kids find yourself managing their private funds. This additionally makes cash an on a regular basis subject to speak brazenly about and focus on reasonably than a taboo topic shrouded in secrecy.

- Dad and mom ought to act as position fashions, displaying their kids the best way to deal with each good and unhealthy instances. What we present is extra vital than what we inform. Furthermore, when mother and father present children the best way to save for a sure monetary objective or spend money on an index fund, these all find yourself turning into lasting studying experiences.

- Dad and mom can empower their children by opening up a checking account for them and serving to them get their first job. This job might be so simple as pet-sitting the neighbor’s canine or eradicating the snow from the driveway. Armed with an account and job, children will have the ability to begin saving and dealing in the direction of their very own private objectives.

Dad and mom have entry to quite a few instruments to assist them educate their kids throughout completely different life levels. So, whether or not the children are in Kindergarten or in Elementary college, they will profit from the correct software and study vital lifelong classes.

Sadly, mother and father are additionally restricted.

In an excellent state of affairs, the duty could be cut up between our colleges and our mother and father. The colleges would give us helpful cash classes, and our mother and father would instill in us the correct behaviors.

Nevertheless, simply as colleges could also be restricted in what they will provide our youngsters, so are the mother and father:

- Many mother and father could also be unqualified to show their children helpful cash classes. Do not forget that nearly 60% of American adults are thought-about financially illiterate. So, regardless of their finest intentions, mother and father might discover themselves in a state of affairs the place the blind are main the blind.

- But, the extra worrying drawback is that relating to cash, our actions hardly ever align with our phrases and beliefs, making many people ill-suited to be position fashions to our youngsters. Many mother and father grew up in households that didn’t speak about cash, and it’s laborious to interrupt that sample.

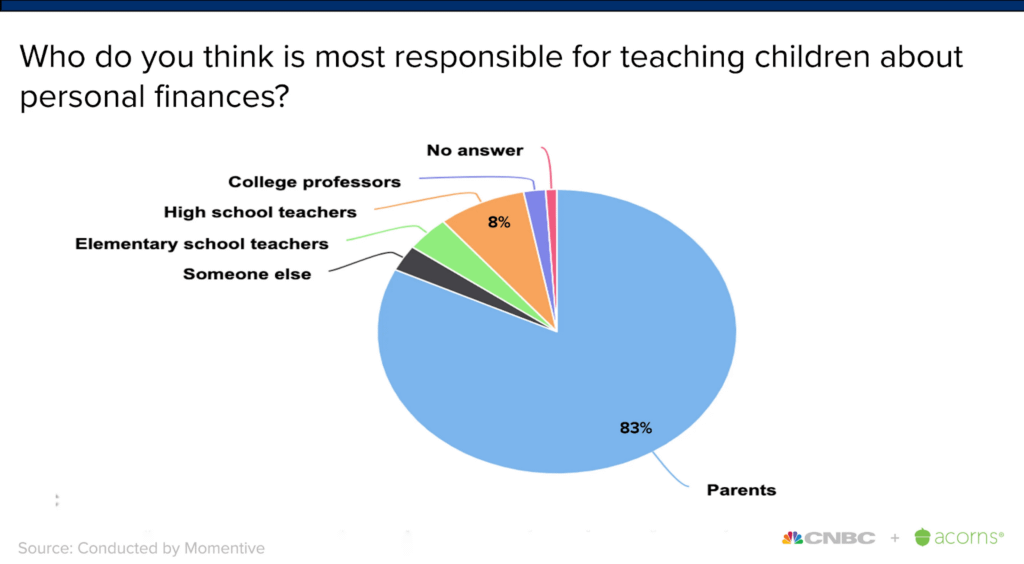

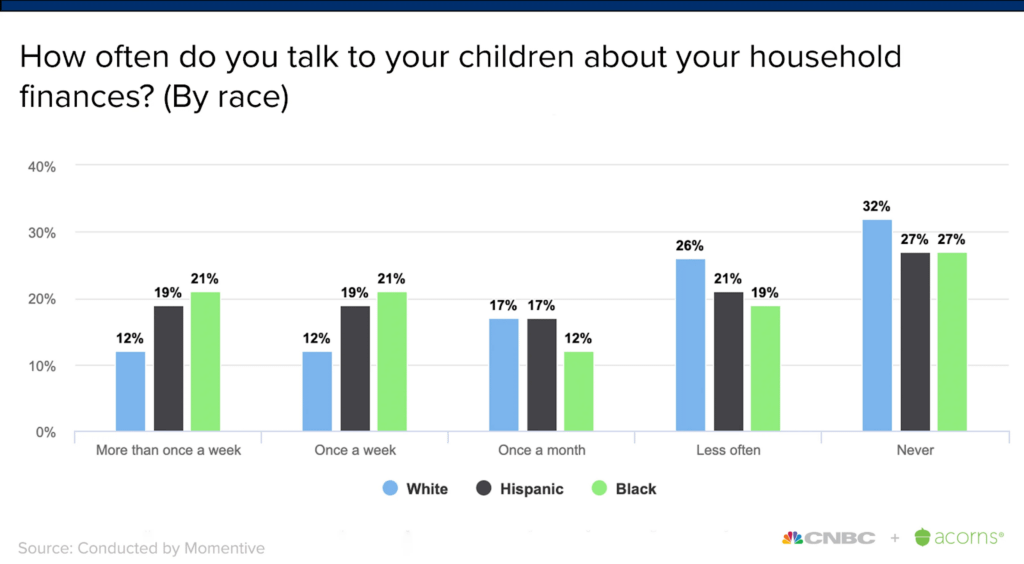

- Moreover, though a number of mother and father consider that they need to educate their kids about cash, few of them really pull by. In response to one survey, round 83% of People consider that folks ought to be the primary ones chargeable for their kids’s monetary schooling. However, a meager 15% of those self same adults took the time to speak to their kids about cash greater than as soon as each 7 days[1].

Most of us suppose we must always educate our youngsters about cash, however too many people don’t do it.

3. The Accountability is Ours

So, if each colleges and fogeys are restricted, then the place does the majority of the duty in the end lie?

I consider the reply is with us.

There are numerous on-line sources these days that may educate us all the pieces we might presumably need about finance. You’ve gotten books, Youtube channels, and Fb Teams, all devoted to educating us the best way to handle our funds higher.

On the finish of the day, the well being of your funds depends in your behaviors and attitudes far more than in your understanding of the intricacies of the banking system. It’s your duty to study to manage your self financially.

It’s also on you to know your self properly sufficient to know which kinds of investments you’ll be snug with and which varieties will hold you up at night time. On the finish of the day, only a few issues are value your peace of thoughts.

As with our different choices, self-guided studying additionally has its limitations. One is that the choice to pursue monetary data requires an consciousness of finance that many younger folks simply don’t have. In consequence, many younger folks don’t get critical about monetary literacy till they’ve already made critical and avoidable errors.

Placing It All Collectively…

It may be straightforward responsible the college system or our mother and father for not educating us the best way to do taxes or make investments our cash. However, I personally consider that that thoughts body robs us of our company.

Sure, it could be nice if we might study cash in school, and it could be even higher if our mother and father might focus on with us the funds of the house recurrently. However, even when we had neither of these choices rising up, we now reside within the age of data, the place something we need to study is actually at our fingertips.

So, who ought to educate you about monetary literacy?

👉 My reply could be 10% is the college’s duty, 20% is the mother and father, and the remaining 70% is all on you.

The issue, in fact, is that with the intention to educate ourselves successfully, we’ve to get up to the necessity for monetary literacy, ideally earlier than we’ve already dug ourselves right into a gap. That implies that whereas colleges and households is probably not the perfect supply of monetary data, they play an important position in getting us began on the trail to monetary data!